UBS has argued that since we couldn't identify which trades in the EMMA data were the UBS bond fund trades and UBS wasn't providing the data, we shouldn't speculate about whether UBS charged excessive markups or not. It turns out that we can identify at least some of UBS's purchases of Puerto Rican municipal bonds for the funds it managed and those purchases tell an interesting story.

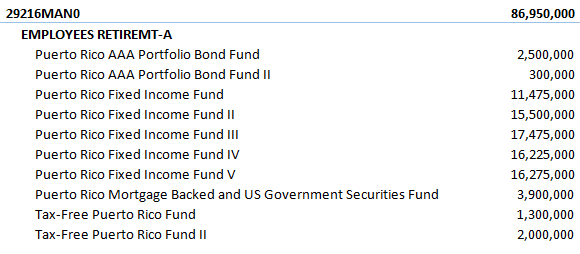

Table 1 shows UBS PR funds' $86.95 million holdings face value of the 6.45% coupon, long term Puerto Rican municipal bond (CUSIP: 29216MAN0) issued in January 2008 by the Employees Retirement System.

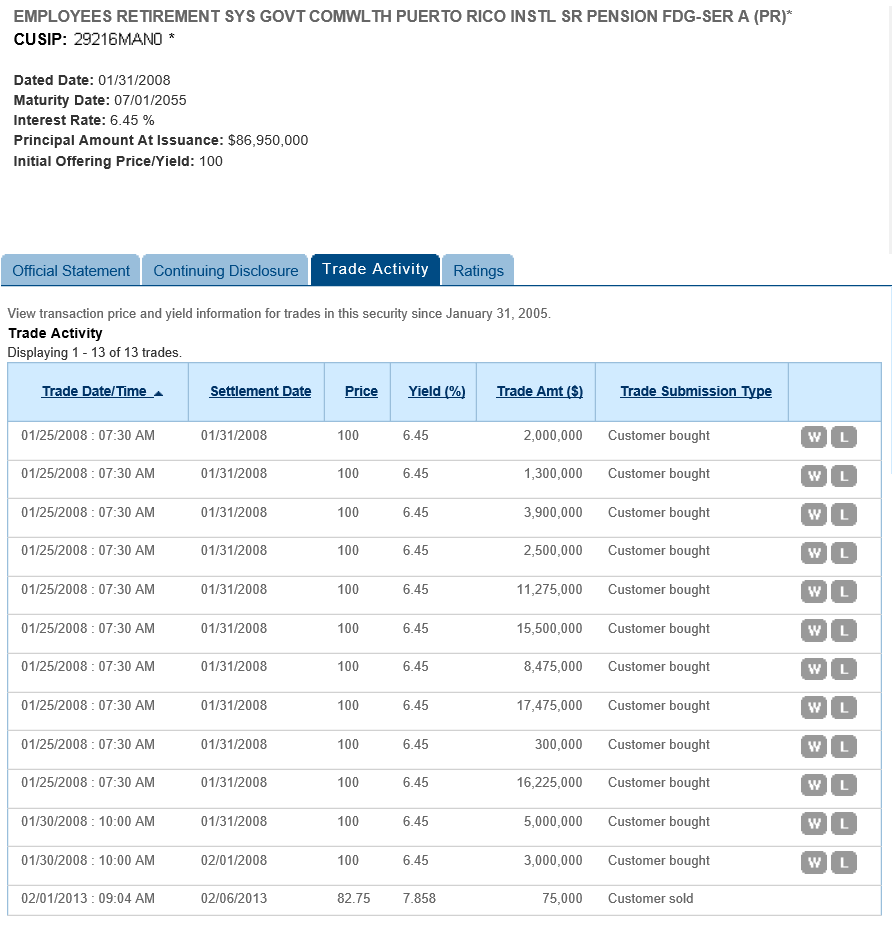

Table 2 lists the trading activity in this bond and shows that these UBS funds were the only purchasers of this $87 million bond issue and that the funds paid the $100 offering price.

There are many other examples in which the UBS funds buy all, or virtually all, of a UBS underwritten bond from an issuer whose bonds the mainland funds wouldn't touch. This raises a number of issues which we address in later posts. For today, we will just address the markup issue.

Our example bond was part of a larger Employees Retirement System deal. The Official Statement can be found online. The underwriters paid $98.95 on average for the bonds. UBS resold these bonds, which it paid the Employee Retirement System approximately $86,033,050 in the when-issued market, to its proprietary mutual funds for $86,950,000. UBS charged its mutual fund investors a $916,950 markup over the price UBS paid the issuer in what was, economically at least, a riskless principal trade. This as a 1.05% markup on an $86 million institutional purchase.

Breen, Hollifield, and Schurhoff (2006) find the average underwriting spread on municipal bonds is 0.8% and that more than half of this spread is provided to the brokerage firm as a sales credit or gross commission to motivate the sales force.*

They also find that a significant fraction of large trades are done below the reoffering price at the time of the offering.

So, if a $300,000 underwriter spread on this CUSIP would have been roughly the average non-sales credit component of the spread, why did UBS charge its mutual fund investors an additional $616,950? There were no retail brokers to motivate.

UBS paid the Puerto Rican Employee Retirement System hundreds of thousands of dollars less than it should have or UBS caused its mutual fund investors to pay hundreds of thousands of dollars too much - or both.

Ultimately others will judge UBS's conduct but, to my eyes at least, the answer to the question posed in the title of this post is Yes.

_______________________________________

*Breen, Hollifield, and Schurhoff (2006) "Dealer Intermediation and Price Behavior in the Aftermarket for New Bond Issues."