Each month we review BREIT's Performance webpage to see what NAV it claims for the prior month end. After two years' absence, a grossly misleading graphic reappeared yesterday. In fact, Blackstone has made this renewed misrepresentation even worse.

Two and a half years ago, we started a series of posts outlining problems with BREIT.

In December 2022, we predicted a run on BREIT and then in April 2023 we identified 7 major areas in which we believe Blackstone and BREIT have been misleading investors.

Blackstone's Choice: Let BREIT Crash or Collapse It Slowly? can be found here.

Blackstone Fiddles as BREIT Burns can be found here.

In Blackstone is Watching Us and Just Admitted a Major Misrepresentation, available here, we pointed out that BREIT appeared to acknowledge that its claimed after-tax yields and tax-equivalent yields were inflated approximately by 25% for every breit.com/performance/e webpage report for the six month-ends September 30, 2022 through March 31, 2023.

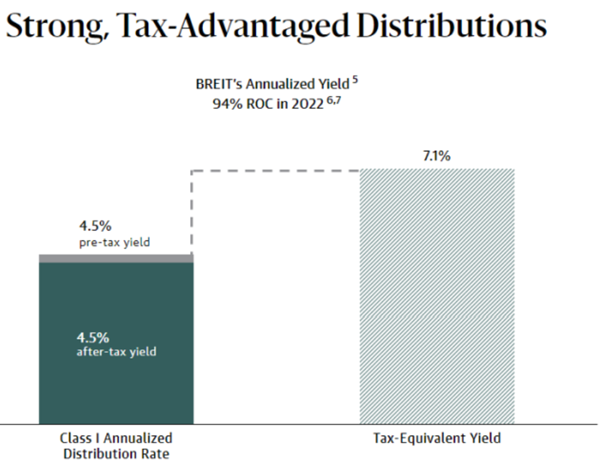

Figure 1 is a screen shot of the misleading graphic on BREIT's Performance page in early 2023 based on distributions as of December 31, 2022.

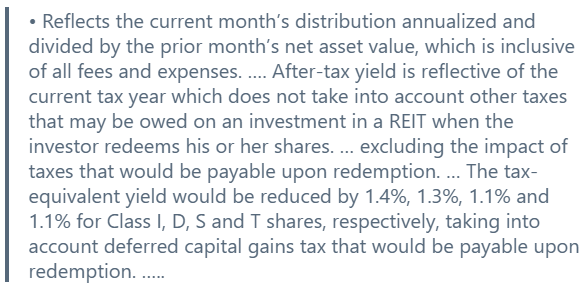

The graphic reports an after-tax yield of 4.5% and a tax-equivalent yield of 7.1%. Neither representations are true and neither are footnoted. Instead, if you dig into the footnotes - footnote 5 in particular - you can start to see BREIT's mischief. Footnote 5 reads in part.

BREIT claimed an after-tax yield that ignored the capital gains taxes which, at a minimum, would be due in the future on the distributions which were largely being treated as a return of capital. In the footnote, a highly skeptical, highly sophisticated reader might figure out that BREIT's prominent graphic is false and the tax equivalent yield on the I shares is 5.7% since the footnote says the tax equivalent yield in the graphic - 7.1% - would have to be reduced by 1.4% to account for the taxes due. Moreover, the footnote does nothing to correct BREIT's claim that the after-tax yield is 4.5%. By the same logic the footnote opaquely and partially discloses the truth about the tax-equivalent yield, the after-tax yield on the I shares was 3.6% not 4.5%.

On May 1, 2023, we linked to a Reuters story on BREIT's announcement of April redemption requests and commented that BREIT's misleading claimed tax-equivalent yield requires a huge "just kidding" asterisk. BREIT pulled this misleading graphic within a day or two of when we called it into question.

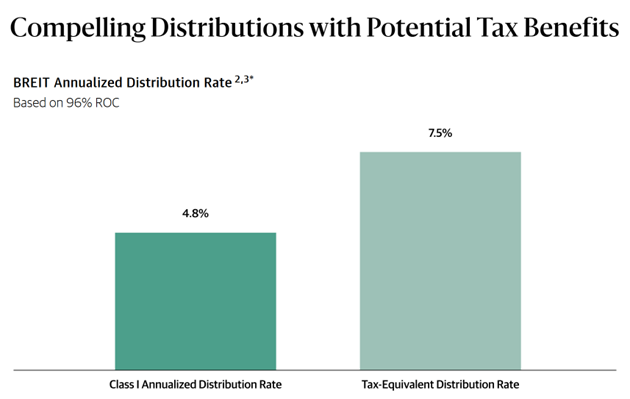

BREIT Brings the Misrepresentation Back After a Two-Year Hiatus

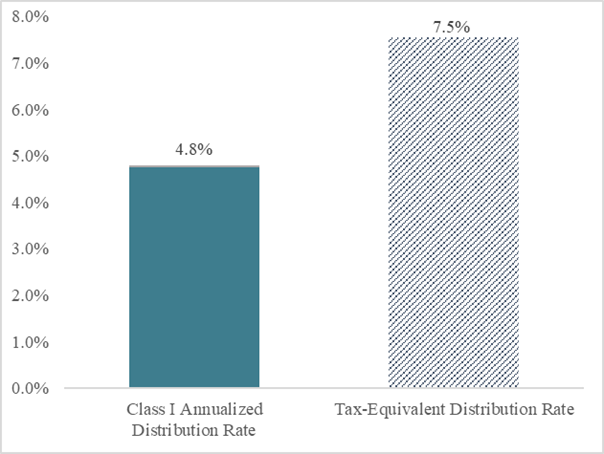

Figure 2 BREIT's Misleading Performance Graphic Re-emerges On May 15, 2025

This graphic is trivially different than the graphic Blackstone dropped after we pointed out how misleading it was. "Annualized Distribution Rate" and "Tax-Equivalent Distribution Rate" have replaced "Annualized Yield" and "Tax-Equivalent Yield" but the fundamental misrepresentation has returned. Also, the claimed "After-tax Yield" has been removed.

