Feb 2014

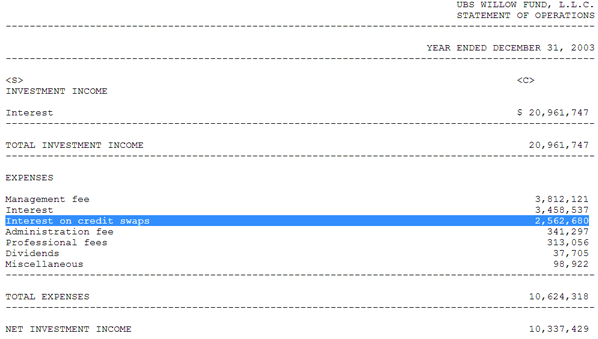

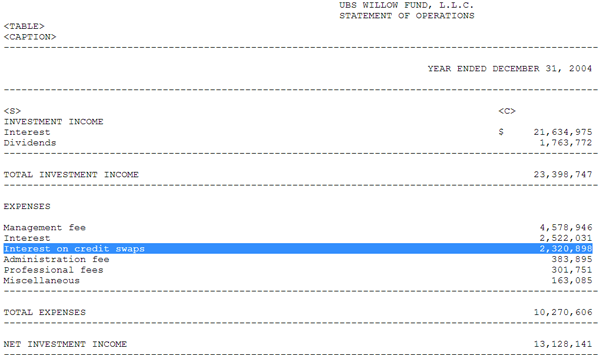

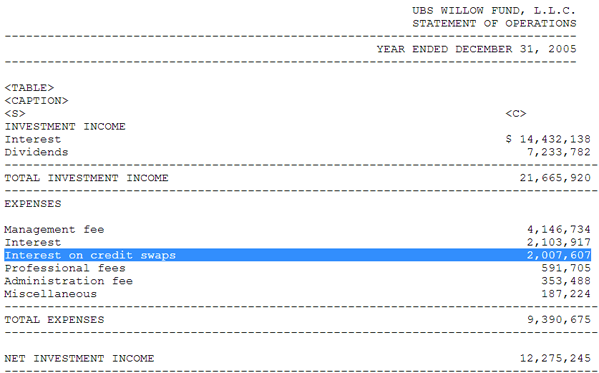

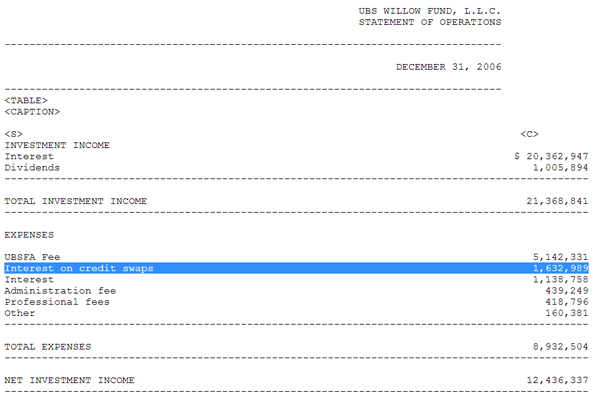

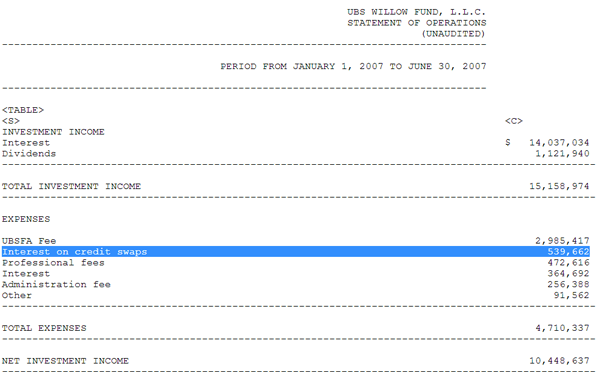

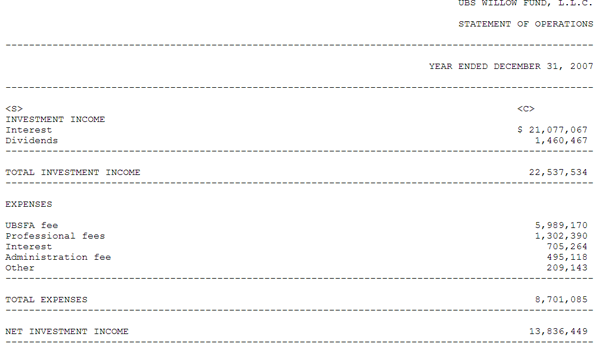

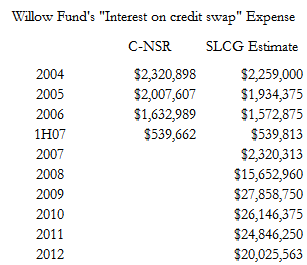

The accrued expense related to the periodic payments is reflected as interest on credit swaps in the Statement of Operations.Starting with the December 31, 2007 N-CRS, this language was changed to read:

The accrued expense related to the periodic payments on credit default swaps is reflected as realized and unrealized loss in the Statement of Operations.This CDS expense skyrocketed after the Willow Fund stopped reporting it. We estimate that the Fund paid over $20 million per year on average in CDS premiums from 2008 to 2012. By changing how it reported this item from an expense to a change in the market value of the securities it held or had sold the Willow fund was able to mislead investors.