Jan 2014

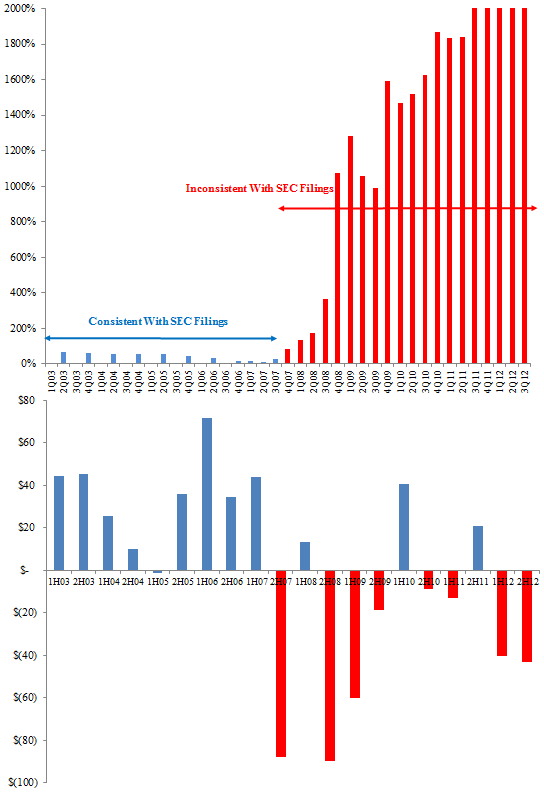

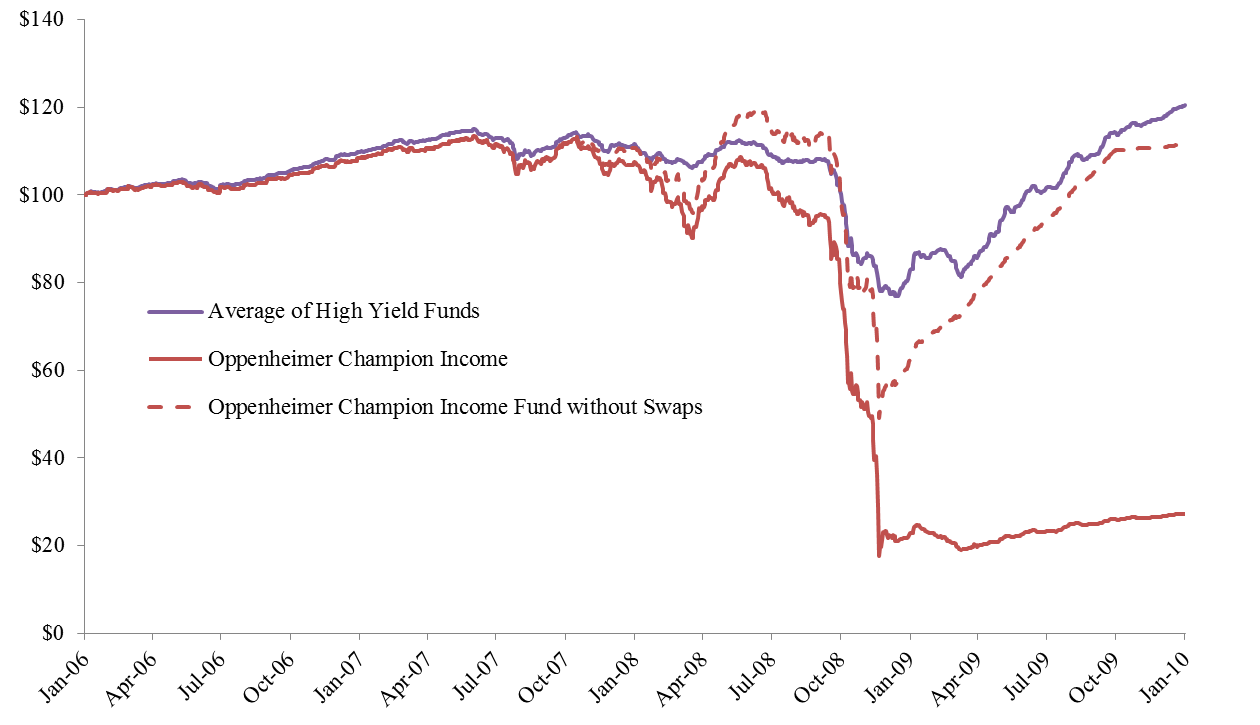

UBS Willow Fund, L.L.C. (the "Fund") was organized as a limited liability company under the laws of Delaware on February 1, 2000. The Fund is registered under the Investment Company Act of 1940, as amended (the "1940 Act") as a closed-end, non-diversified management investment company. The Fund's investment objective is to maximize total return. The Fund pursues its investment objective by investing primarily in debt securities and other obligations and to a lesser extent equity securities of U.S. companies that are experiencing significant financial or business difficulties (collectively, "Distressed Obligations"). The Fund also may invest in Distressed Obligations of foreign issuers and other privately held obligations. The Fund may use a variety of special investment techniques to hedge a portion of its investment portfolio against various risks or other factors that generally affect the values of securities and for non-hedging purposes to pursue the Fund's investment objective. These techniques may involve the use of derivative transactions, including credit swaps. The Fund commenced operations on May 8, 2000.The fund's annual and semi-annual reports can be downloaded off the SEC website. While the fund managers claimed to be investing in distressed debt, in late 2007 and early 2008 they were aggressively shorting high yield debt. The Fund increased its short position in 2008 and 2009 betting that credit spreads would widen further.