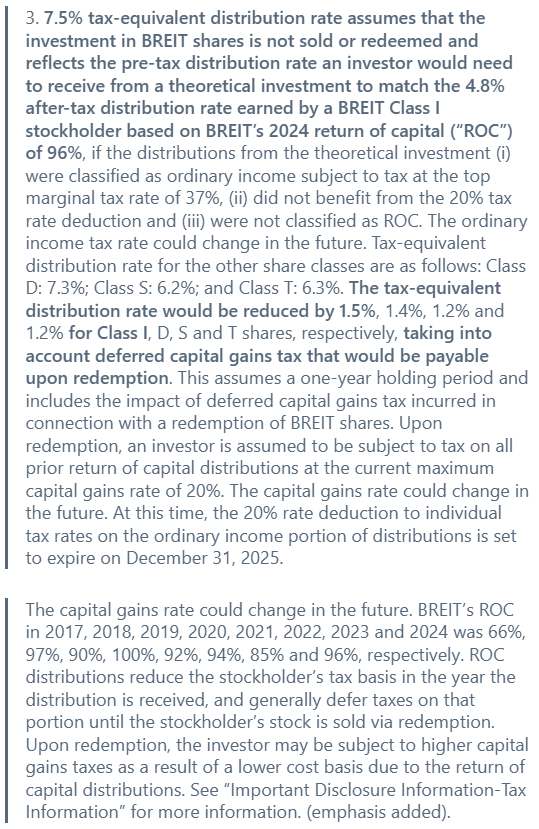

Footnote 3 reads in its entirety:

Figure 3 is our recreation of BREIT's current graphic. We calculate the 7.5% "Tax-Equivalent Distribution Rate" by first applying the 20% capital gains tax rate to only 3.73% of the 4.789% annualized distribution (BREIT rounded this to 4.8%) and 0% tax on the remaining 96.27% of the 4.789% distribution rate. This tax application reduces the distribution by 0.036% - from 4.789% to 4.753%. In the previous iteration of this misleading graphic, (BREIT had plotted this result in the graphic and referred to it as an after-tax yield.) Next, we gross up the 4.753% by the assumed 37% ordinary income tax rate. This is done by dividing 4.753% by 0.63 resulting in 7.545%, which BREIT rounded to 7.5%. See Figure 3.

Figure 3 BREIT's Deceptive Illustration

BREIT's 7.5% tax equivalent annualized distribution rate is not tax-equivalent to the 4.8% figure which includes 20% capital gains tax on only 3.73% of the distributions and no tax at all on the remaining 96.27% of the distributions.

It's quite challenging to read BREIT's footnote 3 and understand what the illustration's 7.5% means. The very first sentence of footnote excerpted above is false. The 4.8% distribution rate is not an after-tax distribution rate anymore than BREIT's previous incarnation's "after-tax yield" in Figure 1 above was an after-tax yield. Traditionally, we would fully tax the distributions (the other 96.27%) at the 20% capital gains tax rate which BREIT acknowledges will be due on these distributions when the stock is sold and gross up the resulting after tax amount by the higher, 37%, ordinary income tax rate.

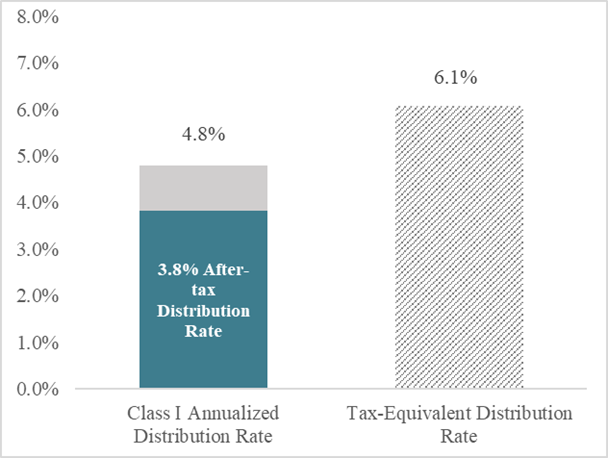

In this instance, applying the 20% capital gains rate to all of the 4.789% distribution rate, we get 3.83%, which when divided by 0.63 to gross up for the 37% ordinary income tax rate results in a 6.1% tax equivalent distribution rate. See Figure 4.

Figure 4 Closer to the Truth

Unlike BREIT's Figure 2 which we reproduce in Figure 3, the calculations in Figure 4 have a coherent meaning. BREIT distributes 4.8% per year, mostly tax-deferred. Assuming all of the distributions are eligible for the 20% capital gains tax rate, what distribution rate subject to a 37% ordinary income tax rates would provide the same after-tax distributions? The answer is 6.1% not 7.5% as claimed by BREIT. Buried in footnote 3, BREIT actually admits the graphic is false when it writes: "The tax-equivalent distribution rate would be reduced by 1.5%, 1.4%, 1.2% and 1.2% for Class I, D, S and T shares, respectively, taking into account deferred capital gains tax that would be payable upon redemption."

Once called out for this deception and removing it two years ago, why did BREIT chose to bring it back yesterday?