Non-Traded REIT Conflicts Run Amok: VRM I, VRM II and MVP, MVP II

Apr 2017

Introduction

SLCG has written extensively about pervasive conflicts of interest in non-traded REITs arising because a non-traded REIT's sponsor, advisor, selling agents, and major suppliers are often affiliated entities that benefit more from creating the non-traded REIT than from running the REIT profitably. See our blog posts on REITs. SLCG economists have also published peer-reviewed articles on non-traded REITs, including An Empirical Analysis of Non-Traded REITsi.

A collection of real-estate funds under common control based in Las Vegas, NV epitomize the worst of non-traded REIT abuses. The real estate funds (Vestin Realty Mortgage I, Vestin Realty Mortgage II, MVP REIT I, and MVP REIT II) are under the common control of Michael Shustek and, indirectly, Lance Bradford. The abuses include selling loans to related parties in non-arms length transactions, transferring liabilities to public investors through non-arms length transactions, and transferring property among related entities at less than arms length.

VRM I, VRM II, MVP REIT I, and MVP REIT II illustrate the perils of non-traded REITs in which control persons can direct transactions for their benefit with little or no regard for the harm they cause retail investors.

The extreme disregard shown by control persons for investors in these registered investments also highlights the potential risks associated with proposals to allow easier sale of unregistered investments to retail investors.

Mr. Shustek Reaped $1.6 Million by Purchasing a Loan from VRM II

In November 2014, Vestin Realty Mortgage II (VRM II) sold a $7.45 million loan due in January 2015 to its CEO, Mr. Shustek, for $3 million, plus 50% of whatever Mr. Shustek collected from the borrower beyond $3.0 million (after expenses).ii In January 2015, just two months after VRM II sold the loan to Mr. Shustek, the borrower paid back the loan and VRM II received an additional $1.6 million per the agreement. That means Mr. Shustek received at least $6.2 million from the borrower and kept at least $1.6 million for himself ($3.0 million + 2 * $1.6 million = $6.2 million).

Publicly available documents do not indicate whether VRM II conducted any due diligence to confirm that the transaction was fair to VRM II shareholders. However, Mr. Shustek's large windfall in two months, the myriad conflicts of interest, and the existence of other potential abuses of his power to control VRM II raise questions about the legitimacy of this loan transaction. The transaction stands out not only because it is an apparent abuse of his power, but also because of its size. In December 2014, VRM II only had $28.9 million of net assets, meaning the transfer of at least $1.6 million from VRM II to Mr. Shustek was a significant loss for VRM II investors.iii

The Influence and Control of Mr. Shustek and Mr. Bradford

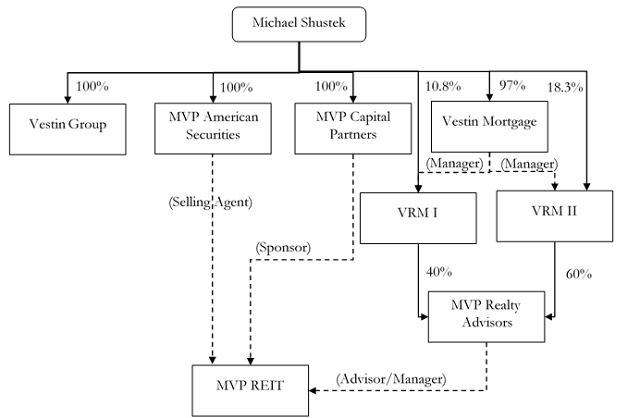

Mr. Shustek controls multiple companies, including the Vestin Mortgage, LLC, Vestin Realty Mortgage I (VRM I) and Vestin Realty Mortgage II (VRM II). Mr. Shustek also owns MVP REIT's sponsor, and one of MVP REIT's two selling agents. Figure 1 presents a simplified organizational chart of Mr. Shustek's influence over the related entities.

Figure 1. Mr. Shustek's Influence.iv Solid lines indicate ownership; dashed lines indicate non-ownership roles with significant influence.

