We have significantly updated our working paper on dual directional structured products (or simply dual directionals). Since our first version of the paper, our work has been covered by RISK.net and in November of 2012 RISK.net named a dual directional as their trade of the month. The latest version of the paper is available from the SLCG website and SSRN.

In this version of the paper, we expanded our scope by studying all dual directionals registered with the SEC since 2008. We divide dual directionals into two broad categories: knock-out dual directionals (KODDs) and single observation dual directionals (SODDs). KODDs have a final payoff that depends on the linked assets value throughout the term of the note while SODDs have a payoff that depends only on the linked asset's value at the final valuation date. For an example KODD, see JP Morgan's SEC filing for their product linked to the S&P 500. For an example SODD, see Morgan Stanley's SEC filing for a product linked to Apple stock.

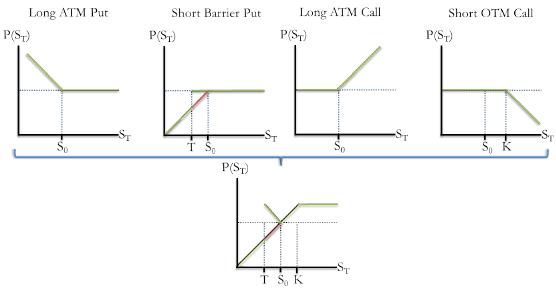

KODDs have embedded barrier options that encode the dependence on the linked asset's price. These products can be decomposed as follows:

Our sample included 38 KODDs and we found that on average these products were worth approximately $0.973 per dollar invested on their issue date (lower than the principal investment minus the average underwriting fee of $0.0133).

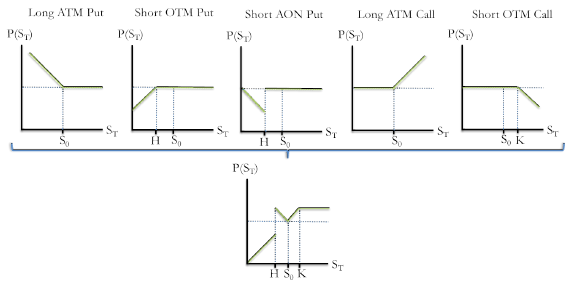

SODDs have embedded binary options that lead to discontinuities in the final payoff for the dual directional. These products can be decomposed as follows:

We valued 65 SODDs and found that their average issue date value was approximately $0.957 -- again, less than $1 minus the average stated fee of $0.0159.

The current version of the paper also expands on the first version by including downside leverage (a feature offered by some SODDs). This feature is essentially equivalent to the buffer in buffered notes.

Dual directionals are interesting because these products embed a straddle position into a structured product and because issuers have begun to issue these products more frequently in recent months. Like most structured products, the notes are exceedingly complex for retail investors and are often priced at a premium to the present value of the options embedded in them.