You can download a PDF copy of this post to print or email here.

You can download an Excel file containing some of our analysis of Aegis' sole underwritten offerings

here.

Introduction

Aegis Capital is one of the worst few retail brokerage firms based on complaints and investors should avoid it at all costs. You can see our recent post on bad brokerage firms here

2024 Brokerage Firm Risk Rankings

In addition to its retail brokerage business, Aegis Capital serves as an underwriter. Since 2010, Aegis has been the sole underwriter of 186 offerings for 111 issuers totaling $1.9 billion.

The stocks were issued by nano stock companies constantly on the verge of delisting and bankruptcy, kept afloat only by Aegis's willingness to sell these failing firms' worthless stock to its customers

and to the customers of other brokerage firms.

Aegis-underwritten offerings were bought into Aegis's retail brokerage clients' accounts and were re-traded in Aegis' retail brokerage clients' accounts at significant markups and markdowns.

In addition, Aegis served as a market maker for many of the stocks it underwrote receiving bid ask spread revenue as a result of trades its brokers were strongly motivated to recommend.

Aegis provided inflated research analyst coverage for many of the stocks it underwrote, providing relentlessly aggressive buy recommendations with stratospheric price targets even as the stock

prices of virtually all the companies it underwrote plummeted close to $0.

Aegis's roles as retail brokerage firm, underwriter, market maker and research analyst created a farm-to-table securities fraud supply chain.

Aegis underwrote a series of offerings which systematically and predictably failed in exchange for extraordinary compensation. Investors, including many Aegis' retail customers,

suffered at least $3.0 billion in losses as a result of Aegis' conduct.[1]

Not only did Aegis underwrite, make a market in, and recommend worthless stocks, in many cases, Aegis and the Issuers increased the number and size of the offerings by aggressively interpreting

limitations on issuances. Shockingly, in at least three instances, Aegis either marked the close or looked the other way while others marked the close to facilitate underwritings.

