Feb 2015

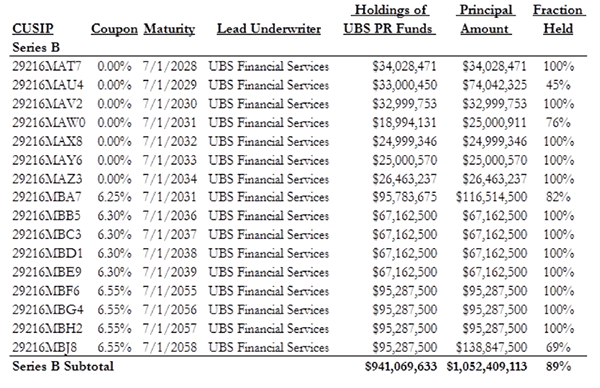

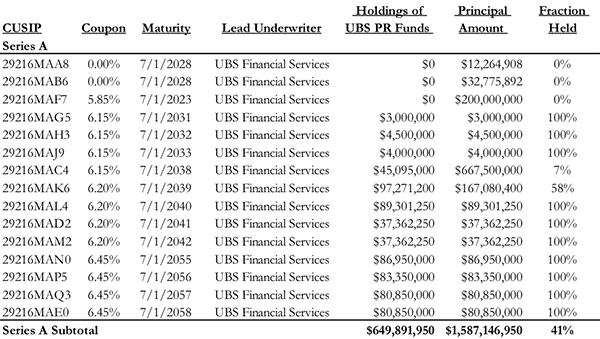

The System currently contemplates offering additional parity Bonds (the "Series B Bonds") in other jurisdictions. The Series B Bonds would be offered by means of one or more separate Official Statements and may not under any circumstances be purchased by residents of Puerto Rico.The 2008 Series A Offering Circular language was unambiguous protection for Puerto Rican investors in the 2008 Series A bonds since the Series B bonds, which would be on par with the Series A bonds, would only be issued if the Series B bonds passed the market test.