In a lot of our research work, we break down complex financial products into simpler pieces and then value those simple pieces one at a time. Often, those smaller components are options contracts (especially in our structured product work), which are relatively easy for practitioners to value. However, options contracts use a peculiar terminology that can be confusing to the uninitiated, so we thought we would lay out exactly what we mean when we talk about options.

Options contracts are derivatives that give the holder the right, but not the obligation, to purchase or sell a security at a specified price on a specified date (or dates). The price specified in the contract is known as the option's strike price and the last date the option can be exercised is known as the option's expiration. The buyer of an option pays the seller -- who is called the option writer -- a premium for the right specified in the contract. Options can be traded in a standardized exchange-traded format -- such as on the Chicago Board Options Exchange (CBOE) -- or in customizable over-the-counter bilateral agreements.

Options that can only be exercised at maturity are called European options -- S&P 500 index options on the CBOE, for example -- and options that can be exercised at any time prior and on the options expiration are called American options -- equity optionson the CBOE, for example. Other types of options exist, but these two are by far the most common.

Options that give the holder the ability to purchase at a specific price are called call options whereas options that give the holder the ability to sell at a specific price are called put options.

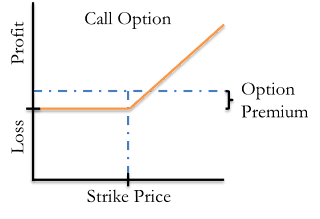

Call Options

Buyers of call options believe that the asset on which the option is written will appreciate in value prior to the expiration of the option. If the asset is more valuable than the strike price specified in the option contract, the option holder can exercise their right to buy the underlying asset at the strike price from the option seller and then sell the asset at the current market price to realize a profit.

If the asset is less valuable than the strike price, the holder of the option is not obligated to exercise the option andwill simply allow it to expire. The following schematic summarizes the profit and loss (or payoff) a call option buyer can realize as a function of the underlying asset price upon exercise of the option.

Call option buyers only realize a profit if the underlying asset is worth more than the strike by at least the option premium. Buyers of call options can lose at most the option premium (if the underlying asset is below the strike at expiration) but can realize any level of profit.

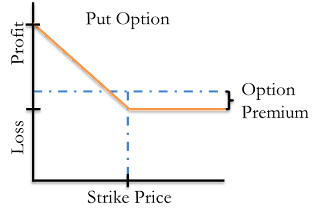

Put Options

Buyers of put options, on the other hand, believe that the underlying asset will depreciate in value prior to the expiration of the option. If the asset is less valuable than the strike price specified in the option contract, the option holder can buy the underlying asset at the current market price and then exercise their right to sell the underlying asset at the strike price to realize a profit.

If the asset is less valuable than the strike price, the holder of the option will simply allow the option to expire -- the option holder is not obligated to exercise the option. The following schematic summarizes the profit and loss (or payoff) a put option buyer can realize as a function of the underlying asset price upon exercise of the option.

Put option buyers only realize a profit if the underlying asset is worth less than the strike price by at least the option premium. Since the underlying asset can not be worth less than zero, put option buyers have limited profit potential (at most realizing the strike price less the option premium) and, like call option buyers, can lose at most the option premium.

Of course, sellers of calls and puts have the opposite payoffs--a seller of a call option profits if the asset does not appreciate more than the option premium, and a seller of a put profits if the asset does not depreciate more than the the option premium. Sellers are said to be short a call or put whereas buyers are said to be long the option.

American and European puts and calls are the most prevalent type of options contracts, but many more exotic types of contracts exist, such as barrier and binary options. We hope to cover these in depth in later posts, as they are important in understanding structured products like reverse convertibles and dual directionals.