Our study looks at markups and markdowns implied by EMMA trade data. My colleagues have shown an example of how we calculate the markups, but I wanted to illustrate the methodology used to handle the more complex cases that arose when analyzing the trade data.

There were effectively four cases that we needed to address. The first case occurs when inter-dealer trades occur on the same business day as the customer trade. In that case we computed the volume weighted average price (VWAP) of the inter-dealer trades and calculated the absolute markup or markdown as the difference between the customer price and the VWAP. This case was covered in the previous example.

In this case, the VWAP of the customer orders is $104.3967. As a result, we estimate the absolute markup charged on the customer purchase is $1.4573 and the absolute markdown charged on the customer sale is $0.7287. We also report a percentilemarkup, which is the absolute markup divided by the VWAP -- in this case, the percentile markup is 1.3959% and the percentile markdown is 0.6980%. To get the dollar amount of the markup, multiply by the trade amt divided by 100. The customer who purchased the bonds was charged an markup of $146 and the customer who sold the bonds was charged a markdown of $146.

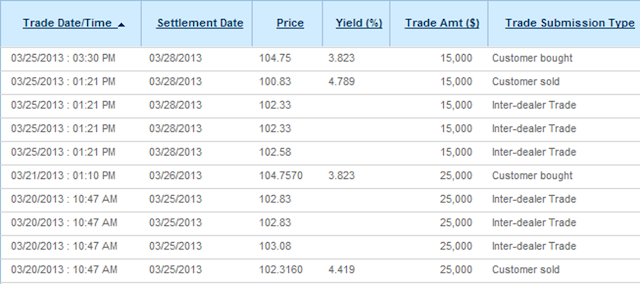

The VWAP of inter-dealer trades was $102.7258. The customer purchase on March 21, 2013 transacted at $104.7570, implying an absolute markup of $2.0312. The dollar amount of this markup is $336.

In this case, the VWAP of the customer orders is $107.398. The absolute markup charged on the customer purchase is $1.513 and the absolute markdown charged on the customer sale is $1.513 (equal because the trades are of equal size). The dollar value of the markup was $151 and of the markdown is $151.

Those four cases covered approximately 93% of the customer trades. If none of these cases are met, then we did not assign a markup or markdown to the customer trade.