Another Example of Non-Traded REITs' Wealth Destruction: Columbia Property Trust (Wells REIT II) Cost Investors $4.4 Billion

Jan 2014

Non-traded REITs are illiquid investments, not listed on public exchanges and with little to no secondary market trading. Their offering documents typically claim that after some period of time, perhaps 5-10 years, the REIT intends to list on an exchange, merge with another company, or in some other way allow investors to sell their shares but for many non-traded REITs, this "liquidity event" never occurs.

However, even if a non-traded REIT lists on a major exchange, that does not mean that its original investors have benefited from being sold such an illiquid investment. Investors in many subsequently listed non-traded REITs have sustained massive losses relative to low cost, liquid alternatives they should have been sold in the first place.

For example, Columbia Property Trust (CXP, formerly known as Wells Real Estate Investment Trust II) was first sold as a non-traded REIT in 2004 and subsequently listed on the New York Stock Exchange in October 2013. Before it was listed, it sold shares to new investors at $10 per share. After its first day trading on the NYSE, its per share value was $22.52.

Looks like a win for CXP's investors but that was accomplished entirely by sleight of hand. Columbia Property Trust underwent a 4-for-1 reverse share split. Therefore the post-listing value of a $10 CXP share was approximately $5.63 or equivalently investors originally paid $40 for what was selling after the listing for $22.52 -- a capital loss of almost 44%. Many non-traded REITs do a reverse stock split before listing to give the appearance of capital appreciation.

