Persistence and Mean Reversion in VIX Rolling Futures Indexes

Mar 2013

In our last post we followed up on Jason Voss's discussion of the Hurst exponent as a measure of persistence or mean reversion in market data. We compared the Hurst exponents of the S&P 500 to that of the VIX index, and found that the S&P 500 is largely a random signal (Hurst exponent near 0.5) but that the VIX exhibits characteristics of a 'switching' or mean reverting signal (a Hurst exponent between 0 and 0.5).

Much has been made of VIX mean reversion in the financial blogosphere. One idea is that if you could purchase the VIX when it is at historical lows--such as we have seen recently--then you could profit from its eventual reversion to its historical mean (a level of approximately 20). However, the VIX isn't an investible index, so most people who want 'volatility exposure' look to VIX options, VIX futures, and increasingly to VIX exchange-traded products which essentially wrap these derivatives into a convenient package.

We have two papers on volatility exchange-traded products ("The VXX ETN and Volatility Exposure" and "Are VIX Futures ETPs Effective Hedges?"), and one of our main points is that these products do not behave like the VIX itself. The details are a bit complicated, but in essence these products mimic a strategy of continuously buying and selling VIX futures. The transaction costs involved with this strategy can significantly affect returns. The most popular volatility exchange-traded product is an ETN known as VXX, which currently has a market cap over $1 billion.

Just looking at these two time series suggests that they exhibit different persistence properties; specifically, VXX seems persistent (downward) and VIX seems more mean reverting. We decided to see what the Hurst exponent says about these two signals.

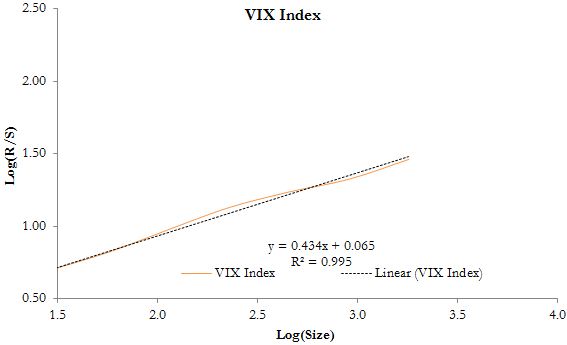

The underlying index that VXX tracks is known as the S&P 500 VIX Short-Term Futures Index Total Return(or SPVXSTR), which has data going back to late 2005. If we calculate the Hurst exponent of the VIX index over this period, we obtain a similar result to what we had found before, namely that the VIX index exhibits mean reverting properties (though somewhat less so than over the longer time period previously considered):

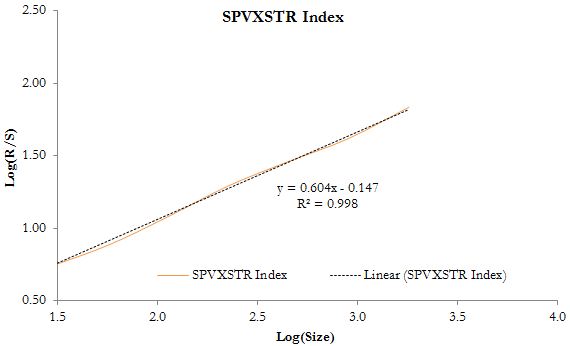

SPVXSTR, however, exhibits persistent behavior, with a Hurst exponent of 0.60*:

These results--though limited by a relatively short time period--suggest that the VIX index has different time series properties thanSPVXSTR and that using SPVXSTR to take advantage of mean reversion in the VIX may not be an effective strategy. These results mirror those of our paper on hedging the S&P 500 with volatility products (PDF), which finds that while the VIX itself may be have useful hedging properties, volatility exchange-traded products do not.

_______________________________________

* We also calculated the Hurst exponent of theS&P 500 VIX Mid-Term Futures Index Total Return (SPVXMTR) and obtain a Hurst exponent of 0.61 over the same time period.