SLCG Research: Volatility Smiles from Leveraged ETF Options

Jan 2013

Leveraged ETFs are a perennial subject on our blog. I thought I'd take this opportunity to highlight a recent research project entitled "Crooked Volatility Smiles: Evidence from Leveraged and Inverse ETF Options" that I recently completed with my colleagues Geng Deng, Craig McCann and Mike Yan.

While studying options data on leveraged and inverse ETFs, we began to notice a pattern such that deep-in-the-money call options -- contacts whose strike price is well above the current spot price -- on inverse leveraged ETFs were more expensive than similar deep-in-the-money call options on positively leveraged ETFs. A the same time, we noticed that far-from-the-money call options -- current spot price is below the option's strike price -- on inverse ETFs were cheaper than similar far-from-the-money options on positively leveraged ETFs.

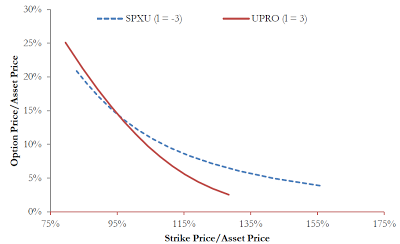

As an example, the following figure shows the market prices of three-month call options on ProShares UltraPro Short S&P 500 ETF (SPXU) and ProShares UltraPro S&P 500 ETF (UPRO) on October 19, 2009.

UPRO is a daily (3x) leveraged ETF and SPXU is a daily (-3x) inverse leveraged ETF. If we were to believe the classic model -- Black-Scholes model for those in finance -- for option pricing, these two lines should be on top of one another since both ETFs track the S&P 500.

My colleagues and I looked beyond the classic model and found that a popular stochastic volatility model can explain this phenomenon neatly. We showed further that this stochastic model can properly predict the price at which options on pairs of ETFs have the same value -- graphically this is the intersection point in the figure above. See the SSRN entry for the paper.