Aegis Capital's Underwritten Offerings

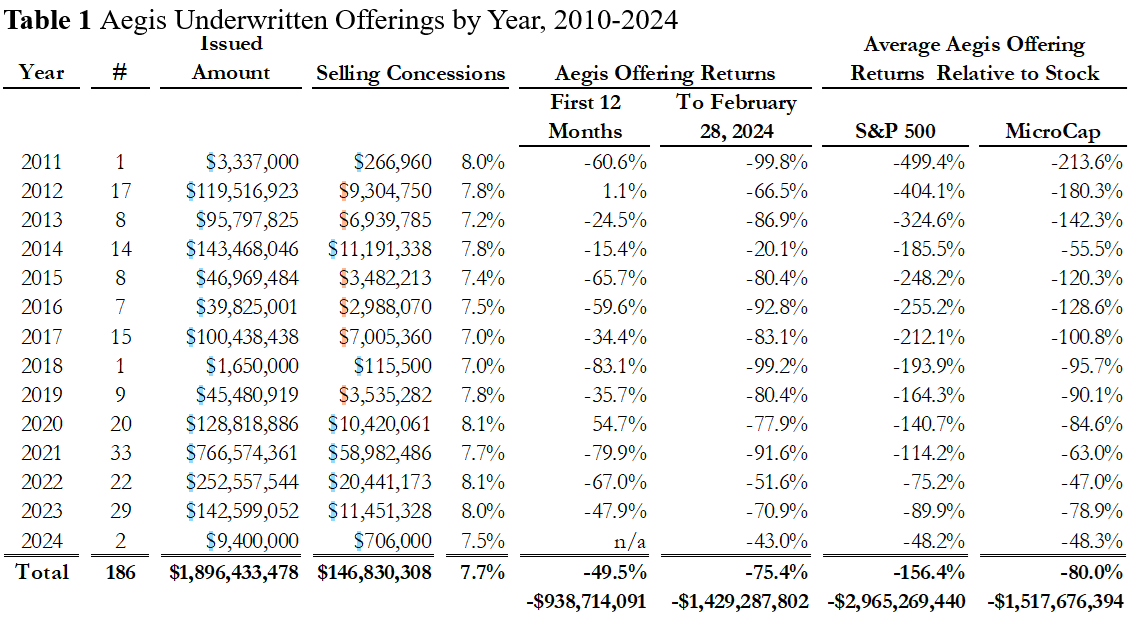

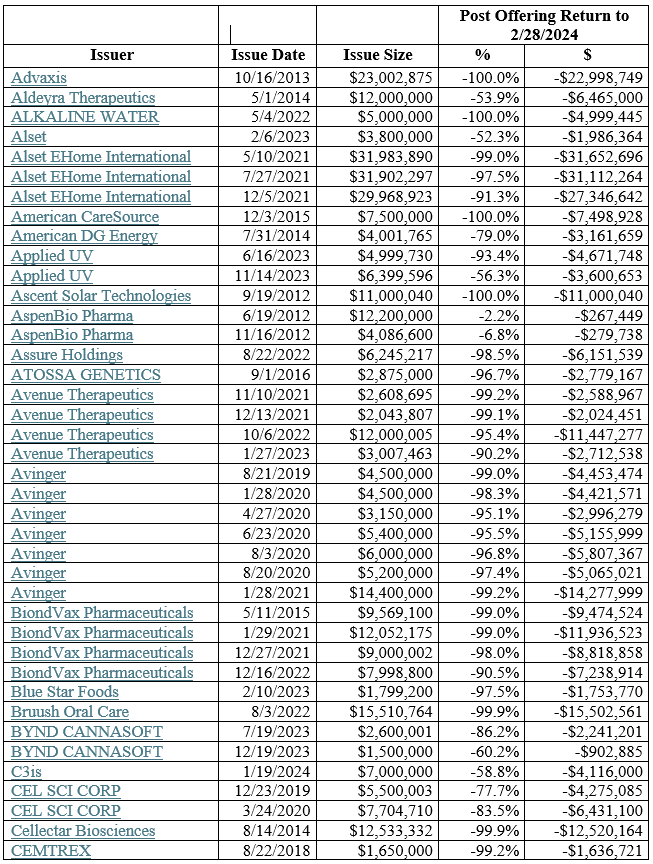

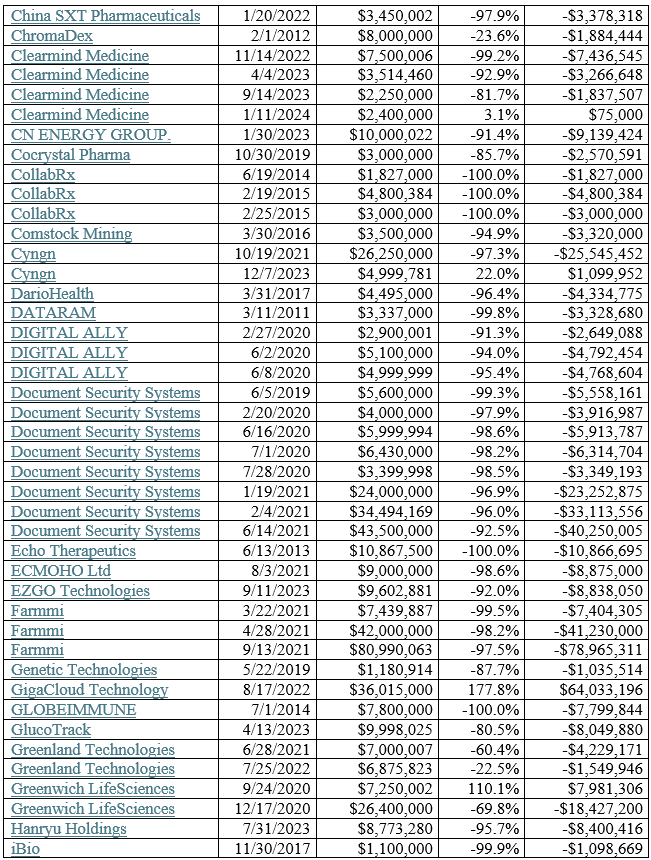

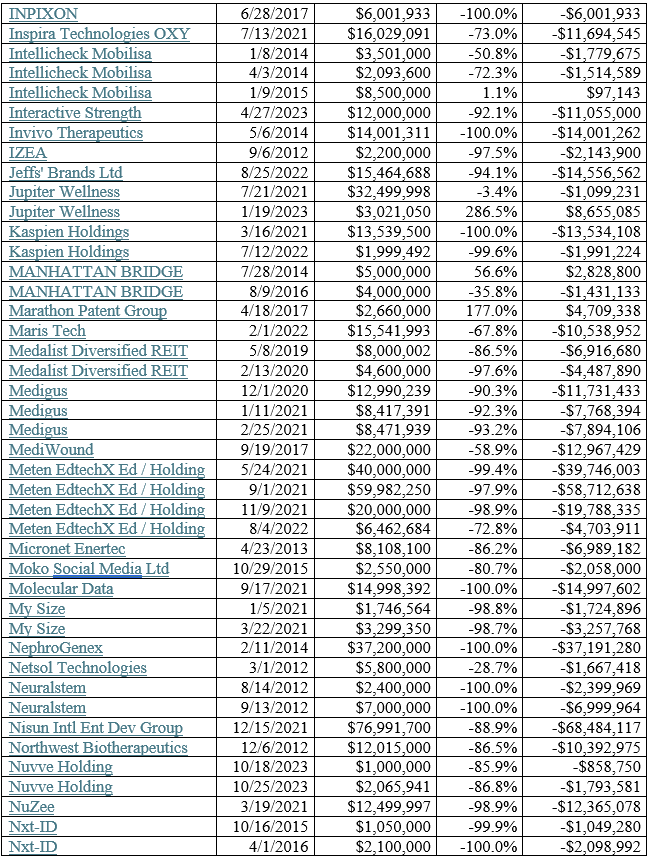

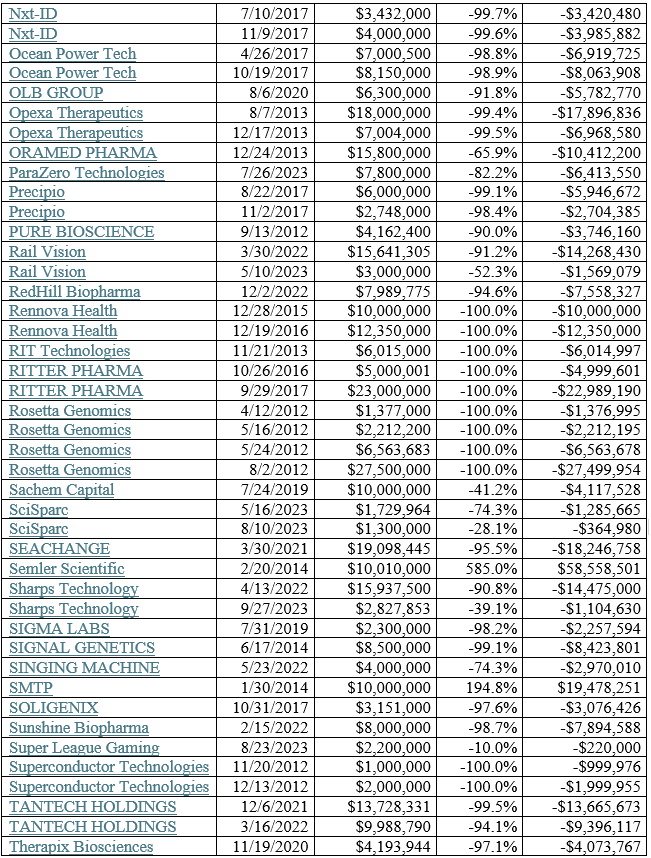

Aegis Capital's sole-underwritten offerings are listed in Appendix 1 below. The issuers names are hyperlinked to the Form 424(b)s for each issuance. Table 1 reports the number and dollar value of

Aegis sole-underwritten offerings by year from 2011 to early February 2024. The number and dollar values increased significantly over time.

The weighted average 12 month return following an Aegis underwriting is -49.5%.

The weighted average 12-month return in each year is negative except 2020; even those offerings went on to lose 77.9% on average and underperform the S&P 500 by 140.7% and microcap stocks by 84.6%.

Investors lost $938,714,091 of the $1,896,433,478 invested in the first twelve months after an Aegis underwritten offering.

The weighted average return to February 28, 2024 across Aegis underwritings is -75.4%.

Investors lost $1,429,287,802 of the $1,896,433,478 invested in the Aegis underwritten offerings by February 28, 2024.

174 (93.5%) of the 186 Aegis issues have negative returns. Only 12 (6.5%) of the 186 Aegis issues have positive returns.

