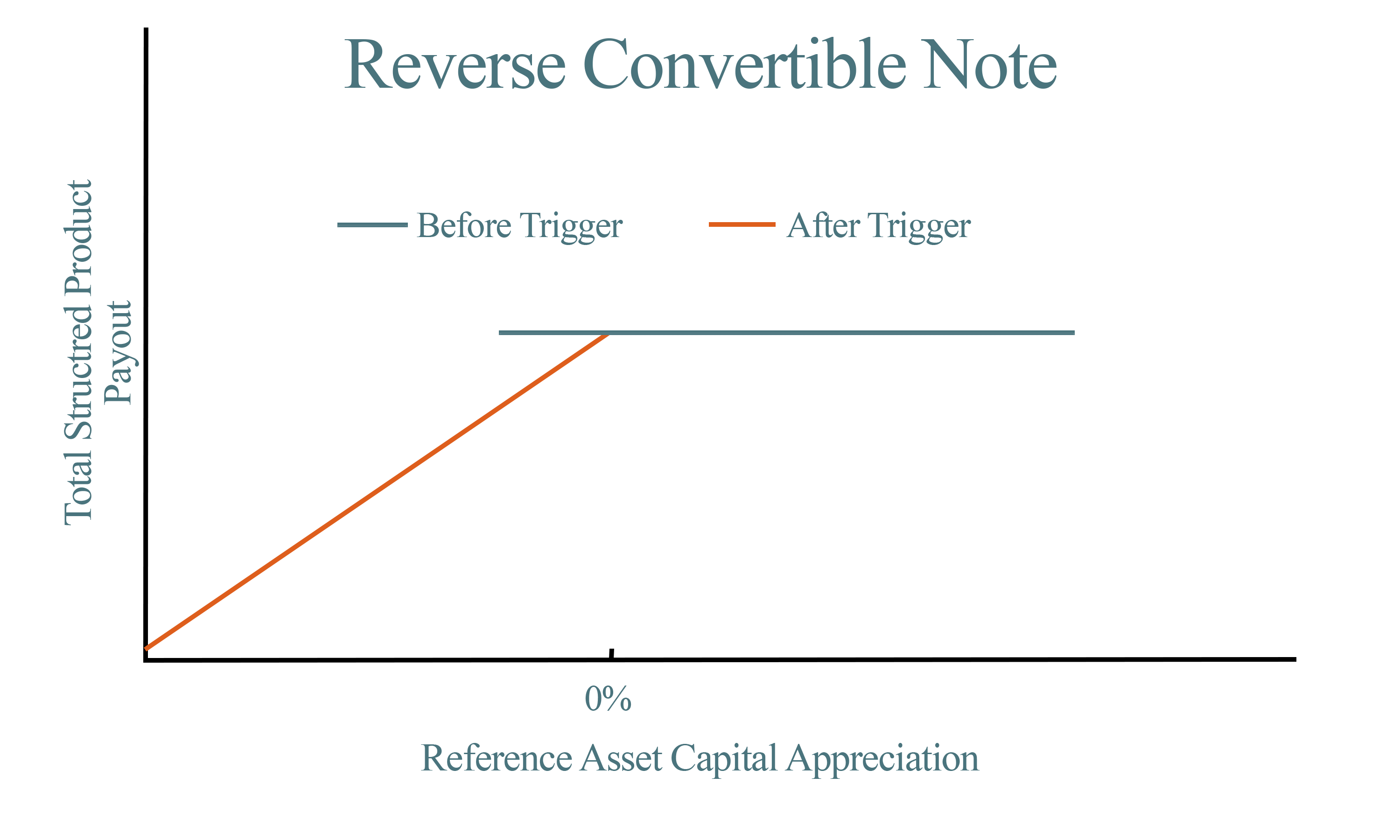

Basic Reverse Convertibles

Basic reverse convertibles are notes whose repayment of principal is linked to the reference asset's lowest value during the note's term. If the reference asset's value falls below a pre-specified level during the term of the note, investors receive substantially

less than the note's face value. Basic reverse convertibles tend to pay higher coupon rates than traditional notes because they expose investors to much more risk than traditional notes.

