You can download a pdf of this article to print or email here.

BREIT this week eliminated a prominent marketing graphic touting inflated after-tax yields and tax-equivalent yields after we pointed out that it was false and misleading.

In December 2022 we predicted a run on BREIT and then in April 2023 we identified 7 major areas in which we believe Blackstone and BREIT have been misleading investors.

Blackstone's Choice: Let BREIT Crash or Collapse It Slowly? can be found here.

Blackstone Fiddles as BREIT Burns can be found here.

In addition to these two significant notes, I have posted and briefly commented periodically as BREIT announced monthly redemption requests at the beginning of the month and NAVs around the 20th of the month.

BREIT recently appears to have acknowledged that its claimed after-tax yields and tax-equivalent yields were inflated approximately by 25% for every webpage report for the six month-ends September 30, 2022 through March 31, 2023.

On May 1, 2023, I linked to a Reuters story on BREIT's announcement of April redemption requests and commented:

On May 1, 2023 when I made this comment, BREIT's Performance webpage displayed a graphic claiming a false after-tax yield and false tax-equivalent yield. This graphic and the false yields first appeared in October 2022 on the BREIT.com/performance webpage reporting the September 30, 2022 NAV and performance statistics.

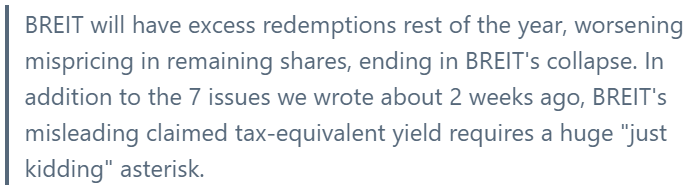

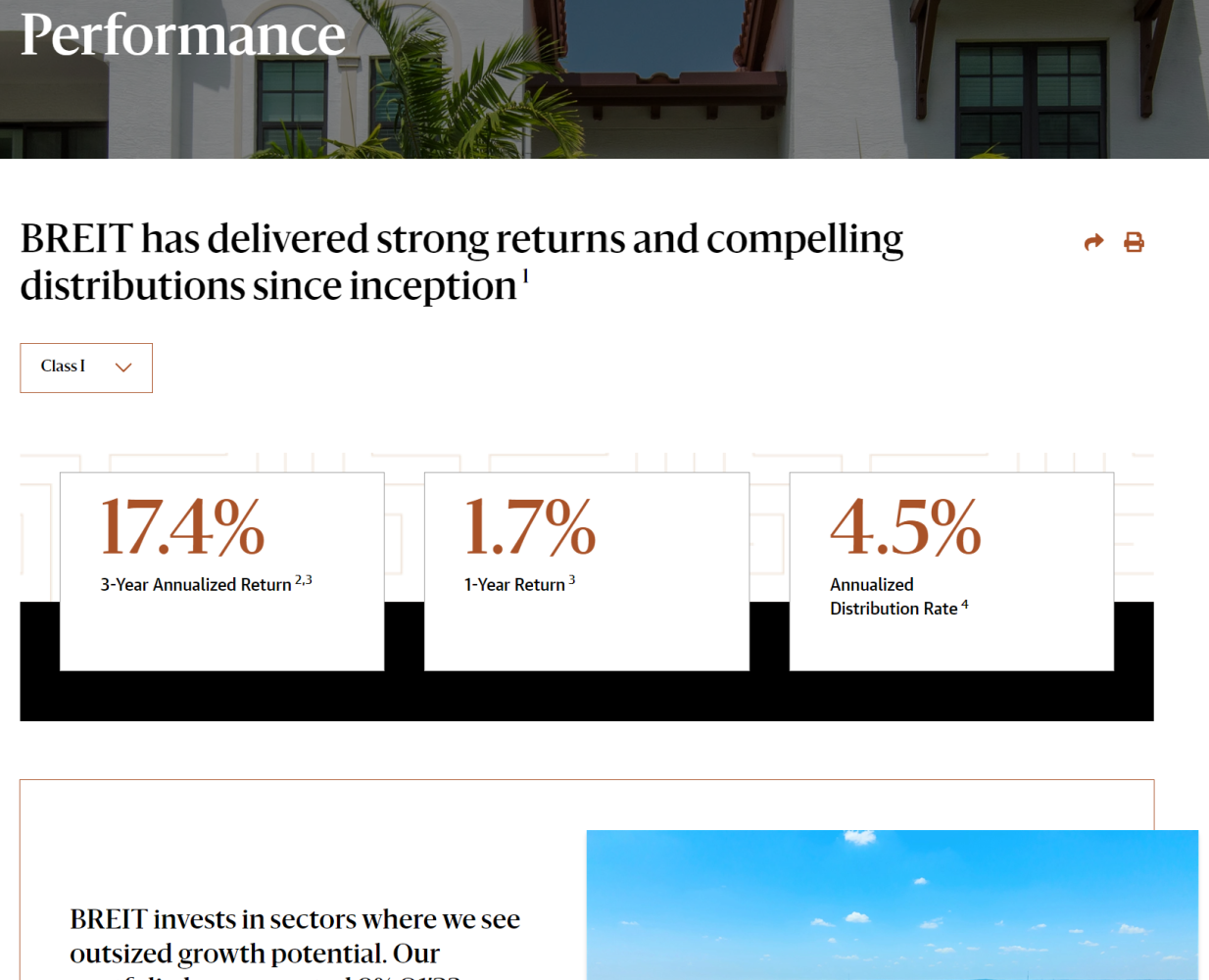

The image in Figure 1 is the top of BREIT's Performance webpage in late April and early May when we commented that BREIT's tax equivalent yield was false. Unfortunately, the wayback machine did not capture this page in late April or early May so we'll have to work with this image we saved at the time for now. We had selected "Class S" in the drop down box and so the graphic reported a 3.7% pre-tax, 3.6% after-tax and 5.7% tax equivalent yield as we took this screen shot.

Figure 1. BREIT.com\Performance on May 1

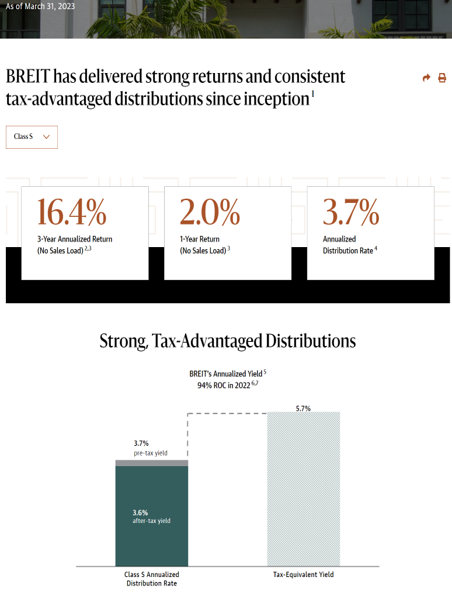

Lost now to the ether, when Class I was the default share class displayed by BREIT, the graphic looked like Figure 2. BREIT claimed a 4.5% after-tax yield and a 7.1% tax-equivalent yield as of March 31, 2023.