177 (95.2%) of the 186 Aegis issues have lower returns than microcap stocks. Only 9 (4.8%) of the 186 issues have higher returns than microcap stocks.

179 (96.2%) of the 186 Aegis issues have lower returns than S&P 500 stocks. Only 7 (3.8%) of the 186 issues have higher returns than S&P 500 stocks.

The summary numbers presented in Table 1 understate the harm done to investors by Aegis's underwriting activity up through February 28, 2024. In addition to the $1.5 billion decline in value of

securities Aegis underwrote, and the $1.5 billion in underperformance compared to the overall stock market, investors likely unnecessarily paid at least $1.5 - $2.0 billion in markups, markdowns

and bid ask spread trading these worthless securities.

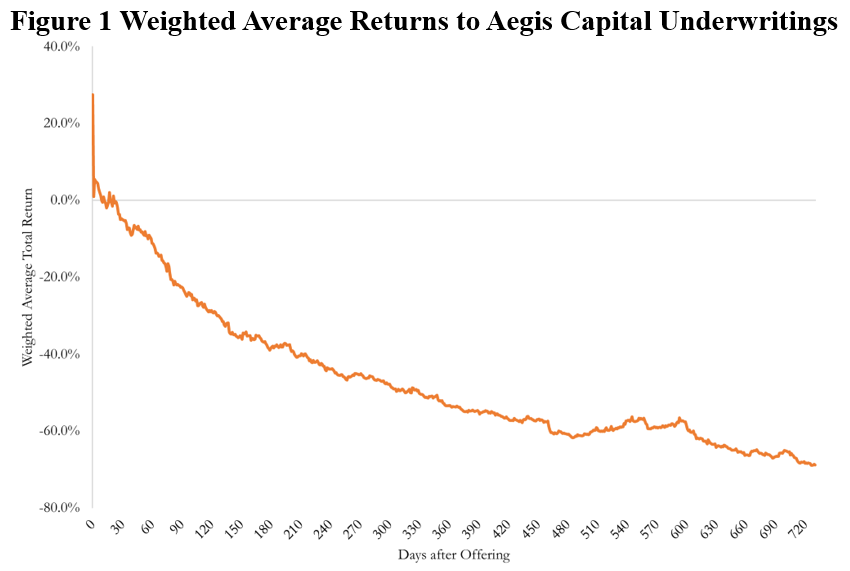

Figure 1 plots the weighted average return to all Aegis offerings for the first two years after an offering.

The dramatic underperformance of Aegis's underwritten offerings is not because Aegis underwrote micro-cap issuers when micro-cap issuers in general suffered losses or because of general market forces.

The -75.4% weighted average return to Aegis underwritten offerings is 80.0% worse than the +4.6% weighted average return to the Dow Jones U.S. Micro-Cap Total Stock Market Index.

Investors lost $1,429,287,802 in the Aegis underwritten offerings when they would have made $88,388,592 investing in microcap stocks.

The -75.4% weighted average return to Aegis underwritten offerings is 156.4% worse than the +81.0% weighted average return to the S&P 500.

Investors lost $1,429,287,802 in the Aegis underwritten offerings when they would have made $1,535,981,638 investing in S&P 500 stocks.

Invitation to Mischief in Underwritings

Instructions for S-3 and F-3 registrations require that an offering be no more than 1/3rd the value of issuers' shares held by unaffiliated investors less the dollar value of stock previous sold to

the public in the prior 12 months if the market value of shares held by unaffiliated investors is less than $75 million.

The instructions appear to invite issuer and underwriter abuse by allowing the value of shares held by unaffiliated investors to be calculated by multiplying the current shares held by nonaffiliates

by the highest closing price in the prior 60 days.[2] Underwriters and Issuers have an incentive to overstate the number of shares held by nonaffiliates and to search for, even manufacture, the highest

possible price over the prior 60 days. It is common in the Aegis underwritings for the issuer's stock price to have been declining significantly over the prior 60 days and so the "1/3rd of value of

shares held by nonaffiliates" cap as calculated often results in an effective cap of more than 100% of the shares held by nonaffiliates.

We see at least three examples wherein Aegis or the Issuer appears to have marked the close so an issue can be much larger than would otherwise be allowed.