A common basic reverse convertible has the same payoffs as an unsecured note issued by the brokerage firm and a contingent at-the-money short put option on the reference asset. If the reference asset's value falls below a threshold

or "trigger" price at any point during the term of the note, the contingent put option is activated and the reverse convertible note will pay the lesser of the face value of the note and the market value of the number of shares of the

reference asset which could have been purchased on the note's pricing date with the note's face value. If the reference asset's value never drops below the trigger price, the reverse convertible note will pay investors the face value of

the note at maturity.

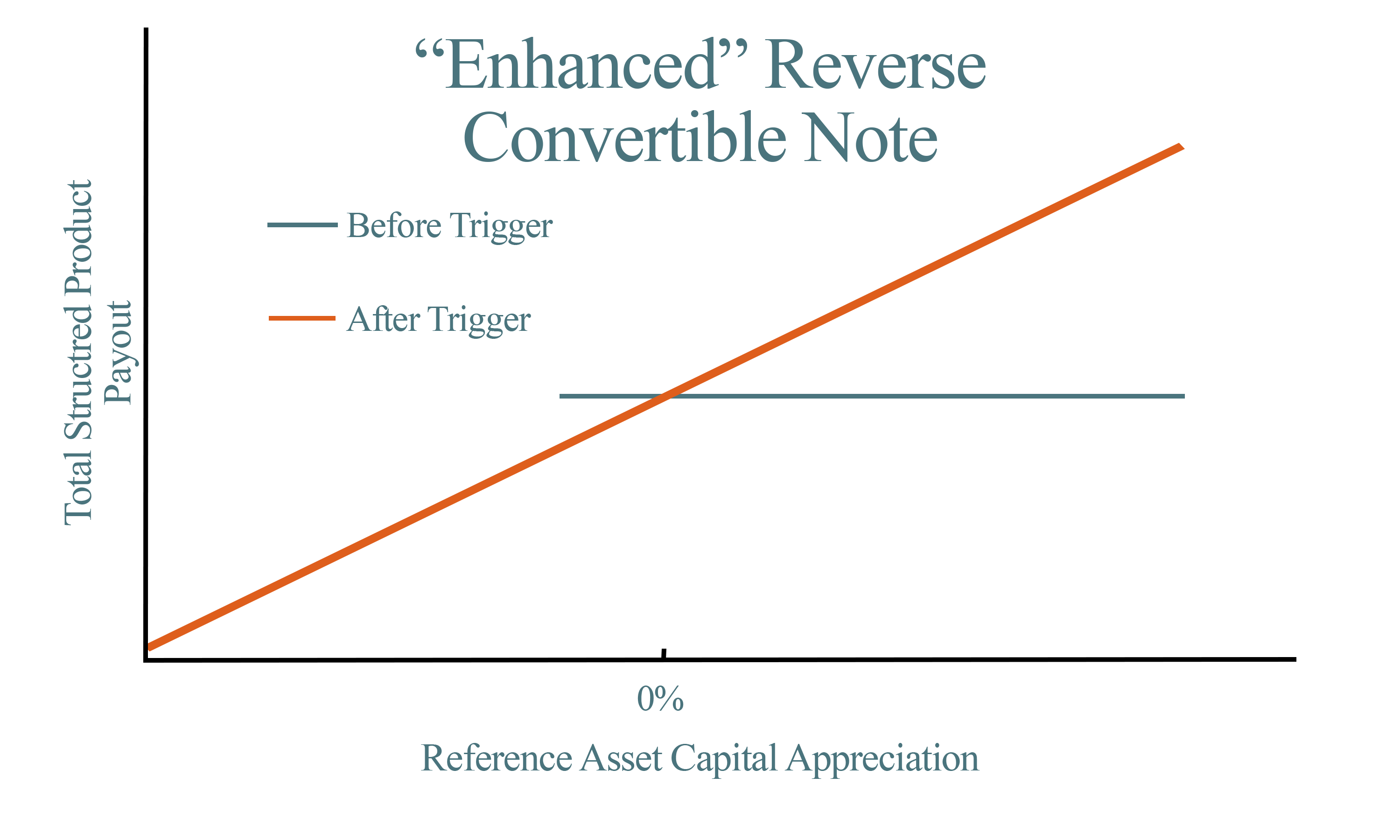

Some brokerage firms issued "enhanced" reverse convertibles that exposed investors to both the downside risk and the appreciation potential of the reference asset if the trigger was breached. Such "enhanced" reverse convertibles

include ELKS®, issued by Morgan Stanley, and some Yield Optimization Notes with Contingent Protection issued by UBS.