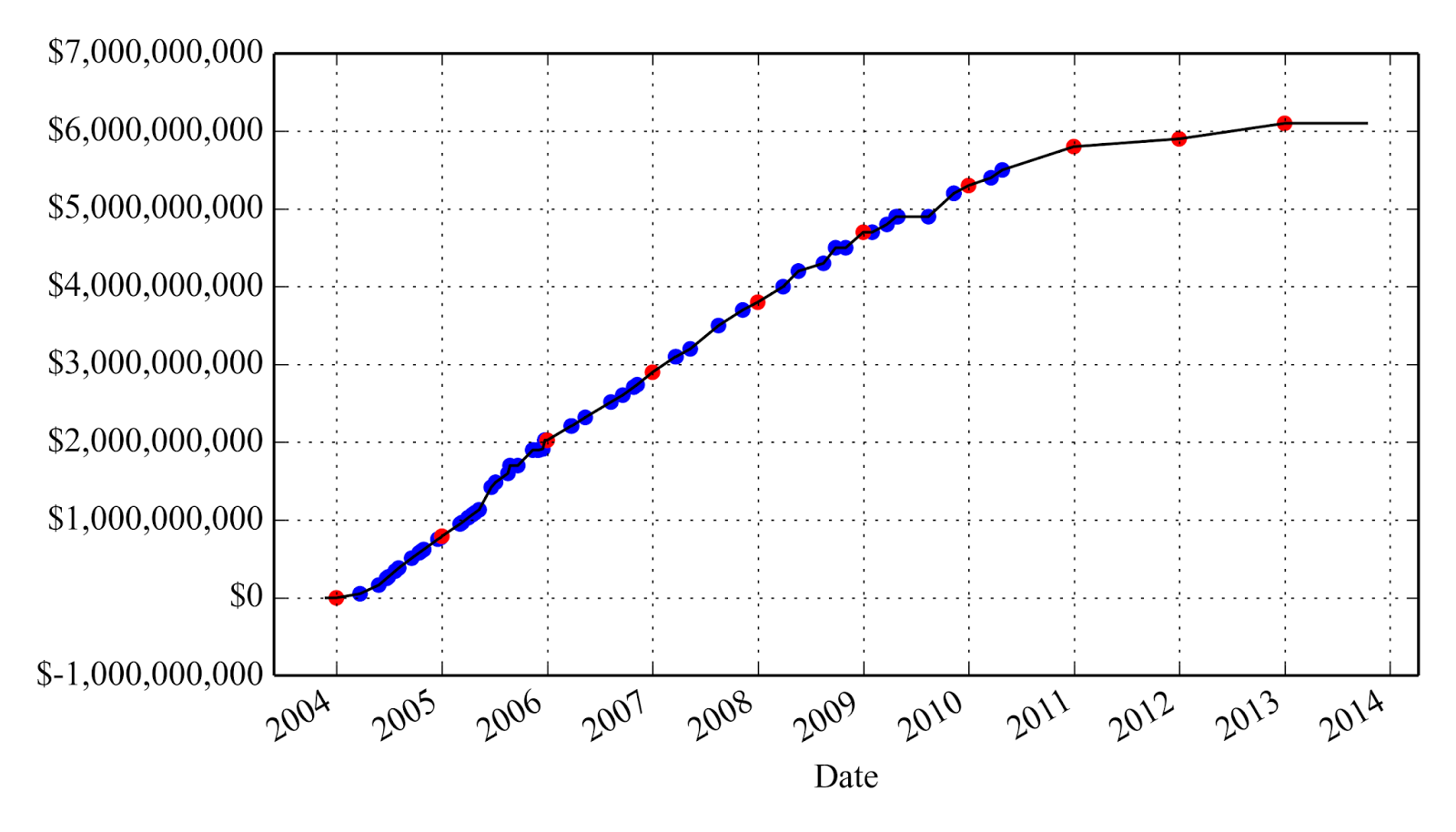

The CXP losses are even greater if you consider what that $10 would have purchased in a low cost, diversified real estate fund such as Vanguard's REIT Index Fund. We can do this using the same methodology we applied to Behringer Harvard REIT I / TIER REIT last week. Columbia Property Trust (or Wells Real Estate Investment Trust II) raised approximately $6.1 billion from 2004 to 2013, as reflected in its 10-K and 424B3 filings:

Columbia Property Trust / Wells REIT II Gross Proceeds (blue dots are from 424B3s, red dots are from 10-Ks)

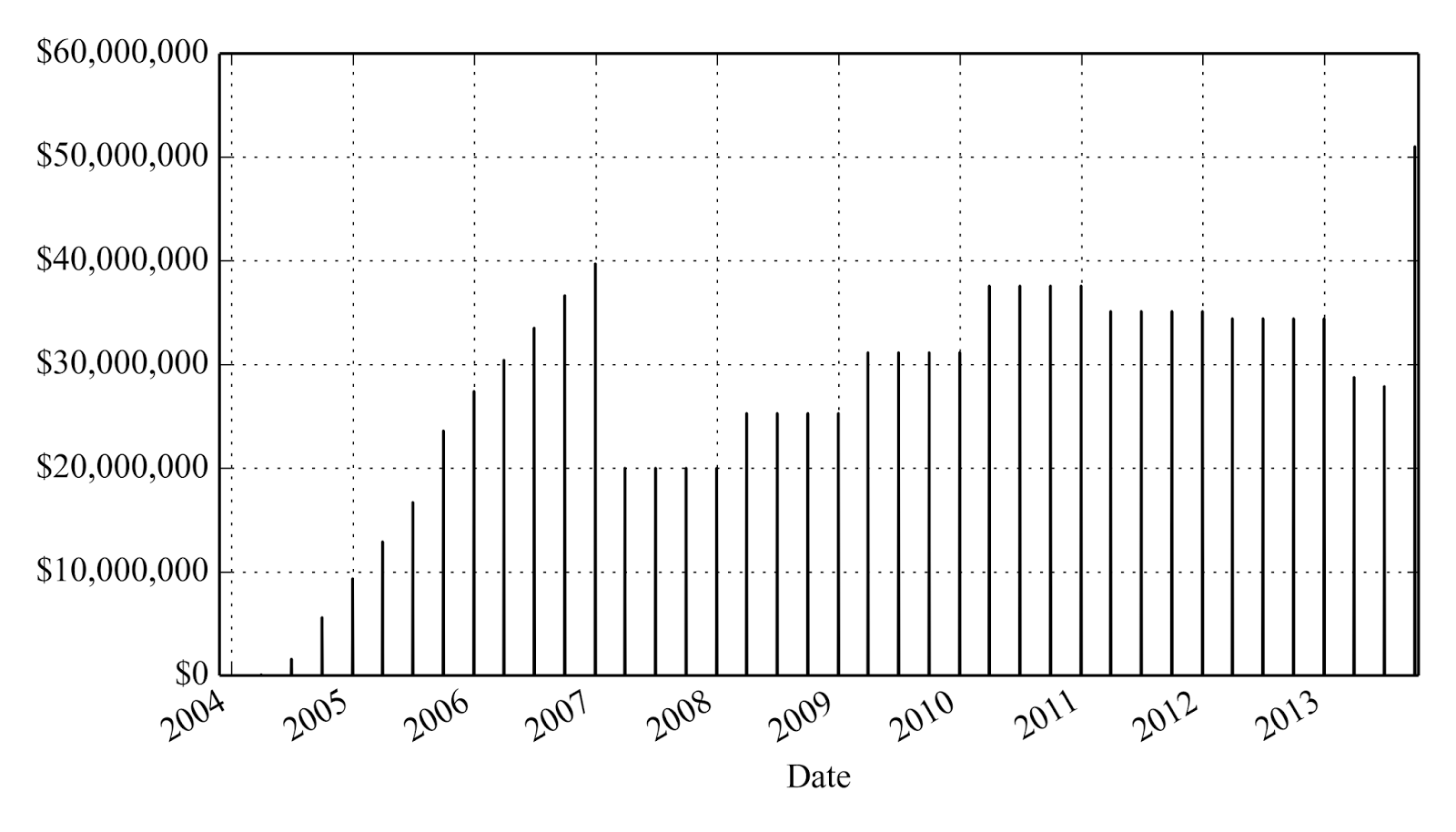

It also paid approximately $1.1 billion in quarterly distributions:

