Options Strategies Embedded in Exchanged Traded Products

May 2013

In theory, exchange traded products (ETPs) can be linked to almost any underlying asset, including derivatives. While many ETPs are linked to portfolios of bonds or stocks, some are linked to portfolios of futures contracts, which we have discussed at length before. Bill Luby at VIX and More has written a coupleposts on ETPs that are linked to portfolios of options, which are gaining some traction with investors. As usual, we greatly enjoyed Bill's posts and thought we'd explain some of the mechanics behind the option strategies embedded in these ETPs. More information about the basics of options can be found in our blog post titled "The Basics of Options Contracts".

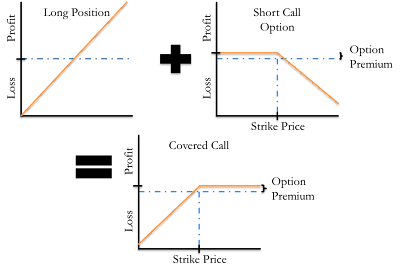

The first strategy we'd like to talk about is referred to as a "covered call" or "buy-write". This is the strategy implemented by PowerShares S&P 500 BuyWrite ETF (PBP), iPath CBOE S&P 500 BuyWrite Index ETN (BWV), Credit Suisse Gold Shares Covered Call ETN (GLDI), and most recently, Credit Suisse Silver Shares Covered Call ETN (SLVO). In options parlance, a covered call refers a position that is both long some asset and short a call option on that asset: the short call is 'covered' by the long position in the underlying asset. The figure below explains the profit and loss of this combined position graphically.

The covered call strategy generates income by selling call options (thus earning the option premium), but in doing so misses out on any increase in the value of the asset above the call strike. This strategy is particularly effective in markets without significant appreciation (since the investor would miss out on said appreciation) or depreciation (since the option premium would provide little protection against losses). Generally speaking, the closer the strike price is to the current asset price, the more income is generated and more upside potential is lost.

Another closely related strategy that has been implemented in ETPs is the put-write strategy. One ETP that implements this strategy is theALPS US Equity High Volatility Put Write (HVPW). You might have noticed that the covered-call strategy looks very much like a short put option. Well, that is the essence of the put-write strategy. The strategy sells put options and profits when the put options expire worthless. This strategy has gained significant attention since the CBOE began publicizing the PUT index (noting that the PUT index returned a staggering 1150% compared to the S&P 500 returning 800% between 1986 and 2012).

What makes these ETPs interesting is that it gives investors a way to invest in moderately complex option strategies without really understanding their mechanics. If an investor wanted to implement a covered call on their own, they'd have to worry about when (and how) to sell the call, when to cover the short position and rolling the position forward periodically (repeating this process all over again). ETPs wrap this process up into (a perhaps too easily) digestible package.