Figure 2: BREIT.com/performance as of March 31, 2023, claimed May 1, 2023

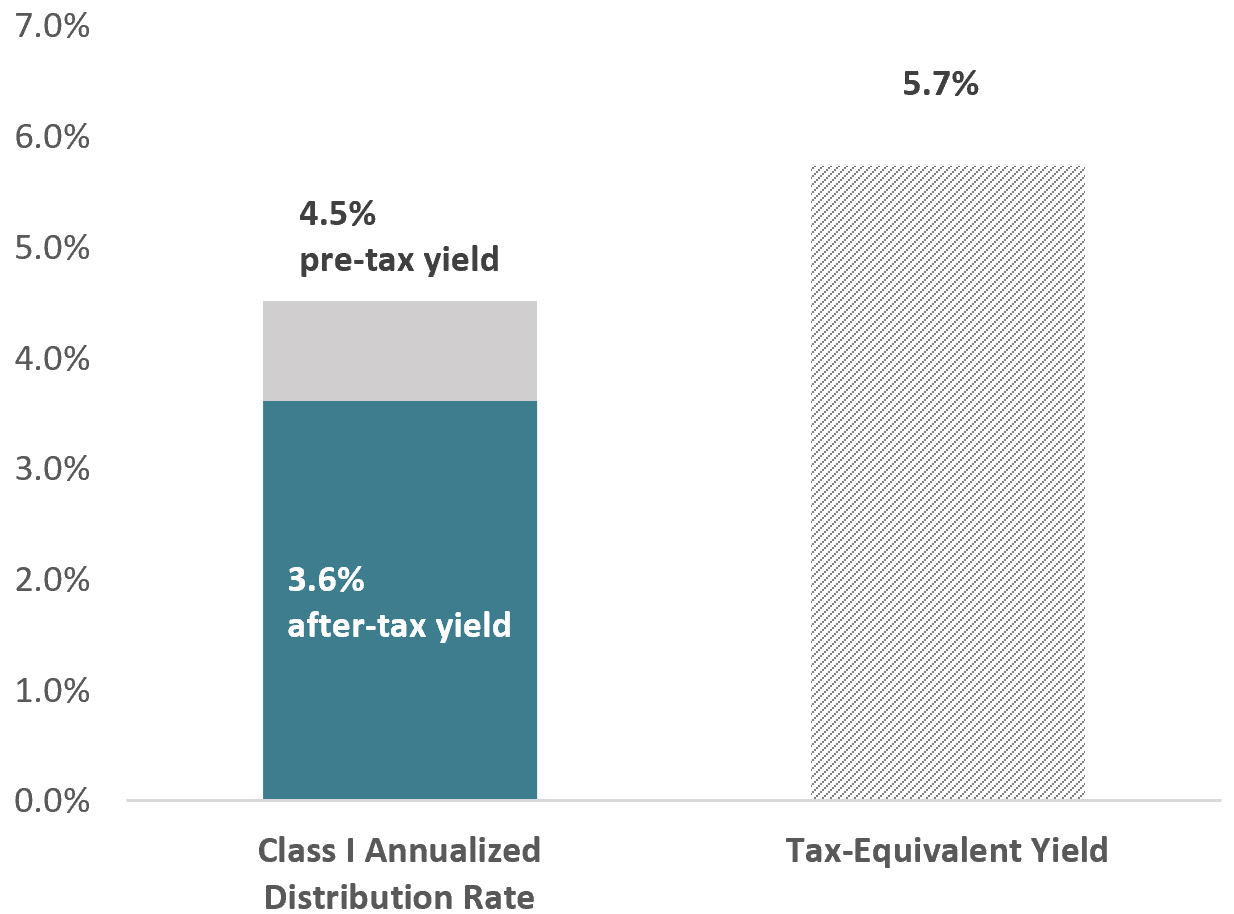

The correct after-tax yield as of March 31, 2023 for the I shares was no more than 3.6%, not 4.5% as BREIT claimed and the tax-equivalent yield for the I shares was no more than 5.7%, not 7.1% as BREIT claimed.

Because we didn't save the full www.BREIT.com/Performance page on May 1 and the wayback machine didn't archive it, we will explain BREIT's mischief using BREIT's BREIT.com/performance webpage as of February 4, 2023. [here]

