We've shown in recent posts that UBS underwrote $1.7 billion of unmarketable ERS and $1.35 billion of COFINA bonds and bought them into the UBS PR Funds in 2007 and 2008. You can find our earlier blog posts on Puerto Rican Funds. UBS made room for these ERS and COFINA bonds by selling out of the Funds, roughly $3 billion of other bonds UBS didn't underwrite. UBS bought the ERS and COFINA bonds it underwrote in 2007 and 2008, because there was no other market for the bonds it was underwriting.

The disastrous losses suffered by investors in the UBS PR Funds in 2013 are directly traceable to UBS putting its interests ahead of its clients in 2008 as we show in three examples.

Fixed Income Fund II's

Figure 1 categorizes the Fixed Income Fund II's November 30, 2012 holdings into ERS, COFINA and Other. ERS bonds are 27.5% of the portfolio, COFINA bonds are 21.3% of the portfolio and Other Investments are 51.1% of the portfolio. The ERS bonds lost 50.3% of their value from November 30, 2012 to December 13, 2013. The COFINA bonds lost 29.7% from November 30, 2012 to December 13, 2013. Other investments in the Fund lost between 4.8% and 15.8% of their value between November 30, 2012 and December 31, 2013. If the ERS and COFINA bonds had only suffered the losses suffered on the rest of the Fixed Income Fund II's portfolio, the Fund would have only lost $140.2 million instead of between $201 and $251 million.1

Figure 1. Fixed Income Fund II Asset and Losses Allocation

Fixed Income Fund III

The same pattern found in the Fixed Income Fund III can be observed in the other UBS PR funds. Figure 2 presents similar analysis for Fixed Income Fund III. ERS bonds are 28.1% of the portfolio, COFINA bonds are 15.1% of the portfolio and Other Investments are 56.8% of the portfolio.

The ERS bonds lost 45.4% from June 30, 2013 to December 13, 2013. The COFINA bonds lost 26.2% from June 30, 2013 to December 13, 2013. Other investments in the Fund lost between 2.6% and 12.5% of their value between June 30, 2013 and December 31, 2013.

If the ERS and COFINA bonds had only suffered the losses suffered on the rest of the Fund's portfolio the Fund would have only lost $103.6 million instead of between $151 million and $197 million.

Figure 2. Fixed Income Fund III Asset and Losses Allocation

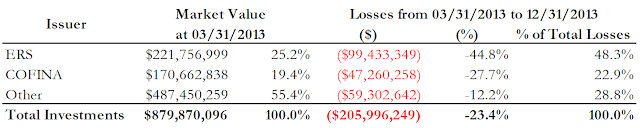

Fixed Income Fund IV

Figure 3 presents similar analysis for Fixed Income Fund IV. ERS bonds are 25.2% of the portfolio, COFINA bonds are 19.4% of the portfolio and Other Investments are 55.4% of the portfolio.

The ERS bonds lost 44.8% from March 31, 2013 to December 13, 2013. The COFINA bonds lost 27.7% from March 31, 2013 to December 13, 2013. Other investments in the Fund lost between 8.0% and 12.2% of their value between March 31, 2013 and December 31, 2013.

If the ERS and COFINA bonds had only suffered the losses suffered on the rest of the Fund's portfolio the Fund would have only lost $107 million instead of $206 ($185) million.

Figure 3. Fixed Income Fund IV Asset and Losses Allocation

So now we see what hell hath UBS wrought with its self-dealing. We estimate these three funds lost between $537 million and $654 million. Of these losses, the UBS underwritten ERS and COFINA bonds lost $464 million. That is, between 71% and 86% of the billions of dollars the UBS PR Funds lost in 2013 was the direct result of the UBS underwritten ERS and COFINA bonds for which there was no market.

1 We estimated a range of possible losses on the Funds' portfolios because the Funds do not produce financial statements for the periods over which we have spanning holdings data and the number of units of each fund changes significantly over time.