We've talked a lot on this blog about collateralized debt obligations (CDOs), including a post just last week about how they might be regaining popularity. We thought it might be worthwhile to step back and explain just what a CDO is and why it is considered such a risky investment.

Part of the complexity just has to do with terminology. CDOs are a type of asset-backed security; so like a derivative, the value of a CDO is linked to the value of another asset. Typically, CDOs are linked to an entire portfolio of assets, called the collateral, and for CDOs that collateral is usually corporate debt (hence, 'collateralized debt obligation'). There are numerous other types of asset-backed securities that follow a similar pattern: if the collateral is a portfolio of loans, they are called collateralized loan obligations (CLOs), if they are mortgages, collateralized mortgage obligations (CMOs, also known as mortgage-backed securities or MBS), and so on.

When a traditional pooled-asset investment such as a mutual fund sells shares, each share is equally risky. If the portfolio of assets loses 5%, each share in turn loses 5% in value. This is referred to as a 'pass-through' security. The way CDOs work is by selling different levels of risk to different investors. A single CDO might issue several different types of securities (called 'tranches') that bear losses not together, but in turn.

This structure has what's referred to as a 'waterfall' of payments. As the underlying portfolio generates income, investors are paid their share of that income in a distinct order: senior investors are paid first, mezzanine investors are paid next, and equity investors are paid last. The senior and mezzanine investors are paid fixed interest rates (say, 5% and 7%, respectively), but the equity investors are entitled to whatever remains after those payments.

If the collateral generates more income than expected, the equity investors get extra distributions; if it generates less, they be paid smaller distributions, or perhaps none at all. At maturity, the same process happens with the value of the portfolio as a whole: proceeds from selling the pool of assets are used to pay back the principal of the senior investors first, mezzanine investors next, and equity investors with the remainder.

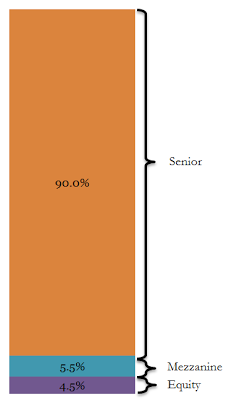

But what makes CDOs especially risky is what happens when there are losses or defaults in the portfolio. To see this, consider a simplified $1 billion CDO with a $900 million senior tranche, $55 million mezzanine tranche, and $45 million equity tranche:

Because of the waterfall structure, equity investors are in what is known as the 'first loss' position. If the portfolio as a whole loses $10 million (1%), equity investors lose $10 million of their $45 million investment, or 22%. If the portfolio loses $50 million (5%), equity investors are completely wiped out, and mezzanine investors lose $5 million. Senior investors only lose value if the losses exceed the combined value of the equity and mezzanine tranches below them, or in this case $100 million. As noted by former Federal Reserve Chairman Alan Greenspan, the "risk per dollar of notional amount of the "first loss," or equity, tranche can be thirty or forty times the risk per dollar of the senior tranche."

Equity tranches are especially risky. While they can generate extra income when the portfolio of assets yields greater than expected returns, they have very leveraged exposure to losses and can be completely wiped out with even relatively small percentage losses in the collateral--as was the case in the 2007 Banc of America CLOs we have discussed before. But in the depths of the 2008 financial crisis, even senior tranches bore considerable losses.

Of course, the higher the quality of the underlying collateral, the less likely CDO investors are to suffer losses. However, we argue that CDOs are so complex and their risks so difficult to evaluate that they are almost always unsuitable for retail investors.