These "enhanced" reverse convertibles appear to be more valuable than the other basic reverse convertibles because the payoff at maturity isn't capped if the note converts into the reference asset. However, this advantage is illusory.

It is unlikely that once the underlying security's value drops below the trigger level it will rebound back above the initial level during the remaining term of the note.

Basic reverse convertibles have been sold by many different brokerage firms including JP Morgan, Barclays, Citigroup, Morgan Stanley, Wachovia, Lehman Brothers, Royal Bank of Canada, and ABN Amro. Although many firms have branded

their reverse convertibles, most are similar in structure. Table 1 lists a few of the names under which basic reverse convertibles have been sold by various brokerage firms.

Table 1: Basic Reverse Convertibles

| Brokerage Firm |

Brand Name |

| JP Morgan |

Reverse Exchangeable Notes |

| Barclays |

Reverse Convertible Notes |

| UBS |

Reverse Convertible Notes |

| Morgan Stanley |

ELKS |

Single Observation Reverse Convertibles

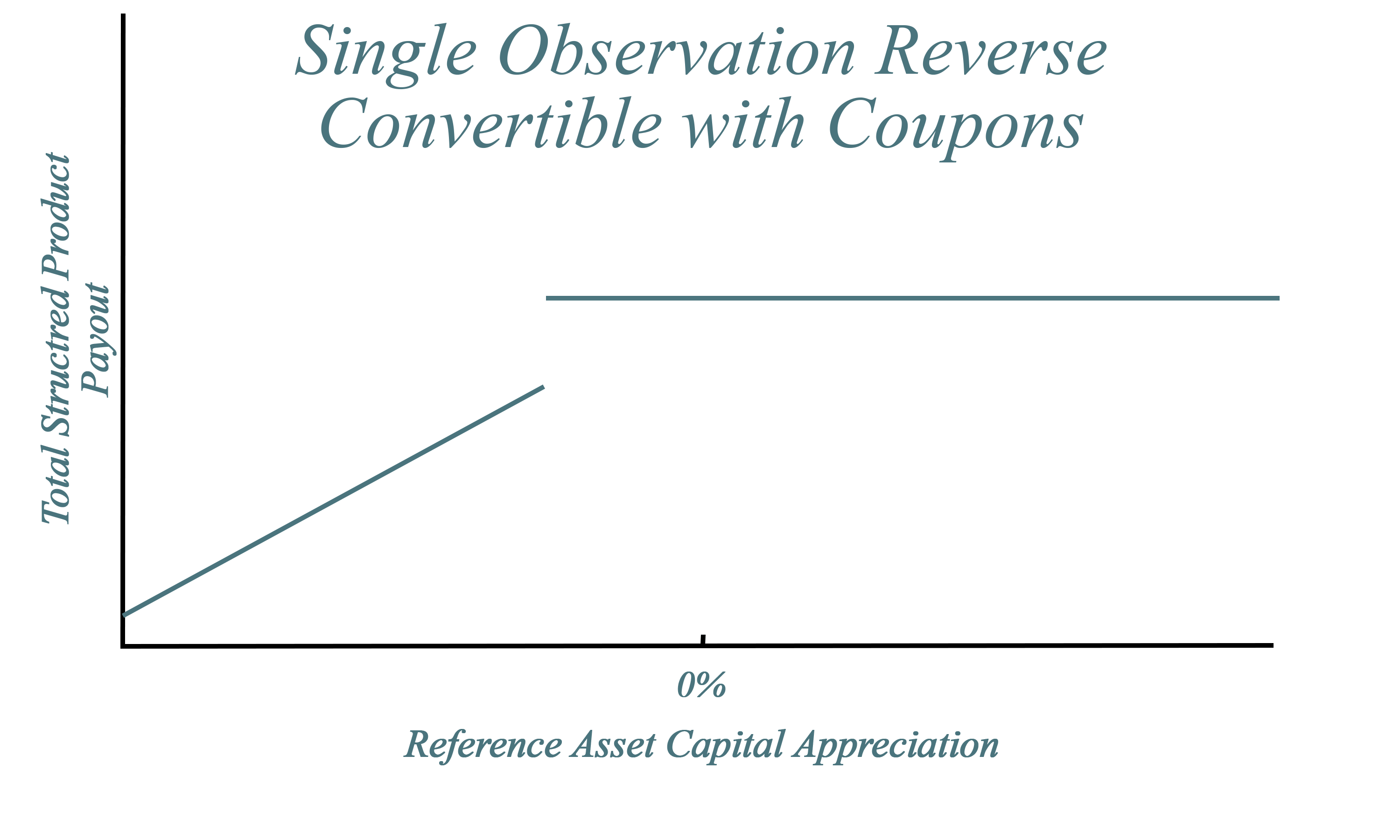

Single observation reverse convertibles pay a fixed positive return if the pre-specified trigger is not breached on the note's final valuation date, and a lesser amount if the trigger is breached. Whereas basic reverse convertibles use the reference asset's

lowest value to determine if the trigger has been breached, single observation reverse convertibles use the reference asset's value on the note's final valuation date. All single observation reverse convertibles expose investors to the

potential losses of the reference asset.

Single observation reverse convertibles cover a broad range of structured products. For example, some single observation reverse convertibles use coupon payments to compensate investors for bearing risk, while others use exposure

to a limited portion of the reference asset's capital appreciation.

Single observation reverse convertibles that pay coupons to compensate investors for bearing risk are quite similar to basic reverse convertibles. Neither type of reverse convertible offers exposure to the reference asset's capital

appreciation, and both expose investors to all of the reference asset's capital depreciation if a trigger is breached.

The only difference is that basic reverse convertibles compare the reference asset's lowest value to the trigger level, while single observation reverse convertibles compare the reference asset's final value to the trigger level.

This type of single observation reverse convertibles includes Yield Optimization Notes with Contingent Protection and Buffered Reverse Convertible Notes. The maturity payoffs to these single observation reverse convertibles are

similar to the payoffs of an unsecured coupon-bearing note combined with a contingent short put option on the reference asset.

