Massachusetts Securities Regulators Fine RBC for Selling Unsuitable Leveraged and Inverse ETFs

(May 2012)

RBC Capital Markets has agreed to pay $2.9 million in restitution to Massachusetts investors related to the sale of unsuitable leveraged, inverse, and inverse-leveraged ETFs. Secretary of the Commonwealth of Massachusetts William Galvin, who has previously investigated Bank of America over warehousing of CLO assets, issued the complaint in July 2011, accusing RBC and its registered representative Michael D. Zukowski of selling these products "to clients who did not understand what these...

Is There No Tracking Error for ETNs?

(Apr 2012)

Some investors may think that while ETFs are subject to various tracking errors, ETNs are not. The argument goes that index-tracking ETFs often hold part or the entire portfolio underlying their targeted index and are thus subject to imperfect tracking and transaction costs. ETNs, on the other hand, are debt instruments, and have returns guaranteed by their issuers.

It turns out, however, that the daily return of an ETN investment may not necessarily equal the leverage ratio times the daily...

TVIX Explodes...Then Implodes

(Mar 2012)

The Wall Street Journal has an article about the rollercoaster ride that TVIX, a volatility-related ETN, has been on recently. [UPDATE 3/31/12: there is now a second WSJ article]

TVIX is a leveraged ETN issued by VelocityShares, which is Credit Suisse's ETF/ETN brand. Contrary to popular belief, TVIX and other volatility products do not track the CBOE S&P 500 Volatility Index (the VIX); instead, TVIX tracks a daily rolling portfolio of first and second month VIX futures with an average...

A Primer on Investment Companies

(Mar 2012)

Investment companies are entities that issue securities and whose primary business is investing in securities. We have written about investment companies in several of our posts (See blog posts on ETFS and Mutual Funds). This post provides a quick introduction to investment companies and the securities they issue. The three main types of investment companies according to federal securities regulation are: closed-end funds, unit investment trusts, and open-end funds.

Some of the main...

SPIVA Scorecard Year-End 2011

(Mar 2012)

S&P recently released their semiannual report comparing the performance of actively managed mutual funds against their appropriate benchmark indices. The S&P Indices Versus Active Funds (SPIVA) Scorecard contains information the mutual fund industry would likely prefer to be kept quiet.

The Year-End 2011 SPIVA Scorecard reports that "over a five-year horizon[...] a majority of active equity and bond managers in most categories lag comparable benchmark indices." Actively managed mutual funds...

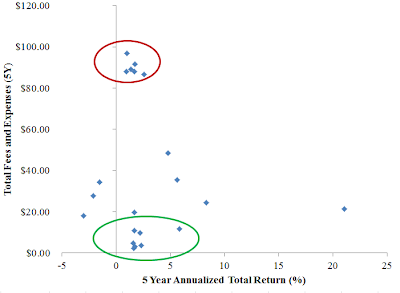

Which Would You Rather Have?

(Mar 2012)

Last month we had a blog post introducing the FINRA Mutual Fund Expense Analyzer tool. In this post we apply it to the 25 largest mutual funds and ETFs measuredby net asset value using data from Morningstar. We assumed for this calculation an initial investment of $1,000 held for five years, and plot the total fees and sales charges over that period against the historical 5 year annualized total return of the fund:

There is no clear linear relationship between returns and fees as depicted in...

Greg Smith Leaves Wall Street

(Mar 2012)

The New York Times published an op-ed by Greg Smith, a Goldman Sachs' Executive Director who is resigning from his job after almost 12 years with the firm because, as he puts it, the firm's culture has veered far from what it was when he first joined the firm. He says in spite of the firm's recent scandals "the interests of the client continue to be sidelined in the way the firm operates and thinks about making money." At SLCG, we have come across many examples of the issues raised by Mr....

SLCG Research: Non-Traded REITs

(Mar 2012)

We've posted a new working paper on our website that brings together much of our research related to non-traded Real Estate Investment Trusts (REITs). In it, we discuss the history and structure of non-traded REITs as well as differences between non-traded REITs and other avenues for gaining exposure to real estate. We highlight the dizzying array of fees and conflicts of interest embedded in these companies. We demonstrate that non-traded REITs are often misleadingly valued, heavily...