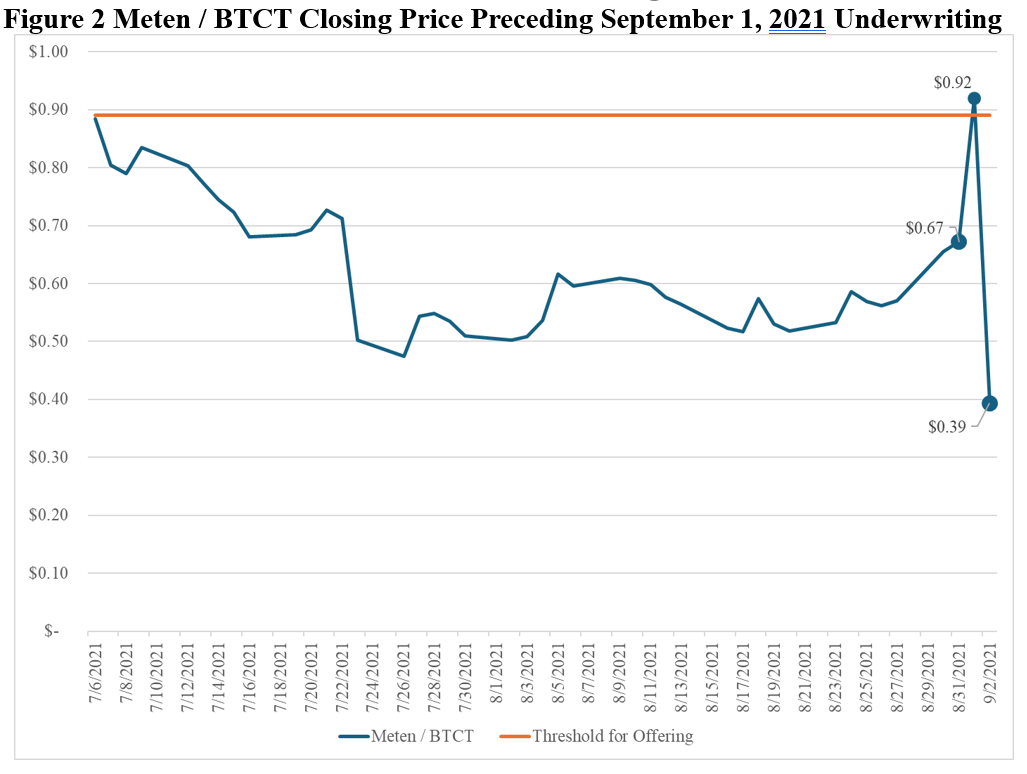

Someone Marks the Close in Meten Holding Group / BTC Digital

Meten EdtechX was created in a SPAC transaction on December 12, 2017 when EdtechX Holdings Acquisition Corp acquired Meten Education.[3] Meten was a Chinese firm providing English Language Training in

China both online and offline. In late 2022, Meten abandoned its ELT business and swapped stock for bitcoin mining machines, renaming itself BTC Digital and changing its ticker from METX to BTCT.[4]

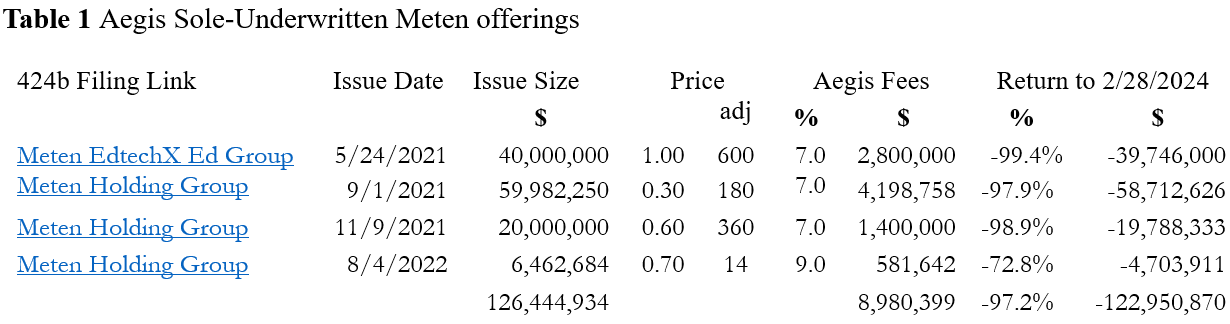

Aegis underwrote four Meten offerings listed in Table 2 and received over $9 million in fees as the sole underwriter.