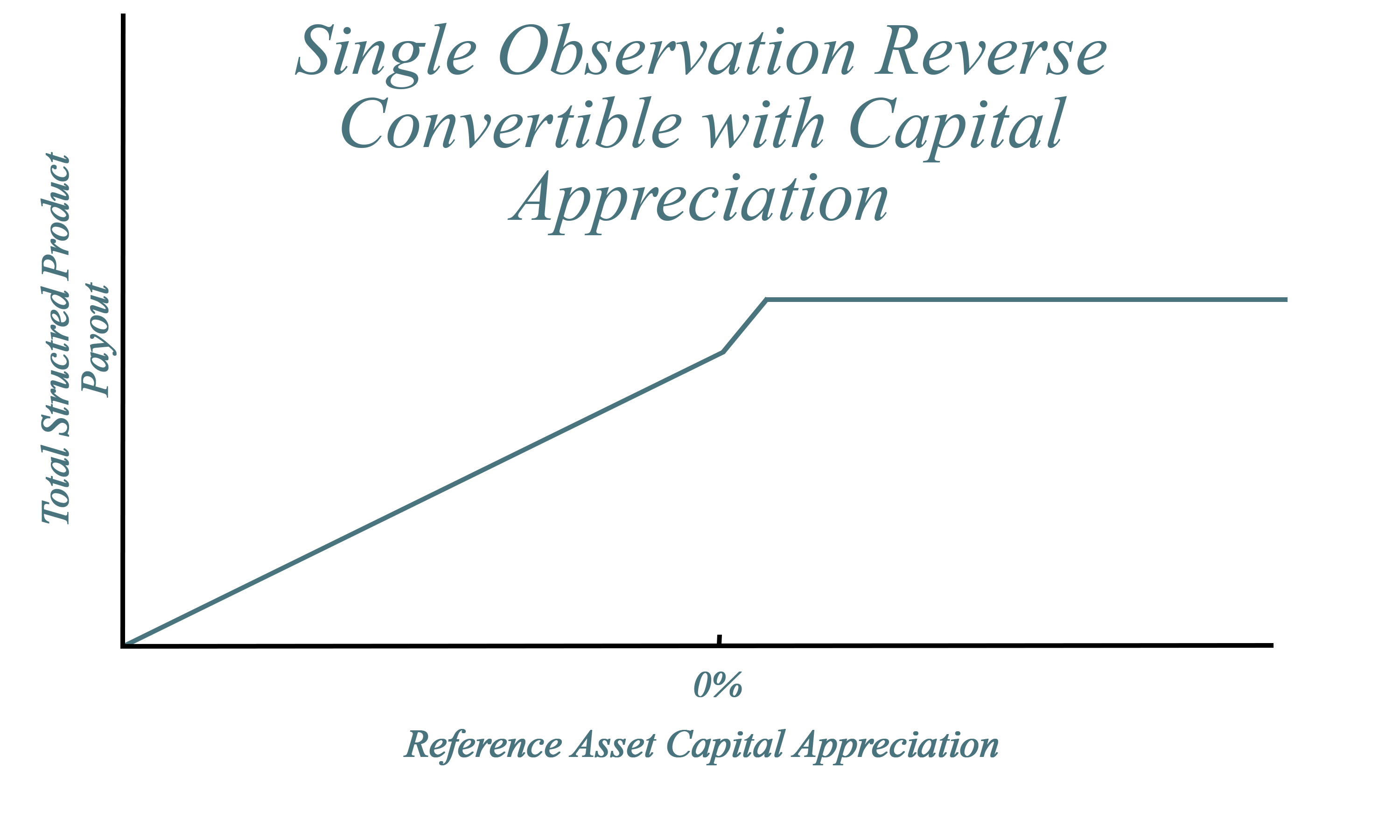

Single observation reverse convertibles that use small exposure to the reference asset's capital appreciation to compensate investors for the risk of loss have payoffs exactly like a zero-coupon, unsecured note issued by the brokerage

firm and three options on the reference asset: a short put option, a long call option, and a short call option. This type of single observation reverse convertibles include some PLUS and Buffered PLUS, Buffered SuperTrack and Buffered

iSuperTrack notes, Performance Securities with Contingent Protection, and Return Optimization Securities with Contingent Protection.

Table 2 lists a few of the single observation reverse convertibles which have been sold under different brand names by various brokerage firms.