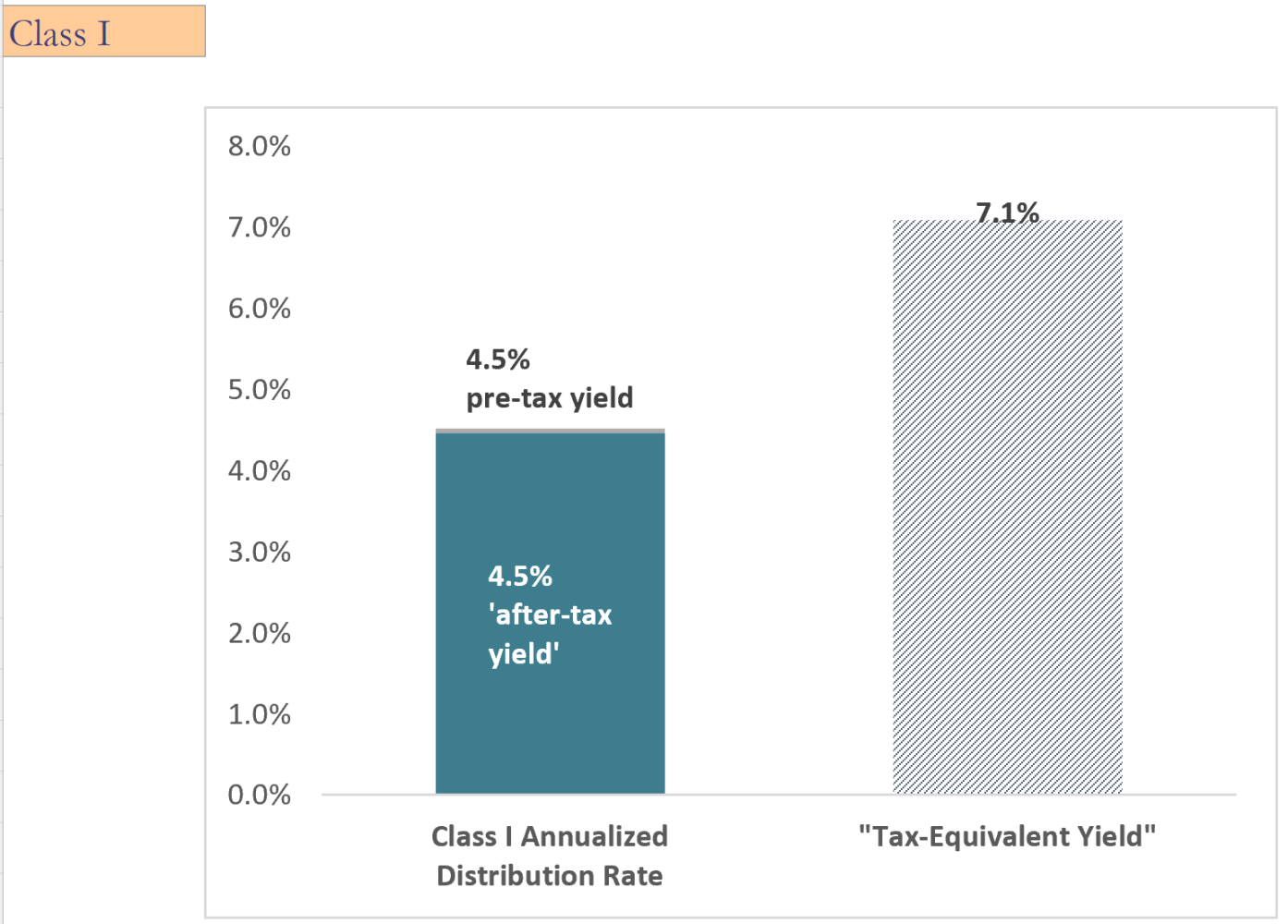

The image in Figure 3 is the top of BREIT's Performance webpage as captured by the wayback machine on February 4, 2023. BREIT's webpage reports results as of December 31, 2022 because BREIT had not yet reported the January 30, 2023 NAV.

Figure 3. BREIT.com\Performance on February 4, 2023

The graphic reports an after-tax yield of 4.5% and a tax-equivalent yield of 7.1%. Neither representations are true and neither are footnoted. Instead, if you dig into the footnotes - footnote 5 in particular - you can start to see BREIT's mischief. Footnote 5 reads in full.

Reflects the current month's distribution annualized and divided by the prior month's net asset value, which is inclusive of all fees and expenses. Annualized distribution rate for all share classes: Class S: 3.6%; Class T: 3.7%; Class D: 4.4%; Class I: 4.5%. After-tax yield is reflective of the current tax year which does not take into account other taxes that may be owed on an investment in a REIT when the investor redeems his or her shares. After-tax yield for all share classes: Class S: 3.6%; Class T: 3.7%; Class D: 4.3%<; Class I: 4.5%. Tax-equivalent yield herein reflects the pre-tax yield an investor in a theoretical taxable investment would need to receive to match the after-tax yield of BREIT's applicable class share in the current tax year assuming that (i) all income earned on the theoretical fixed income investment is taxed at the top ordinary rate of 37% and (ii) 94% of BREIT's distributions are treated as a return of capital ("ROC"), which is equal to the percentage of BREIT distributions classified as ROC for 2022, and excluding the impact of taxes that would be payable upon redemption. he ordinary income tax rate could change in the future. Tax-equivalent yield for the other share classes are as follows: Class D: 6.8%; Class S: 5.7%; and Class T: 5.8%. The tax-equivalent yield would be reduced by 1.4%, 1.3%, 1.1% and 1.1% for Class I, D, S and T shares, respectively, taking into account deferred capital gains tax that would be payable upon redemption.This assumes a one-year