Aegis justified the first Meten offering of $40 million by referencing the highwater closing price in previous 60 days which had occurred 6 weeks before the offering.

Aegis issued research analyst reports touting Meten 9which apparently was never covered by any other firm0 maintaining a $3 price target as the stock price dropped from $1 to $0.01. The first three

Aegis's research reports touting Meten were issued between the $40 million issuance on May 24, 2021 and the $60 million issuance on September 1, 2021.

Marking the Close: Aegis and Meten justified the $60 million September 1, 2021 issuance based on the $0.92 closing price on September 1 which was higher than any closing price in the

prior 60 days and higher than any closing price since. Meten's stock was manipulated to close above $0.89 on September 1 so the value of its stock held by nonaffiliates would exceed $75 million.

Without a closing price above $0.89 the $60 million September 1, 2021 issuance and subsequent two issuances totaling $26,462,684 could not proceed.

Aegis underwrote a third issuance on November 9, 2021, selling over $120,000,000 in worthless Meten stock in less than 6 months.

Aegis underwrote the fourth Meten offering on August 4, 2022 after Meten's stock price had fallen 97% in less than 15 months. Having sold $80 million in prior 12 months, this offering should not

have proceeded.

May 24, 2021 $40,000,000 Meten Issue

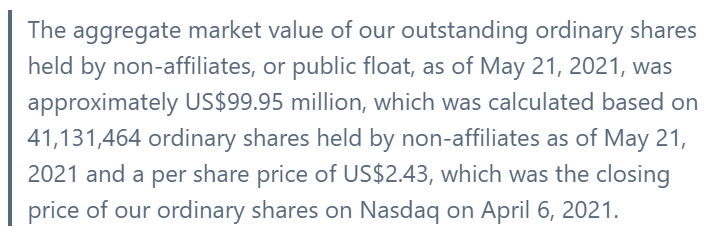

Aegis and Meten claimed that the May 24, 2021 $40 million offering was exempted from the F-3 and S-3 caps because the market value of Meten stock held by nonaffiliates exceeded $75 million based on the

price's April 6, 2021 highwater mark in the previous 60 days. Based on the most recent closing price at the time of this offering, the market value of Meten stock held by nonaffiliates was $59 million

and the $40 million offering was more than double $19.7 million, 1/3rd of the $59 million held by nonaffiliates. Aegis exercised its overallotment option and sold an additional $2 million - $42 million

total - in the May 24, 2021 issuance.[6]

On June 28, 2021 Aegis initiates analyst coverage with $3 price target and Buy Recommendation when METX was $1. Three weeks later, on July 21, 2021 Aegis reiterates buy recommendation and $3 price target

when METX was $0.73. Three weeks further on, on August 18, 2021 Aegis reiterates buy recommendation and $3 price target when METX was $0.57.

September 1, 2021 $59,982,250 Meten Issue - Marking the Close

September 1, 2021 Aegis / Meten issuance read, in part,

Aegis and Meten claimed that the September 1, 2021 $60 million offering was exempted from the F-3 and S-3 caps because the market value of Meten stock held by nonaffiliates slightly exceeded $75 million

based on the $0.92 closing price September 1, 2021.

The September 1, 2021 Aegis / Meten offering was an outright fraud facilitated by a classic "marking the close" market manipulation. Meten had sold $40 million in May through Aegis and so was not

eligible to issue any new stock unless the value of Meten stock held by nonaffiliates exceeded $75 million. Meten's stock price had to exceed $0.89 for the value held by nonaffiliates to exceed $75 million,

given the 84,501,953 shares Meten claimed were held by nonaffiliates.[8]

July 2, 2021 - outside the trailing 60-day window - was the last day prior to September 1, 2021 when Meten closed above $0.89. By September 1, 2021 plans to issue $40 million of stock would have to be

cancelled unless the stock closed above $0.89 on September 1, 2021 or thereafter.[9]

With no material news, the trading volume on September 1, 2021 was 28 times the average daily trading volume over the prior two months and Meten closed at $0.92 - up 37% from the prior day's $0.67 close.