Columbia Property Trust / Wells REIT II Distributions

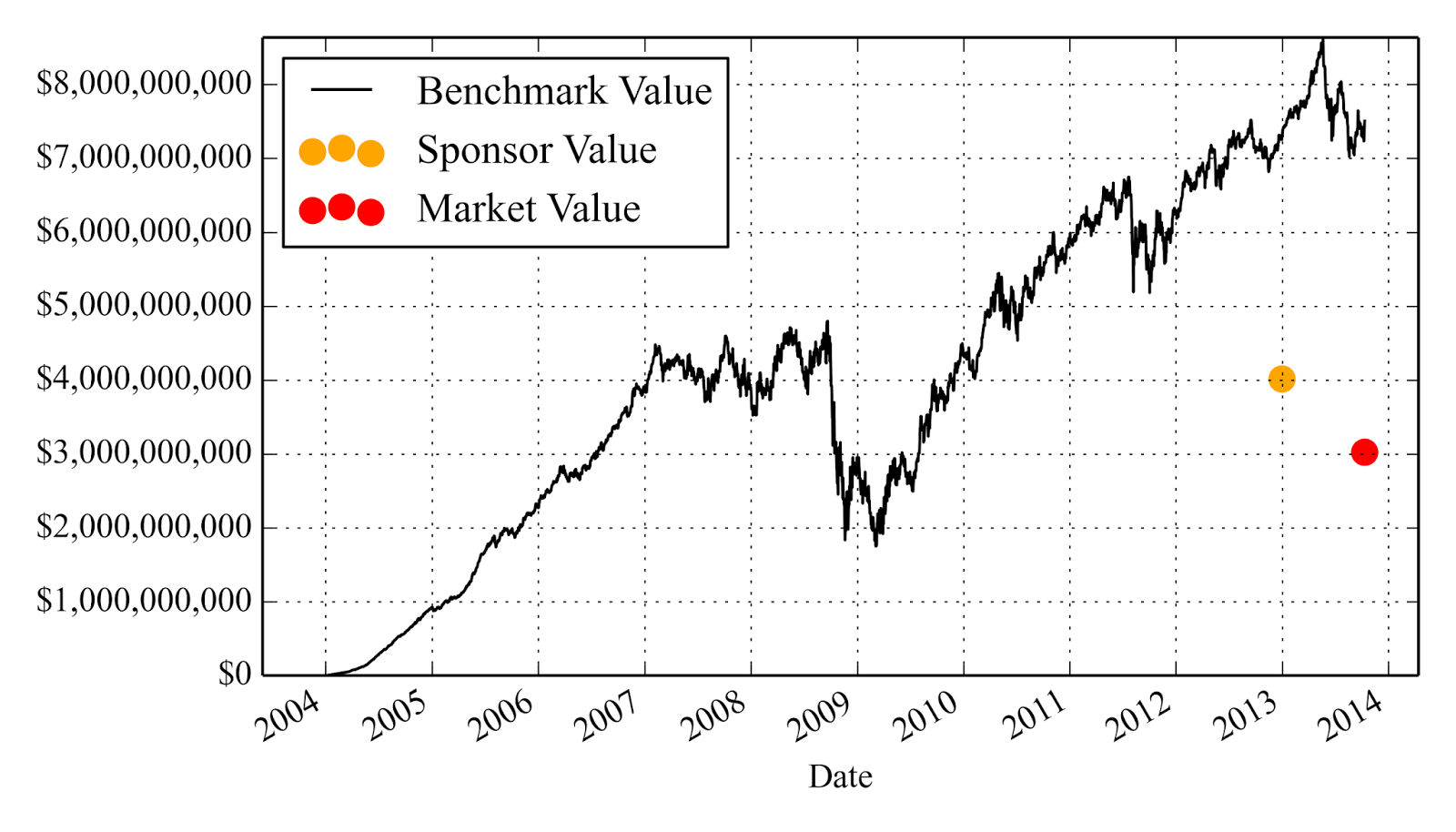

Columbia Property Trust's value after its first day of trading was $22.52. Based on the 134,192,610 post-split shares outstanding, the aggregate value of the CXP REIT was approximately $3.0 billion. If we apply the proceeds raised by Columbia Property Trust from its offering of common shares to the Vanguard REIT Index Fund, the resulting October 2013 value is approximately $7.4 billion.

Investors' Net Investments in Wells REIT II Applied to Vanguard's Traded REIT Fund

By choosing Wells REIT II / Columbia Property Trust over a liquid alternative, investors lost $4.4 billion. In addition, Columbia Property Trust's liquid market value was over $1 billion less than the sponsor's estimated value.

A casual observer might think that Columbia Property Trust was a success story: a successful listing at over twice its offering price. But the reality is that investors lost big as a result of being sold a high cost, illiquid non-traded REIT. If they had chosen a low cost, diversified, completely liquid real estate mutual fund, they would have had about $4.4 billion more than they ended up with.