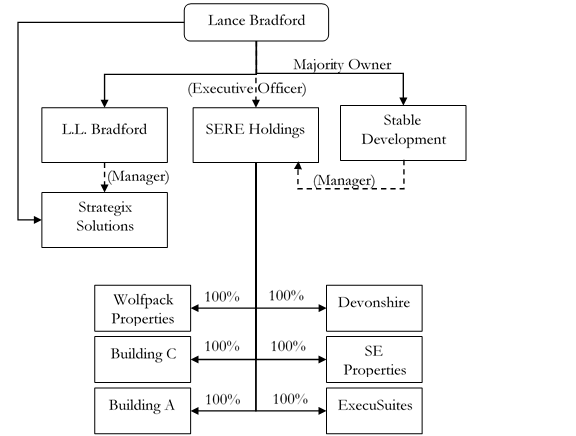

Mr. Bradford controls multiple companies, including L.L. Bradford (an accounting firm) and several holding companies, which transact with companies controlled by Mr. Shustek. Figure 2 presents a simplified organizational chart of Mr. Bradford's influence over the relevant entities.

Figure 2. Mr. Bradford's Influence.v Solid lines indicate ownership; dashed lines indicate non-ownership roles with significant influence.

Mr. Shustek and Mr. Bradford are also affiliated in ways that do not show up on the organizational charts. For example, Mr. Bradford was the President of MVP REIT (2016)vi, a managing officer of MVP Realty Advisors (1999-2005)vii, and an officer of Vestin Mortgage (1999-2005)viii. L.L. Bradford also provides accounting services to VRM I, VRM II, and MVP REIT.ix The questionable nature of Mr. Shustek's and Mr. Bradford's dealings is alluded to in a February 2016 article by a Las Vegas newspaper.x

Mr. Shustek Passed Between $4.5 Million and $17.4 Million in Costs on to VRM I and II

When Mr. Shustek created MVP REIT, he structured the advisory agreement so MVP Realty Advisors would pay the upfront selling commissions and offering and organizational costs. MVP Realty Advisors would then be recover its costs through acquisition fees and asset management fees. When MVP REIT began raising capital in September 2012, Mr. Shustek owned 60% of MVP Realty Advisors through MVP Capital Partners. By December 2013, MVP REIT had only raised $25.5 million of capital, suggesting the advisory agreement was going to be a negative net present value investment. By December 2013 VRM II had lent and written off approximately $6.1 million to MVP Realty Advisors. In December 2013, Mr. Shustek gave his 60% interest in MVP Realty Advisors to VRM I and VRM II. Subsequently, VRM I and VRM II loaned MVP Realty Advisors $4.5 million and an additional $6.8 million, respectively.xi The loans were written off as uncollectable in the same quarter they were issued. VRM II might have loaned MVP Realty Advisors the additional $6.8 million anyway, as VRM II was already a 40% owner. However, the $4.5 million from VRM I would likely have come from Mr. Shustek if he had retained his interest. In effect, Mr. Shustek saved at least $4.5 million by passing his 60% interest in MVP Realty Advisors on to VRM I and VRM II.

Despite owing $17.4 million to VRM I and VRM II, MVP Realty Advisors waived $6.9 million of fee revenue and expense reimbursements from MVP REIT by June 30, 2014.xii Thus, it appears VRM I and VRM II could have avoided some uncertainty about being repaid by just requiring MVP REIT to pay its bills. Both the near-immediate impairment of large loans to MVP Realty Advisors and the waived revenue from MVP REIT raise questions about conflicts of interest and abuses of power at VRM I and VRM II.

The Shustek/Bradford Real Estate Funds

Vestin Realty Mortgage I (Previously Vestin Fund I and DM Mortgage Investors)

Vestin Realty Mortgage I (VRM I) began as DM Mortgage Investors. On March 17, 2000, DM Mortgage Investors registered up to 100,000,000 shares at $1 per share, later amended to be up to 10,000,000 shares at $10 per share. See the registration statement. On June 29, 2001, DM Mortgage Investors changed its name to Vestin Fund I. All Vestin Fund I's SEC filings can be accessed on the SEC website. Vestin Fund I converted to Vestin Realty Trust I, quickly changed its name to Vestin Realty Mortgage I (VRM I) and began trading on the Nasdaq Capital Market on June 1, 2006, under the ticker VRTA. All VRM I's SEC filings can be accessed on the SEC website. In March 2012, VRM I ceased being a REIT, but continued trading on the Nasdaq.

