The Use of Leverage in the UBS Puerto Rico Closed-End Funds Magnified Losses

Jan 2014

The massive declines that hit investors in the UBS Puerto Rico closed-end bond funds in 2013 were especially quick and brutal for fixed income securities which are usually safer investments. In previous posts we have discussed some of the reasons for the precipitous fall in the values of the bond funds and some of the nuances of bond transactions that may have given rise to conflicts of interest between the fund managers and investors. In this post, we will discuss another culprit in the destruction of value for the funds' investors: the fund managers' use of leverage in the funds.

Closed-end funds, even those domiciled in the United States, often borrow and purchase more securities than the funds' net assets in an attempt to increase returns. This "leverage" can take many forms: direct borrowing from financial institutions, the issuance of preferred stock, and security repurchase agreements are some examples. Regardless of the specific form of borrowing, the leverage unequivocally increases risk to fund shareholders. The amount of leverage a closed-end fund utilizes is often measured by the amount of borrowing divided by the total assets of the fund (debt/total assets). This "leverage ratio" is the portion of the fund's assets purchased with borrowed money rather than with fund investors' contributions. Closed-end funds in the United States are generally limited to a maximum leverage ratio of 33% on borrowings and 50% on preferred stock issuance. The UBS PR funds can employ a leverage ratio of 50% on all forms of leverage. So, for example, a UBS PR fund with $500 million in portfolio securities may have total borrowings of up to $250 million. In unsettled market conditions, the Puerto Rico Commissioner of Financial Institutions may allow a fund to have a leverage ratio of 55%.[1]

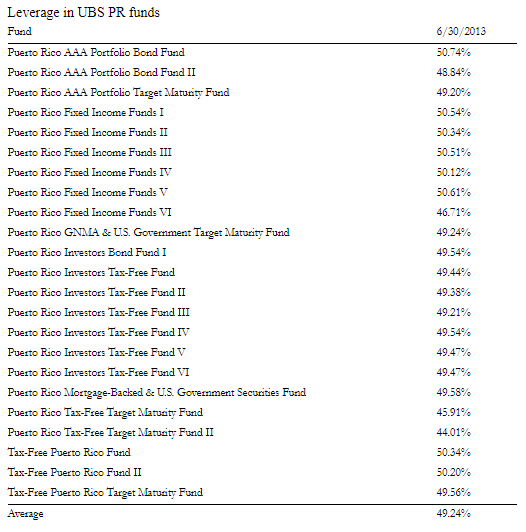

Our analysis of the UBS PR funds in 2013 shows that the funds on average had leverage that was very close to the maximum amount allowed by Puerto Rican securities regulations. In June 2013 the leverage ratios ranged between 44.01% and 50.74%. Declines in the value of Puerto Rican bonds that occurred in 2013 were magnified in the funds by the high use of leverage.

Leverage in UBS PR funds

We have already discussed the non-diversified (or concentrated) nature of the UBS PR funds in a previous blog post, and the coupling of concentration and leverage served to dramatically increase the risks to which fund investors were exposed. Our analysis of the funds shows that the UBS PR funds that experienced the greatest losses were heavily concentrated in the bonds of two specific Puerto Rican issuers: the Puerto Rican Employees Retirement System and the Puerto Rican Sales Tax Financing Corp. The use of leverage magnified the losses attributable to these two issuers. For example, the Puerto Rico Fixed Income Fund I portfolio had net assets of $361M as of June 2013. The leverage allowed the fund to hold total investments of $748M. Of these, $338M was in the two issuers. So while the two issuers represented 45% of the total investments in the fund, they represented 93% of the net assets of the fund. The risk exposure of investors is related to the percentage of net assets the securities represent. If those two issuers' securities declined to zero, it would have almost completely wiped out the fund.

In the three months ended September 2013, these issues lost 36% of their value. The losses in just these two issues caused a 34% decline in the net assets of the fund. Due to the fact that the holdings were close to half of the total assets in the fund and the leverage ratio was roughly 50%, declines in those two issuers together had close to a 1-to-1 impact on the fund.

As a comparison, a diversified fund with no leverage could have as a maximum only 10% of the total assets of the fund invested in two issuers. In such a situation, a decline in the bonds of the two issuers would only be felt by fund investors at 1/10th of the actual decline in the bonds. In our example where the two issuers fell by 36%, the diversified fund would have only declined by 3.6%.

Finally, some media reports have also pointed out that investors may have been encouraged to borrow money to invest in the UBS PR bond funds. This leverage, external to the funds, would further magnify investor losses. Our analysis above does not address this external component of leverage, but our proprietary research addresses the additional problems it causes.

[1] While the UBS PR Fund prospectuses express leverage in terms of a leverage ratio, the US Investment Company Act of 1940 discusses closed-end fund leverage in terms of "asset coverage ratios." The asset coverage ratio is simply the inverse of the leverage ratio. So the asset coverage ratio for Puerto Rican funds is 1/.50 = 2-to-1 or 200 percent. The higher the asset coverage ratio, the less leverage a fund is using.