Table 2: Single Observation Reverse Convertibles

| Brokerage Firm |

Brand Name |

| Barclays |

Yield Optimization Notes w Contingent Protection |

| Barclays |

SuperTrack Notes |

| Barclays |

Buffered SuperTrack Notes |

| Barclays |

Performance Leveraged Upside Securities |

| Barclays |

Buffered Performance Leveraged Upside Securities |

| Barclays |

Return Enhanced Notes |

| Barclays |

Buffered Return Enhanced Notes |

| Barclays |

Buffered Digital SuperTrack Notes |

| Barclays |

Buffered iSuperTrack Notes |

| Barclays |

Buffered Reverse Convertible Notes |

| Barclays |

Return Optimization Sec w Partial Protection |

| Barclays |

Return Optimization Sec w Contingent Protection |

| Barclays |

Knock-in SuperTrack Notes |

| JP Morgan |

Yield Optimization Notes w Contingent Protection |

| JP Morgan |

Return Enhanced Notes |

| JP Morgan |

Buffered Return Enhanced Notes |

| JP Morgan |

Single Observation Reverse Exchangeable Notes |

| JP Morgan |

Performance Leveraged Upside Securities |

| JP Morgan |

Buffered Performance Leveraged Upside Securities |

| JP Morgan |

Buffered Equity Notes |

| Morgan Stanley |

Performance Leveraged Upside Securities |

| Morgan Stanley |

Buffered Performance Leveraged Upside Securities |

| UBS |

Return Optimization Sec w Partial Protection |

| UBS |

Return Optimization Sec w Contingent Protection |

| UBS |

Yield Optimization Notes w Contingent Protection |

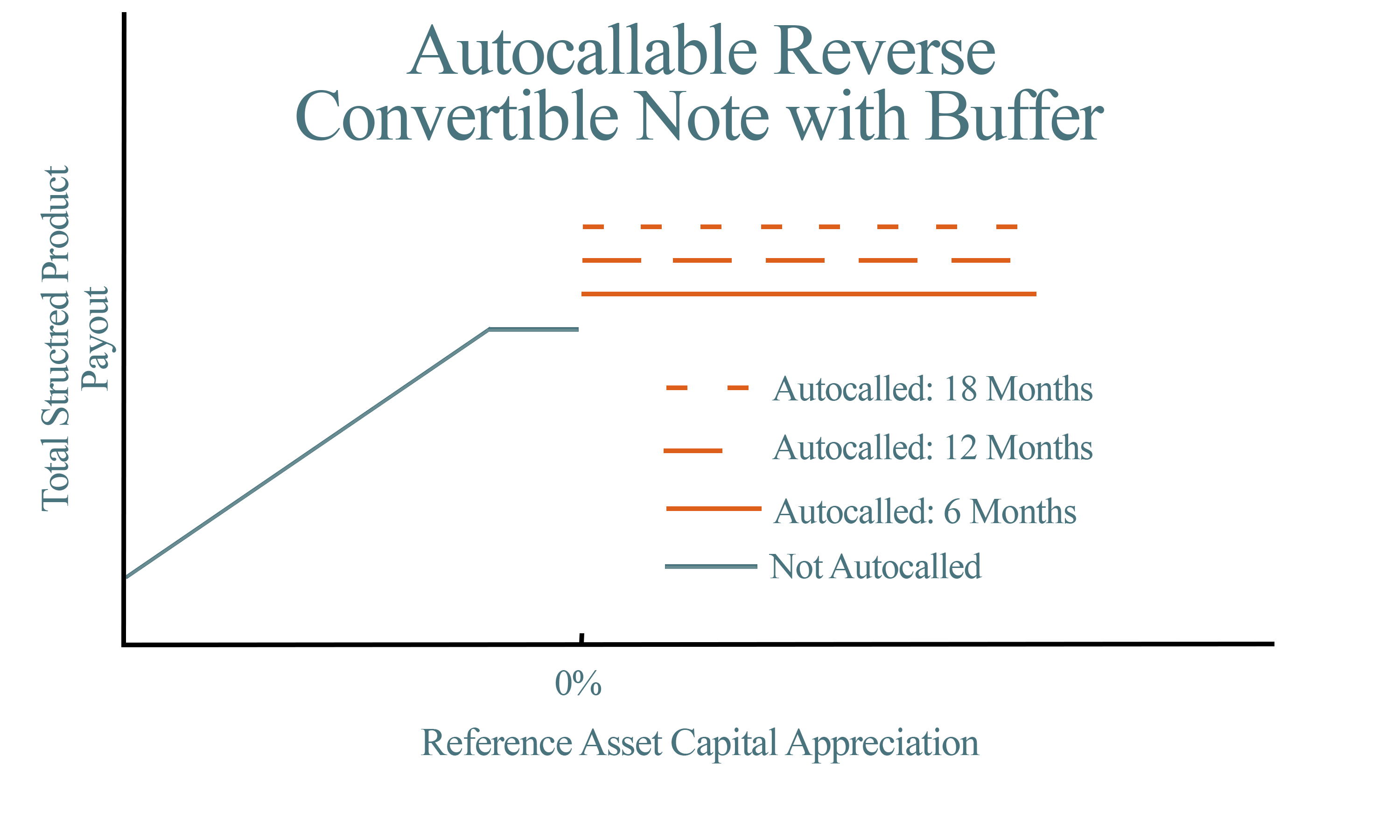

Autocallable Reverse Convertibles

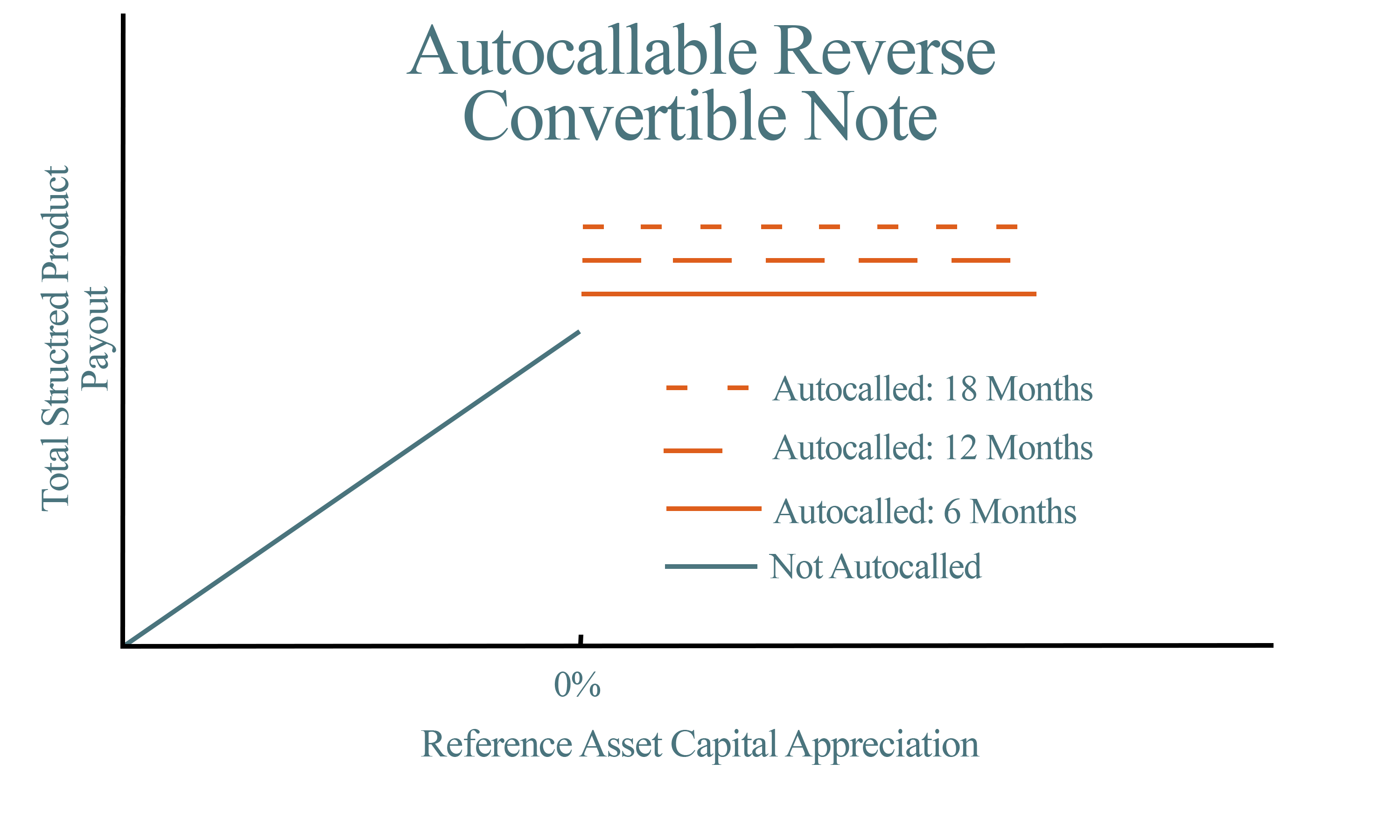

Autocallable securities are a type of reverse convertible. Autocallable securities have one or more call dates on which the structured product must be called by the issuer at a pre-specified premium if the reference asset's value has crossed a pre-specified

"trigger." The call dates tend to be contract anniversaries and the premiums to face value paid when the security is called increase with successive call dates.

If the product is not called, the payoff at maturity exposes the investor to the reference asset's risk of capital loss without offering any exposure to the reference asset's capital appreciation.

Some autocallable reverse convertibles' payoffs at maturity depend on the reference asset's value on the note's final valuation date, while others depend on the reference asset's lowest value during the note's term.

The maturity payoffs to some autocallable reverse convertibles are not reduced below the face value by the full percentage decline in the reference asset's value. The size of this buffer can vary significantly.

Table 3 lists a few of the autocallable reverse convertibles which have been sold under different brand names by various brokerage firms.

Table 3: Autocallable Reverse Convertibles

| Brokerage Firm |

Brand Name |

| Barclays |

Annual AutoCallable Notes |

| Barclays |

Semi-Annual AutoCallable Notes |

| Barclays |

Quarterly AutoCallable Notes |

| Barclays |

Autocallable Optimization Securities w Contingent Protection |

| JP Morgan |

Autocallable Optimization Securities w Contingent Protection |

| UBS |

Autocallable Optimization Securities w Contingent Protection |

| Morgan Stanley |

Auto-Callable Securities |