Jan 2014

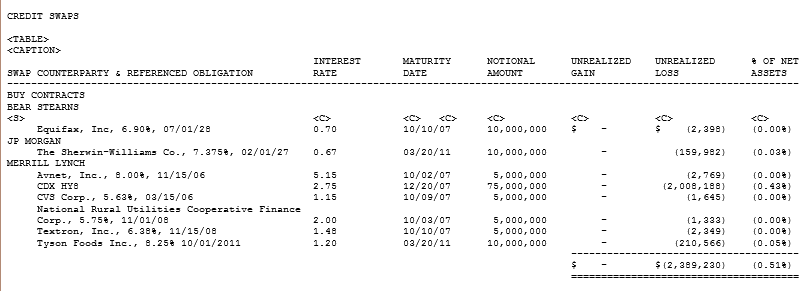

... The Fund may use a variety of special investment techniques to hedge a portion of its investment portfolio against various risks or other factors that generally affect the values of securities and for non-hedging purposes to pursue the Fund's investment objective. These techniques may involve the use of derivative transactions, including credit default swaps.*A Credit Default Swap ("CDS") is a contract that transfers the risk of a credit default on a given bond or portfolio of bonds. The company that issues the bond is called a reference entity. A CDS contract involves two parties, a party that wishes to buy insurance and a party that wishes to sell insurance. The buyer of insurance agrees to pay fixed periodic payments to the seller of insurance. The fixed payments are called CDS premiums. In exchange for the CDS premiums, if the bond issued by the reference entity defaults, the seller of insurance must purchase it from the buyer of insurance at face value or make a cash settlement payment equal to the difference between the defaulted bond's face value and its market value.