You can download a pdf of this article to print or email here.

In late 2022 we analyzed BREIT and concluded that BREIT had been systematically inflating its NAV, smoothing its returns and misleading investors. The intervening 18 months have confirmed our opinions.

We focused on BREIT because it was a juggernaut and a poster child for the nontraded REIT industry trying to rebuild after its prior "lifecycle" flimflam was no longer tenable in the face of overwhelming evidence of investor harm. Also, BREIT was roughly 4 times the size of the next largest monthly-NAV REIT, Starwood REIT.

Starwood REIT recently caught our notice. We believe that Starwood REIT's NAV was inflated and its returns smoothed and that much else of what we said concerning BREIT applies to SREIT. What caught our eye last week though was a grossly misleading SREIT performance claim we called BREIT out over almost a year ago and which BREIT promptly stopped making. To our surprise, SREIT continues to make exactly the same misleading claim - only worse - prompting this post.

Before we discuss SREIT, let's recap our BREIT posts.

On December 9, 2022, we reported on our early research into BREIT in Blackstone's Choice: Let BREIT Crash or Collapse It Slowly? available

here.

We predicted that BREIT would either meet redemptions and collapse quickly or limit redemptions and watch its NAV drop as much as 35% relative to traded REITs. At the time, BREIT's latest reported NAV was October 30, 2022. This morning, BREIT reported its March 31, 2024 NAV. Between October 30, 2022 and March 31, 2024, BREIT has limited redemptions and its NAV has dropped 10% relative to traded REITs. BREIT's latest NAV is lower than it was nearly 30 months ago but still too high. We expect the slow-motion collapse of BREIT to continue until its NAV falls another 20% or more relative to traded REITs.

A year ago this week, we identified at least seven areas where Blackstone has lacked candor in Blackstone Fiddles as BREIT Burns available

here.

1) Performance reporting. BREIT's 10-Ks include a statement that its monthly NAV calculations are not reliable for calculating performance. Nonetheless, BREIT and Blackstone's SEC filings prominently include BREIT returns calculated based on the unreliable NAV.

2) Performance touting. BREIT's website displays historical performance based on its unreliable NAV calculations on a page entitled simply "Performance". Many of BREIT's and Blackstone's press releases and presentations include strong, unqualified statements about BREIT's historical performance based on the NAVs which BREIT's 10-Ks state are not reliable for calculating performance.

3) Asset and Performance Incentive Fees. Blackstone has received $4.2 billion in asset management and performance incentive fees based entirely on its calculation of BREIT's NAV. Blackstone justified nearly $2 billion in performance incentive and asset management fees in 2021 alone by claiming a 30% return for the year based on a NAV which BREIT's 10-Ks state can not be used to calculate performance.

4) NAV calculations. BREIT failed to disclose the critical revenue growth assumption - assumption just as critical as the discount rate and cap rate "key" assumptions it disclosed for 72 months - until November 2022 as things appear to be coming off the rails.

5) 2022 Returns. BREIT's 2022 monthly returns were smooth and positive while traded REITs' prices dropped 29%. BREIT falsely attributed this yawning gap to its concentration in residential and industrial property sectors which fell by roughly the same amount in 2022 as the traded REIT market as a whole. BREIT's 2022 returns were in fact created by increasing assumed net operating income growth rates and lowering assumed discount rates and cap rates in its DCF model when the rising general level of interests indicated the need to do exactly the opposite.

6) Redemptions. In December 2022, for the first time BREIT imposed redemption limits that it had waived three times before. BREIT chose to not enforce limits until BREIT's NAV was likely significantly overstated. Contrary to its justification for limiting redemptions, BREIT could easily have met redemptions without selling properties but, if the NAV was overstated, redeeming shareholders at stated NAVs would increase the mispricing in remaining shares.

7) University of California Investment. Blackstone made a sweetheart deal with the University of California, effectively selling the University of California BREIT shares at a 20% discount. Blackstone would not make this deal if it was confident in BREIT's NAV and could defend the BREIT franchise without paying $1 billion.

In Blackstone is Watching Us and Just Admitted a Major Misrepresentation available here

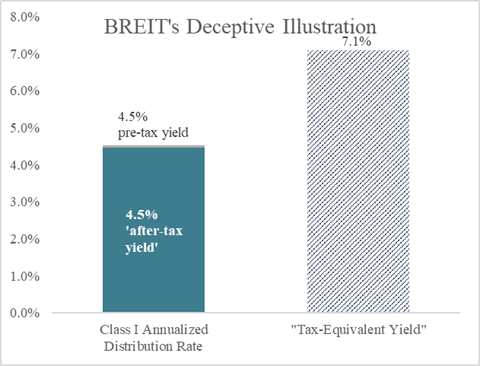

we reported that BREIT eliminated a prominent marketing graphic touting inflated after-tax yields and tax-equivalent yields after we pointed out that it was false and misleading.

