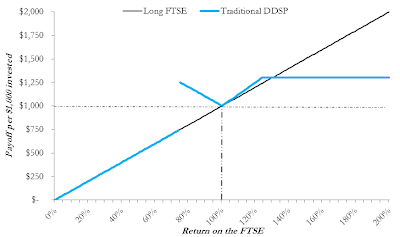

Generically speaking, DDSPs pay out a positive return if the underlying index or stock linked to the product changes in value (appreciates or depreciates) within a specified range. DDSPs do not offer principal protection, but typically offer leveraged and capped exposure to upside returns as well as buffered exposure to downside returns (see figure below). We studied these structured products in depth in a recent research paper and noted that these products typically offer investors less than 95 cents per dollar invested.

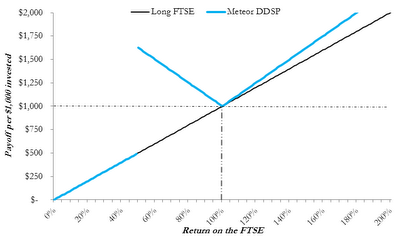

The cap is used by the DDSP issuer to finance the positive returns investors are owed if the underlying asset decreases in value but remains above the barrier level. A few things that makes the Meteor product interesting is (1) the lack of a cap, (2) the leverage on both the upside and the downside, and (3) the extremely long term of the product--over six years. Also, while the product is branded and issued by Meteor, the guarantor is Morgan Stanley and as a result investors will be exposed to Morgan Stanley's credit risk.

To understand how this product works, consider an initial investment of $10,000. If the FTSE 100's level on November 2, 2018 is:

greater than the FTSE 100's level on 11/2/2012, then the product pays back principal plus 1.25 times the appreciation (if any) of the FTSE 100. For example, if the FTSE 100 increased by 40%, the product would pay $10,000*(1+1.25*40%) = $15,000.

less than the FTSE 100's level on 11/2/2012, but greater than the barrier level -- equal to 50% of the FTSE 100's 11/2/2012 level -- then the product pays back principal plus 1.25 times absolute value of the depreciation (if any) of the FTSE 100. For example, if the FTSE 100 decreased by 20%, the product would pay $10,000*(1+1.25*|-20%|) = $12,500.

less than the barrier level, then the product loses value at a rate of 1% for each percentage decline in the level of the FTSE 100 since 11/2/2012. For example, if the FTSE 100 decreased by 60%, the product would pay $10,000*(1-60%) = $4,000.

A graph of the possible total returns an investor could expect to experience as a function of the final level of the FTSE 100 is given below.

We have modeled this product, taking into account the credit risk of Morgan Stanley as well as the other product specific parameters, and have found that this product is worth approximately 96 cents per dollar invested. That's pretty typical for DDSPs and structured products in general, but we should note that this is a valuation after upfront fees, which according to the offering documents could be as much as 7%.

So despite the very unique features of this product that could seem attractive, the extremely long term of the investment (and thus significant credit and inflation risk) make this 'Trade of the Month' pretty typical of what we have seen before.