Mr. Shustek was the President and CEO of Vestin Realty Mortgage I and its predecessors DM Mortgage Investors and Vestin Fund I. He was also the CEO and majority shareholder of Sunderland Corporation, which became Vestin Group, and which owned the Manager.

The Sunderland Corporation / Vestin Group route to becoming a publicly traded company is an interesting story. A shell company, Sunderland Acquisition Corporation, was registered by a Washington, DC lawyer on or about April 20, 1999. Mr. Shustek and Mr. Bradford are not mentioned in the registration statement. Two weeks later, Sunderland Acquisition Corporation acquired Capsource, Del Mar Mortgage and Del Mar Holdings, changed its name to Sunderland Corporation and shortly thereafter to Vestin Group. Mr. Shustek was the majority owner and Mr. Bradford was CFO.

Mr. Bradford functioned as the CFO of DM Mortgage Investors/Vestin Fund I.xiii He was also an executive of Sunderland Corporation. Mr. Bradford's accounting firm provided services to VRM I and its predecessors.xiv

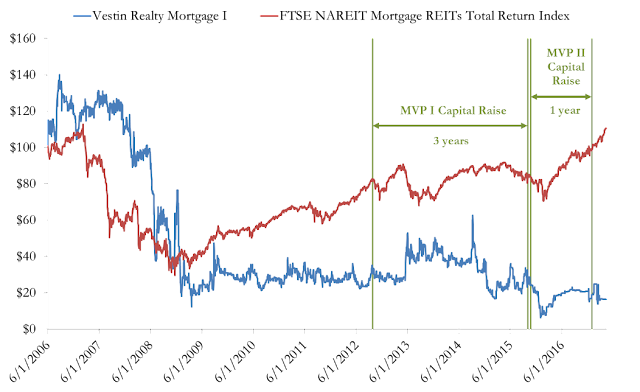

VRM I was always a very small REIT. Its market capitalization never reached $50 million. At the end of 2015, VRM I deregistered with the SEC and moved from the Nasdaq to the OTC Bulletin Board. VRM I's total return from inception to April 11, 2017 was -83.5%. During this same time period the total return to the FTSE Mortgage REIT Index was +11%. See Figure 3.

Figure 3. Vestin Realty Mortgage I (VRM I) Total Return

We have identified MVP I and MVP II's capital raise periods in Figure 3. These non-traded REITs discussed below were controlled by Mr. Shustek. Any brokerage firm considering selling either MVP I or MVP II, could have seen that investors in Mr. Shustek's VRM I had fared very badly both in absolute terms and relative to a more diverse set of mortgage REITs.

Vestin Realty Mortgage II (Previously Vestin Fund II)

Vestin Fund II registered up to 50 million shares at $10 per share on December 21, 2000. Vestin Fund II's registration statement is available on the SEC website. All Vestin Fund II's SEC filings can also be accessed on the SEC website. In May 2005, Vestin Fund II announced plans to convert to Vestin Realty Trust II. Instead, in March 2006, Vestin Fund II merged into newly formed VRM II and in June 2006 VRM II began trading on the Nasdaq as VRTB. At the end of March 2017, VRM II deregistered with the SEC and moved from the Nasdaq to the OTC market.xvVRM II's SEC filing began in 2005 and Vestin Fund II deregistered in 2006.

Michael Shustek is the President and CEO of VRM II.xvi Lance Bradford functioned as the CFO of VRM II's predecessor, Vestin Fund II.xvii Mr. Bradford's accounting firm provided services to VRM II and its predecessors.xviii

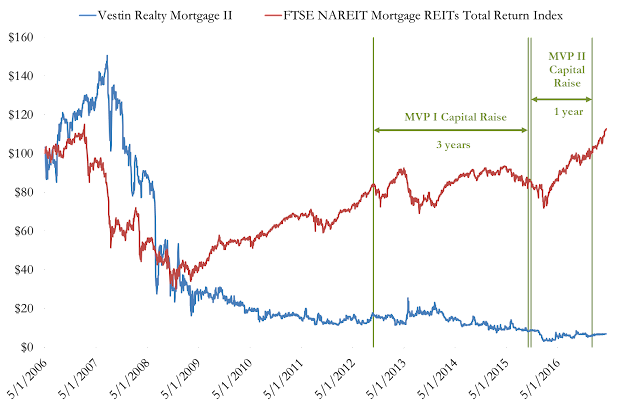

VRM II's maximum market capitalization was approximately $240 million. VRM II's total return from inception on May 1, 2006 to April 11, 2017 was -93%. During this same time period the total return to the FTSE Mortgage REIT Index was +13%. See Figure 4.