BREIT had claimed an after-tax yield that only accounted for current year taxes. Since BREIT's distributions are treated as mostly or entirely return of capital for tax purposes, there were no capital gains or ordinary income to be taxed in the current year but those distributions lowered the cost basis against which capital gains would be calculated. BREIT ignored the capital gains which would be paid in the future as a result of treating prior distributions as a return of capital in its misleading prominent graphic.

Even worse, in this graphic, BREIT claimed a "tax equivalent yield" by dividing this phony after-tax yield by 1 minus an assumed 37% ordinary income tax rate. These after-tax and tax-equivalent yields weren't footnoted but if you dug into other footnotes you could see BREIT knew its graphic was dishonest.

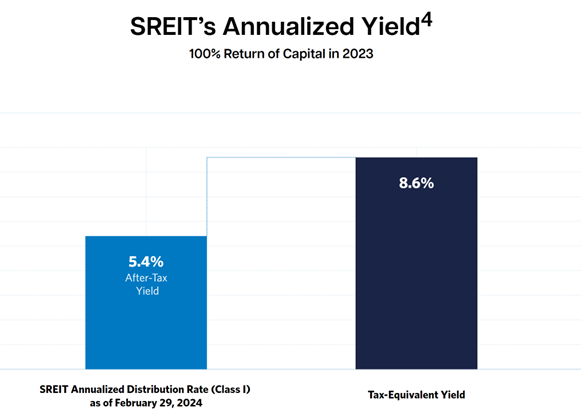

Starwood REIT Persists in Using the Same Deceptive Graphic

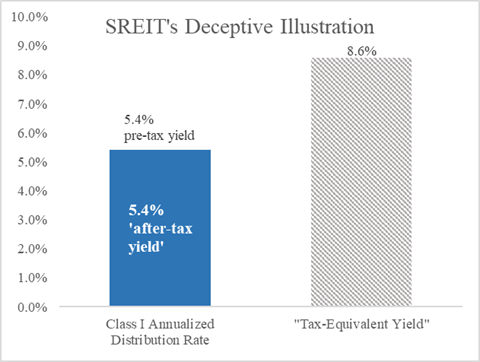

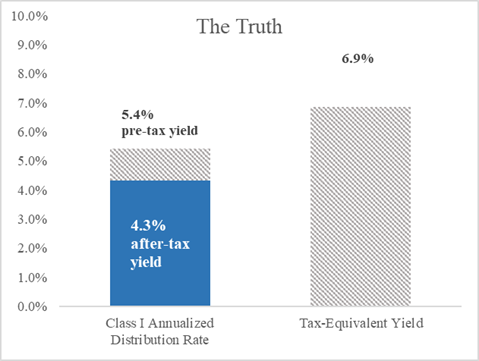

Without rehashing everything we wrote about BREIT which also applies to SREIT, SREIT's deceptive claims of past returns are a good marker for other problems. SREIT's current performance (here) webpage includes this prominent, and false, graphic.

SREIT misrepresents after-tax and tax-equivalent yields in a prominent graphic.[1] In a hidden footnote it acknowledges that it is ignoring the taxes in its "after-tax" yield and then grossing up this phony after-tax yield by an assumed tax rate.

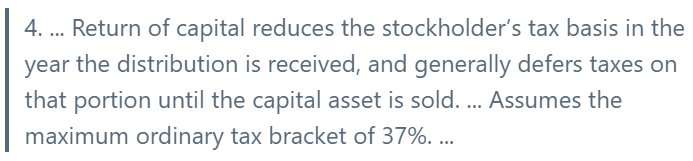

There are footnote numbers on this page including "4" on the graphics title but there are no visible footnotes on the page. At the bottom of this "Performance" page there is, in vanishingly small print, "Summary of Risk Factors / Footnotes" banner. Clicking on this banner, footnotes appear including footnote 4 which reads in part:

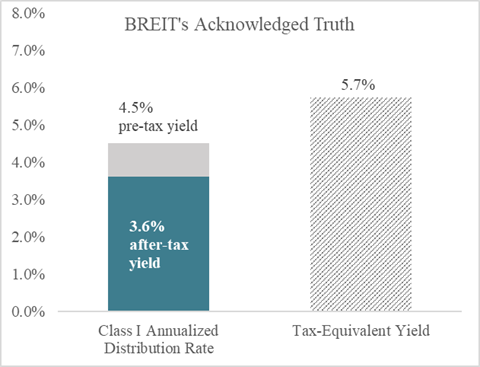

BREIT was concerned enough with misleading investors, or at least was concerned enough about being caught doing so, that in its footnotes BREIT admitted the after tax yield was really 3.6%, not 4.5% and the tax-equivalent yield was 5.7% not 7.1%. Even so, once we pointed out BREIT's wildly misleading after-tax and tax equivalent yield claims were, BREIT stopped.

Eleven months after we pointed out BREIT's deception and BREIT's correction, SREIT continues to make even more deceptive claims after-tax and tax equivalent yield claims using the same graphic and a much less honest footnote. SREIT should drop its graphic or make it more truthful. The after tax-yield is 4.3%, not 5.4%, assuming a capital gains tax rate of only 20% and ignoring state capital gains taxes. The tax-equivalent yield is 6.9%, not 8.6%.