The extraordinarily heavy trading volume occurred throughout the day and steadily pushed Meten's price higher. The price exceeded $0.89 first around 2:30 in the afternoon and plateaued on heavy

volume until the close at $0.9194 - and then opened the next morning with the very next trade at $0.4543.[10]

Aegis, Meten, both or someone else marked the close on September 1, 2021 to allow this $60 million offering to proceed. If the stock had not closed above $0.89, no offering in any amount could have

taken place.

Based on the February 28, 2024 $0.00635 closing price, investors in this single Aegis underwritten offering needlessly lost at least $58,712,626.

November 9, 2021 $20,000,000 Meten Issue

On November 9, 2021 Aegis underwrote a new $20 million Meten issue. With this issue, Aegis had underwritten $120 million of worthless Meten stock in less than 6 months.

Aegis Capital Issues Two more Research Reports Reiterating Buy and $3 Price Target

On November 23, 2021, Aegis reiterates buy and $3 price target when METX was $0.36. On May 16, 2022, Aegis reiterates buy and $3 price target when METX was $0.04.

August 4, 2022 $20,000,000 Meten Issue

Meten's stock price continued its free fall after the November 9, 2021 issue. It underwent a 1:30 reverse split on May 5, 2022. On August 4, 2022, Meten closed at $0.95 post-split,

$0.03 pre-split. Aegis and Meten reached back to the $1.79 post-split highwater mark price on June 6, 2022 to justify the claimed $19.41 million value of shares held by nonaffiliates.

Meten and Aegis claimed capacity to issue $6.47 million and in fact issued and sold $6.46 million in new shares despite having already sold $80 million in the prior 12 months.

Aegis Capital Issues Another Research Report Reiterating Buy and $3 Price Target

On December 5, 2022, Aegis reiterates buy and $3 price target when METX was $0.01.

Meden had two reverse stock splits.

On May 5, 2022 it split 1:30; on August 24, 2023 it split 1:20.

BTCT's closing price on February 28, 2024 was $0.00635 on a split adjusted basis compared to the $1.00, $0.30 and $0.60 underwritten prices in 2021.

Conclusion

Aegis Capital underwrote 4 fraudulent Meten stock issuances totaling $126 million in 2021 and 2022.

Aegis published research analyst reports in support of these offerings with strong buy recommendations and unrealistic price targets.

Aegis and Meten gamed the calculation of the market value of Meten shares held by nonaffiliates.

Aegis, Meten or others marked the close on September 1, 2021 to allow the September 1, 2021 and subsequent issuances to proceed when the issuance would otherwise have been impossible.

Investors lost at least $126 million because of the fraudulent stock offerings underwritten by Aegis.

Discussion

The dramatic failure of Aegis's offerings, both in absolute terms and relative to the micro-cap stock market, demonstrates that Aegis specialized in underwriting hopelessly failing firms

desperate for capital.

As sole underwriter of the offerings, Aegis Capital had a duty to conduct reasonable due diligence into the issuers' operations, business model, financial statements, forecasts, representations.[12]

If Aegis had been doing adequate due diligence to issues it underwrote would have had average returns approximately equal to the average returns to micro-cap stocks, with roughly an equal number

of Aegis underwritten issuers doing better than the micro-cap market as doing worse than the micro-cap market. Instead over 95% of Aegis's underwritings underperformed the average microcap stock.

As with its earlier offerings, offerings underwritten by Aegis in 2020-2023 continued to fail at dramatic rates. Investors, whether retail brokerage clients of Aegis or not, lost approximately

$1.5 billion directly from the decline in value of worthless stock Aegis underwrote.

As a broker-dealer, Aegis has duties to its retail customers. The extent of those duties may depend on the contractual or de facto relationship between the firm and the client. Aegis appears to

have systematically violated the duties it owed to its retail clients. At a minimum, Aegis as broker-dealer needed to understand the issuers' business and have a reasonable basis for recommending

its underwritings to its retail clients.[13] No unconflicted broker dealer would have allowed its brokers to recommend the worthless stock Aegis was systematically underwriting.

In addition to selling concessions Aegis brokers shared in. Aegis brokers likely received commission credit for hundreds of millions of dollars in markups and markdowns as these worthless stocks

were turned over in retail accounts.