Figure 4. Vestin Realty Mortgage II (VRM II) Total Return

We have identified MVP I and MVP II's capital raise periods in Figure 4. Again, any brokerage firm considering selling either MVP I or MVP II, could have seen that investors in Mr. Shustek's VRM II had fared very badly both in absolute terms and relative to a more diverse set of mortgage REITs.

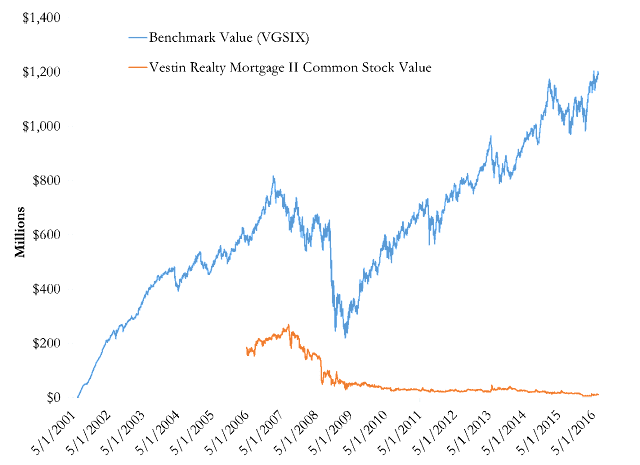

Figure 3 and Figure 4 don't capture the full extent of investor losses due to Mr. Shustek's VRM I and VRM II programs. VRM II had raised over $300 million net of redemptions before becoming Vestin Realty Mortgage II in 2006. Had those net amounts raised from investors been invested in a diversified portfolio of REITs proxied for by Vanguard's VGSIX fund, the investments would have been worth approximately $600 million when the VRM II shares were worth $180 million. Thereafter, the VGSIX shares that could have been purchased with the net amounts paid for Vestin Fund II / VRM II shares would have grown to be worth $1.233 billion while the VRM II shares are worth $0.012 billion. That is, the VRM II program has cost REIT investors $1.221 billion. See Figure 5.

Figure 5. Vestin Fund II / Vestin Realty Mortgage II (VRM II) Total Return

MVP REIT

MVP REIT is a non-traded REIT sponsored by MVP Capital Partners, LLC and advised by MVP Realty Advisors, LLC. MVP Capital Partners, LLC became owned by VRM I and VRM II. MVP REIT's SEC filings are available on the SEC website.

During three years of fundraising starting in September 2012, MVP REIT issued only $77 million of stock, or 14% of its proposed $500 million offering. Most of the $77 million in MVP REIT shares were issued to SERE Holdings controlled by Mr. Bradford in exchange for interests in six buildings. SERE Holdings then appears to have sold the shares to investors through a brokerage firm owned by Mr. Shustek.

MVP REIT II

MVP REIT II is a second non-traded REIT from MVP Capital Partners. It was registered in September 2015 and sought to raise up to $550 million in a one year period. As of September 30, 2016, the REIT had only raised $45 million, or 9% of its maximum offering amount. The Board of Directors extended the close of offering from October 1, 2016, to December 31, 2016, and announced $50 million preferred stock offering after the closing date of common shares offering was determined.

Entities Affiliated with Mr. Shustek and Mr. Bradford Repeatedly Bought and Sold the Same Properties from Each Other.

