Behringer Harvard / TIER REIT Illustrates How Non-Traded REIT Sponsors and Brokers Have Siphoned $10 Billion to $20 Billion (and Counting) From Investors

Jan 2014

Sponsors have issued, and brokers had sold, over $85 billion of non-traded real estate investment trusts (REITs) by the end of 2012. These investments are illiquid, high-commissioned, poorly diversified real estate investments. Despite their glaring defects another $20 billion of non-traded REITs were sold to investors in 2013.

Sponsors and brokers have siphoned off at least $20 billion from investors through their sales of non-traded REITs up through 2012. We illustrate the calculation of these sponsor and broker transfers from investors using investors experience in the Behringer Harvard REIT I.

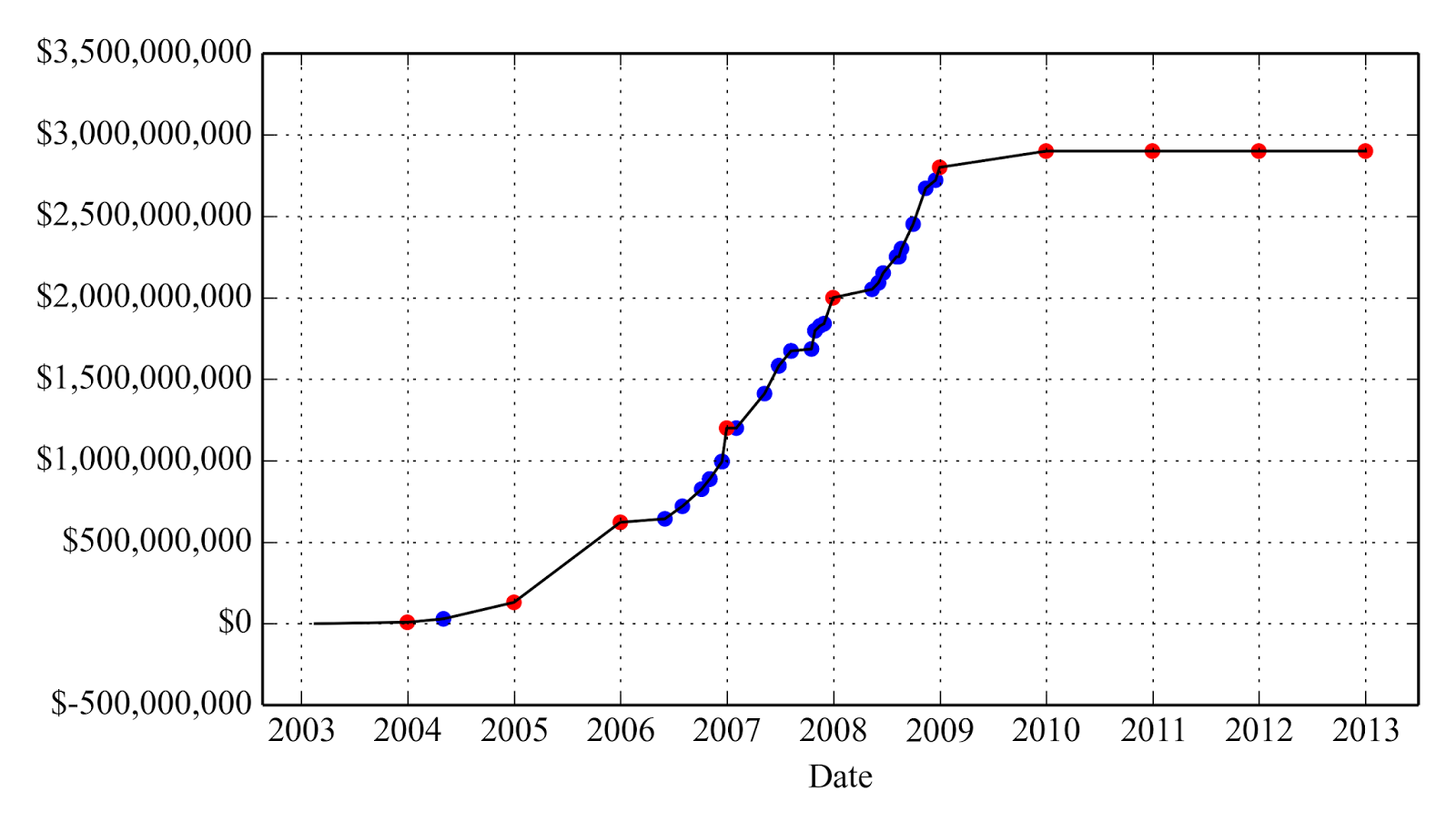

With the help of highly compensated brokers, Behringer Harvard sold $2.9 billion of its BH REIT I shares to investors between 2003 and 2010.* Figure 1 plots the gross proceeds raised by BH REIT I, now known as TIER REIT, from its first effective date through its most recent 10-K:

Figure 1. Behringer Harvard REIT I Gross Proceeds (blue dots are from 424B3s, red dots are from 10-Ks)

BH REIT 1 also paid monthly distributions (reported quarterly) plotted in Figure 2.