As a market maker in these securities, Aegis had a responsibility to "have a reasonable basis for believing the prospectus and other information made available by the issuer of the securities was accurate."[14]

Based on our review of trading volume and closing bid-ask spread from Bloomberg, investors have paid $1.4 billion in bid-ask spread to market makers including Aegis as a result of trading these worthless

Aegis underwritten stocks in just the past 5 years.

Based on observed daily trading volumes and end of day bid ask spreads in the stocks Aegis underwrote, investors paid approximately $1.5 billion in bid ask spread to market makers including Aegis.

As publisher of research analyst reports, Aegis was required to ensure that its analysts were free of conflicts of interest and presented unbiased recommendations and price targets.

Aegis was also required to objectively assess the correspondence between its analyst's published opinions and subsequent returns earned by investors in the covered companies.[15] Given the shocking,

widespread and continuous failure of the stocks Aegis underwrote and on which it provided glowing research coverage, Aegis did not effectively meet its research analyst obligations.

Summary

In the past 10 years, Aegis has underwritten nearly $2 billion of worthless securities - over $1 billion in just the past 3 years. Aegis made a market in these newly issued worthless securities

and bought them into its unsophisticated retail customers' accounts. Investors have lost 98% of the initial investment as the large cap and microcap stock markets experienced positive returns.

Investors also lost over $1.5 billion in unnecessary markups, markdowns and bid-ask spread trading these worthless Aegis-underwritten securities.

In this note we provide summary statistics and returns analysis as well as details on 186 Aegis sole underwritings. We illustrate our analysis with Meten / BTC Digital not because it is unusual but

because it is typical of Aegis' conduct. Every one of the 111 issuers has a story to tell about Aegis as an underwriter, broker, market maker and/or research analyst.

We will follow this note with additional case studies into Aegis underwritings but the clear take away is that not only should investors avoid Aegis Capital as a retail brokerage firm because of its

high rate of customer complaints, investors should avoid buying or holding any stock solely underwritten by Aegis Capital.

Appendix

Aegis Sole Underwritten Offerings, Subtotaled by Issuer, Hyperlinked to 424(b)s

###

[1] Some of the offerings were of units combining a share of stock and a warrant on a share of stock. The included warrants had strike prices typically equal to or greater than the issue date unit prices. After the issue dates these warrants traded separately from the common stock and for a time traded at significant prices. In the statistics below, we ignore the value of the warrants because the stock prices fell so much that the warrants from these offerings are currently worthless for the vast majority of the offerings. Including the value of warrants in the rare instance where the issued warrants have any value will not have a material impact on our conclusion that Aegis's underwritten offerings lost almost all their value when the stock market generally had significant positive returns.

[2] In fact, the instructions do not reference the closing price over the prior 60 days. The instructions require issuers to use the most recent sale price or the average bid and ask price on some date in the prior 60 days. The instructions seem quite clear and allow for only the volume weighted average bid and ask prices as trades occur throughout the day, the simple average inside bid and ask quotes throughout the day. All the Aegis underwritings we reviewed wherein a price for a date prior to the most recent closing price appear to incorrectly use the closing price.

[8] We have not been able to verify Meten's claimed number of shares held by nonaffiliates but given all the other observed indications of fraud in Aegis's underwriting of Meten's issuance the claimed number of shares held by nonaffiliates warrants further investigation.

[9] For 40 calendar days prior to July 1, 2021 Meten had closed each day between $0.90 and $1.00 just above the threshold required for Meten to issue any new shares given the $40 million it had already sold in the prior 12 months.

[10] Meten issued a press release before the open on September 1, 2021 touting plans to use crypto currencies in some fashion but this press release was so inconsequential that Meten did not file a Form 6-K and its existence seems to have been entirely ignored to this date.

[13] "Study on Investment Advisers and Broker-Dealers" January 2011 www.sec.gov/news/studies/2011/913studyfinal.pdf at page 63:

In general, three approaches to suitability have developed under the case law, including FINRA and Commission enforcement actions - "reasonable basis" suitability, "customer-specific" suitability, and "quantitative" suitability. Under reasonable basis suitability, a broker-dealer has an affirmative duty to have an "adequate and reasonable basis" for any security or strategy recommendation that it makes.284 A broker-dealer, therefore, has the obligation to investigate and have adequate information about the security or strategy it is recommending.