Between June 2013 and May 2016, entities affiliated with Mr. Shustek and Mr. Bradford bought and sold the same six buildings from each other on three separate occasions.xix As of May 2016, the net result of the repeated sales was a $9.2 million loss for VRM I and VRM II, plus commissions and closing costs.xx

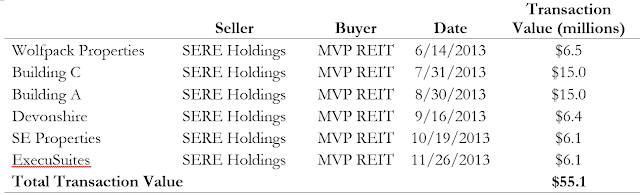

The First Sale

Between June 2013 and November 2013, SERE Holdings, of which Mr. Bradford was the managing member, sold Wolfpack Properties, LLC; Building C, LLC; Building A, LLC; Devonshire, LLC; SE Properties, LLC; and ExecuSuites, LLC to MVP REIT for $55.1 million (see Table 1).xxi Each LLC was a holding company for a single property. As part of the transactions, MVP REIT paid $1.7 million in acquisition fees to MVP Realty Advisors, a subsidiary of VRM II.xxii

Table 1. Summary of the Transactions in Round 1

MVP REIT paid SERE Holdings for the buildings by issuing 2.2 million shares of common stock valued at $19.5 million and assuming the buildings' mortgages ($35.6 million).xxiii In December 2013, just after SERE Holdings sold the last building to MVP REIT, the shares issued for the six buildings constituted 76% of all the equity capital raised by MVP REIT.xxiv

Interestingly, by March 2014, SERE Holdings had divested itself of 1.6 million shares of the non-traded MVP REIT (50% of MVP REIT's shares outstanding)xv without selling any of the shares back to MVP REIT and without selling more than 5% to any single investor. This is interesting because, in less than nine months, SERE Holdings sold more than 1.5 times the number of MVP shares that MVP REIT had issued to other investors since the beginning of its capital raise 18 months earlier (September 2012).

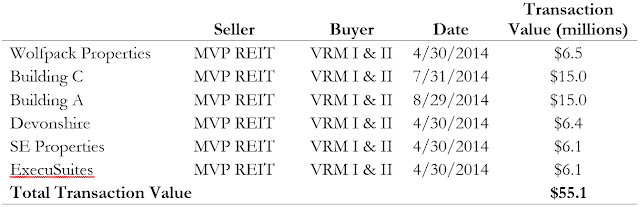

The Second Sale

Within one year of buying the six buildings from SERE Holdings, MVP sold all six buildings to VRM I and VRM II. In return, MVP received cash and interests in parking structures and storage facilities from VRM I and VRM II.xxvi As shown in Table 2, MVP sold the buildings to VRM I and VRM II at MVP's purchase price ($55.1 million). As part of the transaction, MVP paid $1.3 million in expenses to VRM I and VRM II.xxvii

One odd aspect of the second sale is that it ever happened. VRM I and VRM II are mortgage REITs, meaning they invest primarily in mortgages rather than actual real estate. After purchasing the properties, 80% of VRM II's assets were tied up in real estate.

Table 2. Summary of the Transactions in Round 2

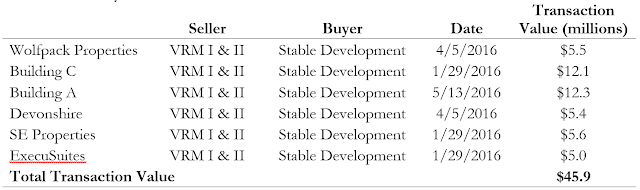

The Third Sale

Table 3 summarizes the third sale of the buildings. Between January 2016 and May 2016, VRM I and VRM II sold the same six properties to companies owned and managed by Stable Development, LLC. As part of the transactions, VRM I and VRM II paid $0.8 million in disposition fees to Vestin Mortgage.xxviii

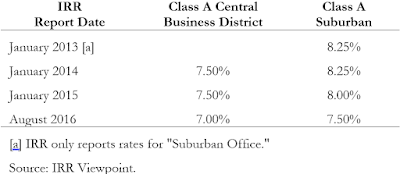

Stable Development was owned by Lance Bradford, who was also the managing member of SERE Holdings.xxix In other words, after the third sale, the properties belonged to the same person who sold them in the first round. However, despite rising values for office properties in Las Vegas (see Table 4),xxx VRM I and VRM II sold the properties back to an entity controlled by Mr. Bradford for $9.2 million less than the 2014 transaction prices.