Figure 2. Behringer Harvard REIT I Distributions

BH REIT 1's most recent reported value was $4.01, although secondary market trades have been below $2.50. Thus investors in this non-traded REIT suffered principal losses of $1.4 billion ($1.1 billion after offsetting with $300 million in distributions). These losses are not the result of general losses in the underlying commercial real estate market. The value of US commercial real estate as a whole has been increasing rapidly since a low point in early 2009 and now exceeds its prior peak.

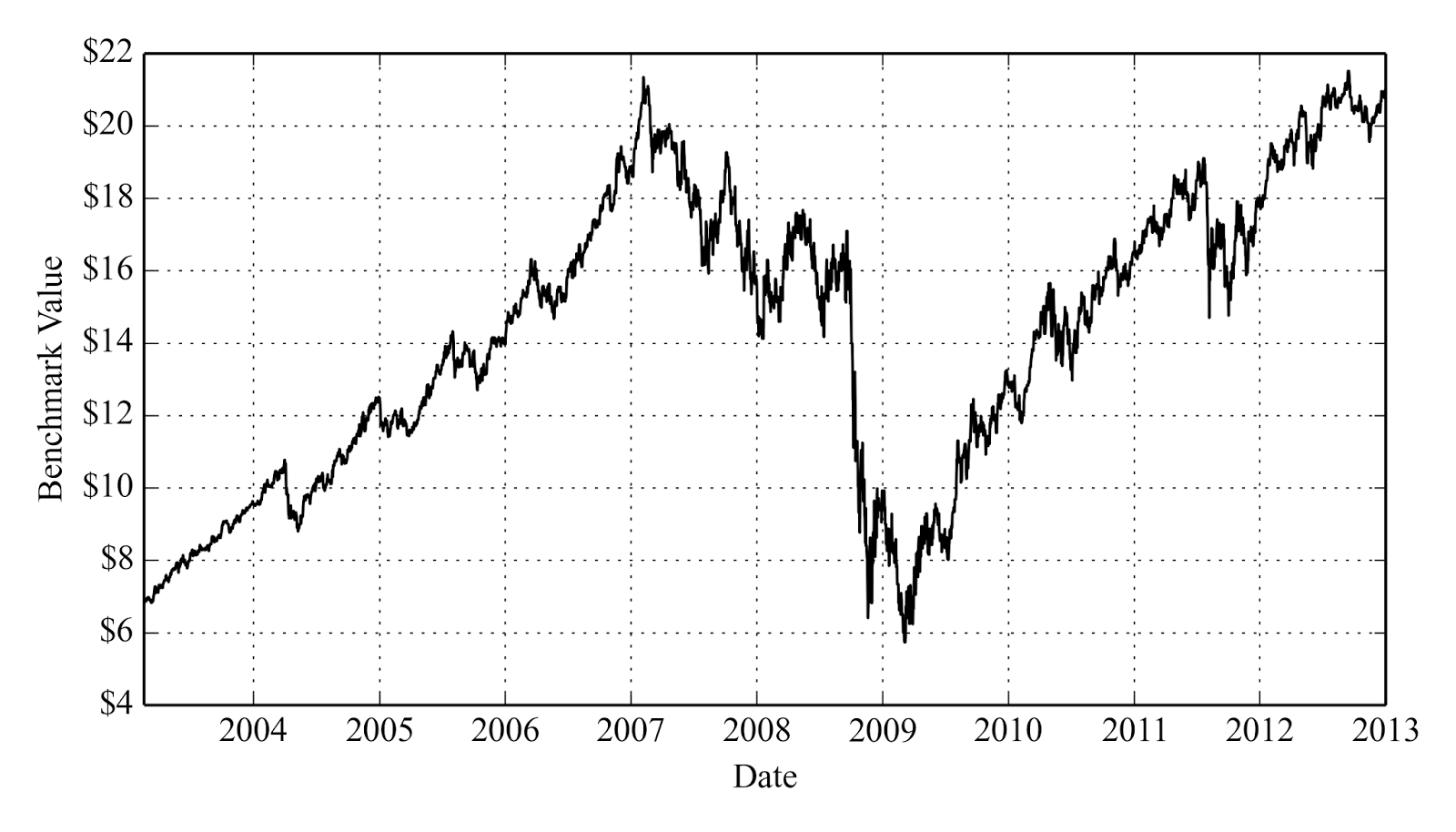

Figure 3. Split and Dividend Adjusted Vanguard REIT Index Fund [VGSIX]

What if all that investor money that brokers directed into the BH REIT 1 had been invested in a portfolio of traded REITs like the Vanguard fund instead? The value of that investment over time is shown below:

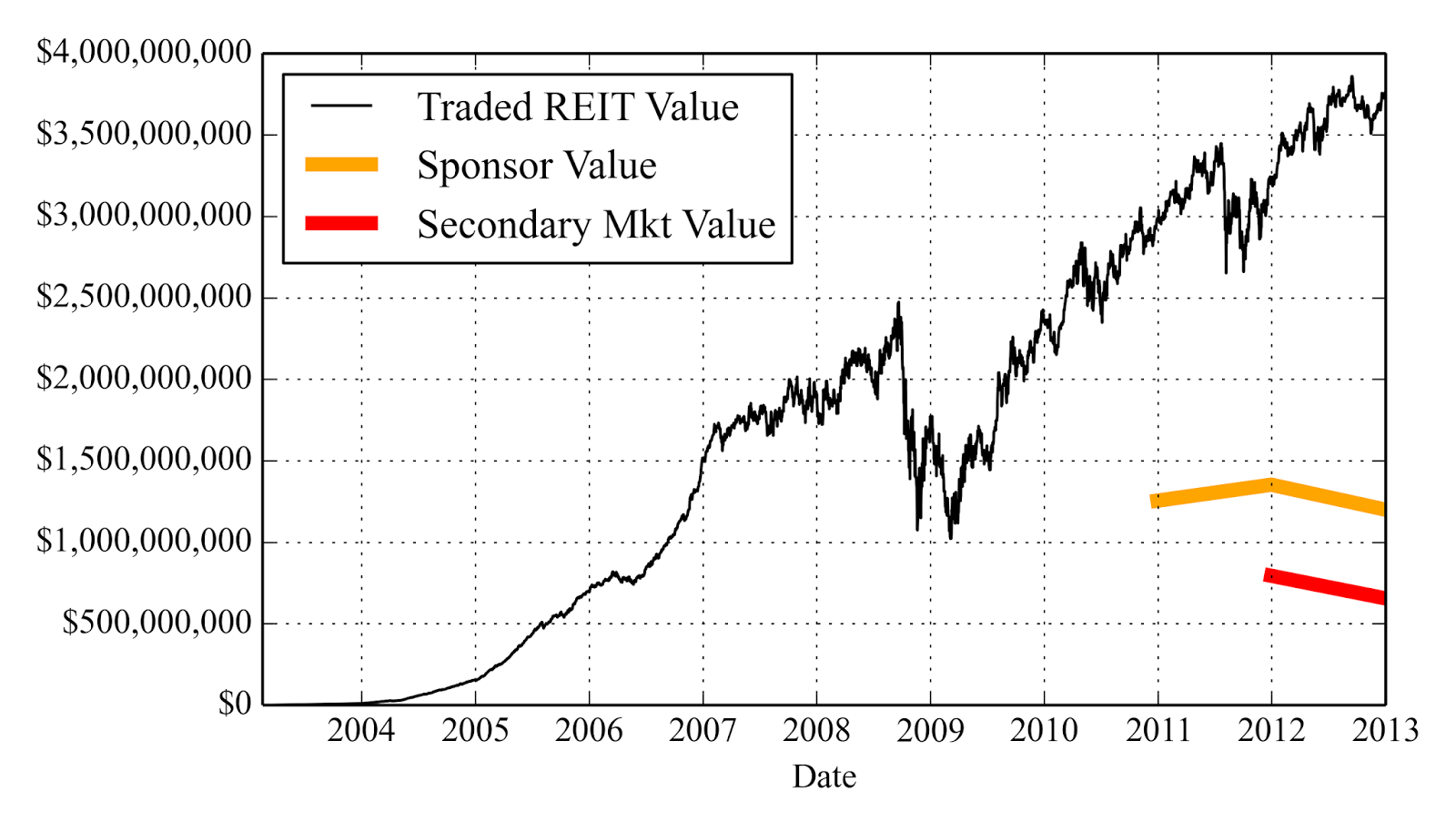

Figure 4. Investors' Net Investments in BH REIT 1 Applied to Vanguard's Traded REIT Fund

Had the funds put into BH REIT I been instead invested in the Vanguard REIT Index Fund, they would be worth approximately $3.8 billion. If we apply Behringer Harvard's last reported value of $4.01 BH REIT I's current value is only $1.2 billion -- a shortfall of $2.6 billion. This relative loss of value reflects a combination of high fees and poor returns relative to real estate as a whole.

However, the last reported value of a non-traded REIT is merely the sponsor's claimed estimate. This REIT has traded in the limited secondary market for approximately $2.19 per share. Therefore the current value could as low as $0.7 billion, for a shortfall of $3.1 billion.

The losses investors suffered in BH REIT 1 relative to liquid, diversified real estate investments were in part due to the high commissions brokers receive for selling these products and large fees taken by non-traded REIT sponsors. Investors paid about $300 million in unnecessary upfront fees in BH REIT 1. Had those fees been invested in traded REITs they would be worth over $500 million today. We estimate that as much as $20 billion in current real estate investment values have been transferred from retail investors to sponsors, brokerage firms and brokers through the sale of non-traded REITs.

No investors should buy these illiquid, high-commissioned, poorly diversified non-traded REITs and no un-conflicted broker would recommend them.

_______________________________________

* We estimate this from BH REIT I's 424B3 and 10-Ks filings with the SEC.