holding period and includes the impact of deferred capital gains tax incurred in connection with a redemption of BREIT shares. Upon redemption, an investor is assumed to be subject to tax on all prior return of capital distributions at the current maximum capital gains rate of 20%. The capital gains rate could change in the future. Other fixed income products with different characteristics, such as municipal bonds, may also provide tax advantages. The availability of certain tax benefits, such as tax losses from other investments, may also increase the after-tax yield of other fixed income products for an investor. Investors should consult their own tax advisors. See "Important Disclosure Information-Tax Information". [Bold and underline emphasis added]

BREIT claimed an after-tax yield that ignored the capital gains taxes which, at a minimum, would be due in the future on the distributions which were largely being treated as a return of capital. In the footnote, a highly skeptical, highly sophisticated reader might figure out that BREIT's prominent graphic is false and the tax equivalent yield on the I shares is 5.7% since the footnote says the tax equivalent yield in the graphic - 7.1% - would have to be reduced by 1.4% to account for the taxes due. Moreover, the footnote does nothing to correct BREIT's claim that the after-tax yield is 4.5%. By the same logic the footnote opaquely and partially discloses the truth about the tax-equivalent yield, the after-tax yield on the I shares was 3.6% not 4.5%.

Figure 4. BREIT's corrected After tax yield and tax equivalent yield on I shares as of December 31, 2022

BREIT filed a 424(b)(3) with the SEC two days ago reporting its NAV. BREIT also updated its performance page and removed the false and misleading after-tax and tax-equivalent yield graphic which had been at the very top of the performance webpage for six months.

Figure 5. BREIT this week eliminated the false and misleading graphic touting inflated after tax yields and tax equivalent yields

It appears that Blackstone and BREIT are paying attention to what Regina and I have to say. :)