Table 3. Summary of the Transactions in Round 3

Table 4. Capitalization Rates for Class A Office Property in Las Vegas, Nevada. Lower capitalization rates mean investors are willing to pay more for a building.

Repeatedly selling the six buildings makes little economic sense, and looks more like a shell game than transactions with economic substance. Together, the three rounds of buying and selling the properties transferred

$3.0 million from MVP REIT to VRM I and VRM II through fees,

$0.8 million from VRM I and VRM II to Michael Shustek through disposition fees, and

$9.2 million from VRM I and VRM II to Lance Bradford through reduced sales prices.

Given rising commercial real estate values in the Las Vegas office market, it appears that either MVP REIT acquired the shares at an inflated price, or VRM I and VRM II sold the shares at a sub-market price - or both.

A Possible Fourth Sale

The sales of the six buildings to Stable Development in 2016 included provisions allowing VRM I and II to repurchase each building within one year, at a 12% mark-up.xxxi Just before the repurchase options began expiring in January 2017, VRM I, VRM II, and Stable Development revised the repurchase agreements.xxxii The new purchase agreement allows VRM I and VRM II to acquire 100% of Stable Development-whose only assets are the six buildings-from two entities for $16.8 million plus the outstanding debt on the six buildings.xxxiii If Stable Development did not pay down any of the mortgages, the revised repurchase agreement allows VRM I and VRM II to acquire the six buildings for $38.6 million (a 16% mark-down from the previous sale price).xxxiv

Shortly after VRM I and VRM II sold the six buildings for a $9.2 million loss-but before the repurchase agreement was renegotiated, VRM II proposed a 1:1,000 reverse stock split.xxxv VRM II required that partial shares (i.e., investors with fewer than 1,000 pre-split shares) be bought out by the company. It is curiously serendipitous that VRM II took what turned out to be a temporary loss equal to 60% of its equity market capitalization at a time when Mr. Shustek and other large shareholders of VRM II would benefit from lower share prices.xxxvi In the six months before the reverse split was announced, Mr. Shustek increased his holdings from 19.9% to 21.5% of VRM II. The reverse split, by eliminating smaller shareholders, would further increase his holdings to 25.5%.xxxvii Together, the $9.2 million loss and the renegotiated repurchase agreement transferred more than $1 million in wealth from small VRM II shareholders to Mr. Shustek and other large VRM II shareholders.

Conclusion

VRM I, VRM II, MVP REIT I, and MVP REIT II illustrate the perils of non-traded REITs in which control persons can direct transactions for their benefit with little or no regard for the harm they cause retail investors.

The extreme disregard shown by control persons for investors in these registered investments also highlights the potential risks associated with proposals to allow easier sale of unregistered investments to retail investors.

