Yesterday, FINRA fined Morgan Stanley for best execution and for charging excessive markups or markdowns. We have been covering markups extensively, and we have taken the Morgan Stanley municipal bond transactions identified by the FINRA action and applied our markup calculation methodology to calculate the distribution of markups charged by Morgan Stanley.

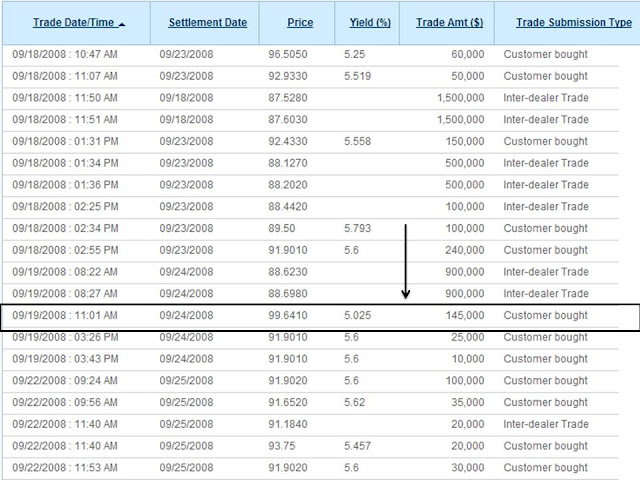

Let's start with an example. FINRA flagged a customer purchase of $145,000 in a West Virginia municipal bond (CUSIP: 95639RBW8) on September 19, 2008 at 11:01 AM. Morgan Stanley sold this bond to the customer at a price of $99.64. Looking at the EMMA trade data for this bond, we can identify this transaction exactly.

We can also see that at 8:27 AM that same day, there was a much larger inter-dealer trade for only $88.70! That's a markup of over 12% or more than 8 times the median markup of similar sized bond trades.

The average interdealer price on September 19, 2008 was $88.60 and the average interdealer price on September 18 and 19, 2008 was $88.06. There were 5 other, smaller, customer purchases of this bond on September 18 and September 19 with a weighted average price of $92.25. Morgan Stanley charged this customer $7.41 more per bond than other customers making smaller purchases in the same bond at the same time were being charged.

This matches a very similar pattern to other municipal bond markups we have identified before.

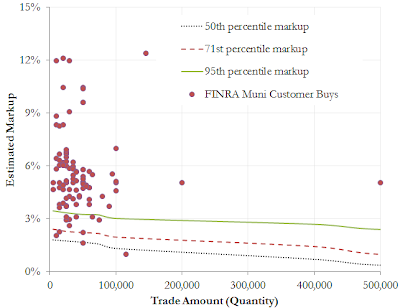

We compared the distribution of estimated markups from a sample of over 13.5 million customer trades in fixed-coupon, long-term municipal bonds to those mentioned in the Morgan Stanley AWC.

The following figure shows the 50th percentile markup, 71st percentile markup and 95th percentile markup for the distribution of fixed-rate, long-term customer trades from our large sample. Also included in this figure are the individual Morgan Stanley customer purchases mentioned by FINRA that had a corresponding match in the EMMA data. The majority of the AWC purchases are for less than 100,000.

Many of the markups charged by Morgan Stanley and identified by FINRA were less than 5% of the bond's market price. The so-called '5% Policy' -- that markups charged above 5% of prevailing market prices constitute excessive -- has been challenged by many, and in 2011 FINRA proposed scrapping the term altogether . Yesterday's action against Morgan Stanley suggests that even markups under 5% can be excessive and subject to restitution.

47 of the 165 municipal bond transactions could not be found in EMMA trade data. This is an issue we have discussed before in the context of municipal bond ETFs, whose transactions also do not always appear to be reflected in EMMA, or sometimes appear in the wrong direction (purchases as sales and vice versa). It may be that the data reported to EMMA is either incomplete, inconsistent (with some reported prices including markups while others do not), or contains erroneous entries.

Our colleagues' research suggests that excessive markets are endemic to the municipal bond market, and that retail investors have been charged over $10 billion in markups by brokers over just the last eight years. This FINRA action may only be the first of many actions against brokers for this potentially very common issue.