_______________________________________

i "An Empirical Analysis of Non-Traded REITs," Journal of Wealth Management, Summer 2016, vol. 19(1). iiForm 10-K for 2015, VRM II REIT, filed with the SEC on 3/30/2016. Page 13. iiiForm 10-K for 2014, VRM II REIT, filed with the SEC on 3/31/2015. Page 20. iv Mr. Shustek's ownership percentages are from an MVP REIT prospectus dated 4/16/2015. v Mr. Bradford's ownership of Stable Development is from VRM II's 2015 10-K, filed on 3/30/2016 (p. 12). SERE Holdings' ownership of the six LLCs is from MVP REIT's 2013 10-K (pp. 86-87). viForm 8-K, MVP REIT I, filed with the SEC on 1/7/2016. viiForm 10-K for 2013, MVP REIT, filed with the SEC on 3/31/2014. Page 86. viii Form 10-Q for 3Q 2014, VRM I REIT, filed with the SEC on 11/13/2014. Page 6. ixForm 10-Q for 3Q 2014, VRM I REIT, filed with the SEC on 11/13/2014. Page 6; Form 10-Q for 3Q 2014, VRM II REIT, filed with the SEC on 11/13/2014. Page 8; Form 8-K, MVP REIT I, filed with the SEC on 3/11/2013. x German, Jeff, "Official targeted in FBI probe linked to firm he supervised," Las Vegas Review-Journal, February 24, 2016. xi VRM I and VRM II also loaned $3.7 million to MVP Capital Partners II (the sponsor for MVP REIT II) in 2015 and 2016. Those loans were also completely impaired in the same quarter they were made. xii Form 10Q for 2Q 2014, MVP REIT, filed with the SEC on 8/13/2014. Page 17. xiiiForm 10-Q for 3Q 2004, Vestin Fund I, filed with the SEC on 8/9/2004 (p. 23). xivForm 10-Q for 3Q 2014, VRM I REIT, filed with the SEC on 11/13/2014. Page 6; Form 10-Q for 2Q 2005, Vestin Fund I, filed with the SEC on 2/8/2006. Page 21. xv Todd Prince wrote about VRM II's plans to deregister in two news articles for the Las Vegas Review-Journal: "Real estate investor Shustek proposing to delist company" on January 13, 2017, and "Vestin property fund plans to delist by end of month" on March 9, 2017. xviForm 10-K for 2015, VRM II REIT, filed with the SEC on 3/30/2016; xviiForm 10-K for 2002, Vestin Fund II, filed with the SEC on 9/27/2002. Page 20. xviiiForm 10-Q for 3Q 2014, VRM II REIT, filed with the SEC on 11/13/2014, (p. 45); Form 10-K for 2005, Vestin Fund II, filed with the SEC on 9/13/2005, (p. 45). xix Eight entities owned and or controlled by Mr. Bradford and Mr. Shustek lease space in Building A, located at 8880 West Sunset Road, Las Vegas, NV 89148. xx VRM II owned 72% of each of the six buildings, suggesting VRM II lost approximately $6.6 million (72% * $9.2) from the purchase and sale of the six buildings. xxiForm 10-K for 2013, MVP REIT, filed with the SEC on 3/31/2014. Pages 42-44. xxiiForm 10-K for 2013, MVP REIT, filed with the SEC on 3/31/2014. Pages 42-44. xxiiiForm 10-K for 2013, MVP REIT, filed with the SEC on 3/31/2014. Pages 42-44. xxivForm 10-K for 2013, MVP REIT, filed with the SEC on 3/31/2014. Page 2. xxvForm 10-K for 2013, MVP REIT, filed with the SEC on 3/31/2014. Page 102. xxviiForm 10-K for 2013, MVP REIT, filed with the SEC on 3/31/2014. Page 62.

xxviiForm 10-K for 2014, MVP REIT, filed with the SEC on 3/31/2015. Page 88.

xxiiiForm 10-Q for 3Q 2016, VRM II REIT, filed with the SEC on 11/10/2016. Pages 18-20.

xxxForm 10-K for 2015, VRM II REIT, filed with the SEC on 3/30/2016 (p. 12); Form 10-K for 2013, MVP REIT, filed with the SEC on 3/31/2014 (p. 86).

xxxi IRR Viewpoint annual report published in January 2013, January 2014, January 2015, and a mid-year update published in August 2016. We focus on the going-in cap rates of Class A office properties in Las Vegas.

xxxiiForm 10-Q for 3Q 2016, VRM II REIT, filed with the SEC on 11/10/2016. Pages 18-19.

xxxiii Apparently, between the time VRM II sold the buildings to Stable Development and January 2017, Lance Bradford sold or transferred his ownership interest in Stable Development to Par 3 Nevada, LLC and DT GRAT CS, LLC. Par 3 Nevada is managed by Lance Bradford. DT GRAT CS is managed by Dennis Troesh.

xxxiv Balances for each building's debt outstanding are from VRM II REIT's Form 8-K filed with the SEC on 2/3/16 and VRM II REIT's Form 10-Q for 3Q 2016 filed on 11/10/2016 (p. 18).

xxxv The first mention of the 1:1,000 reverse split in VRM II's SEC filings was on September 15, 2016.

xxxvi On December 31, 2014, VRM II had market cap of $10.417 million (2.578 million shares outstanding and a share price of $4.04) and a book value of $28.916 million. A $6.6 million loss in 2015 is 63% of the $10.417 million market cap.

xxxviiForm 10-K for 2015, VRM II REIT, filed with the SEC on 3/30/2016; Proxy Statement, VRM II REIT, filed with the SEC on 1/17/17.