Leveraged Exchange Traded Funds (ETFs) are some of the most popular exchange-traded vehicles and (as a result) are liquid, widely available, and very likely to be on the radar screen of even casual investors.

In a previous blog post, we introduced the basics of ETFs. In this post, we are going to discuss a specific kind of ETF: Leveraged ETFs. This post is part of a two-part series. The next post will concern a related instrument called Inverse Leveraged ETFs.

A Leveraged ETF offers investors a daily return that is a multiple of the daily return of the index or asset tracked by the ETF. For example, a 2x leveraged ETF that tracks the S&P 500 index (SPX) would return 2x the daily return of the SPX. So if SPX exhibited a return (loss) of 10%, then an investor in the fund would see a return (loss) of 20%.

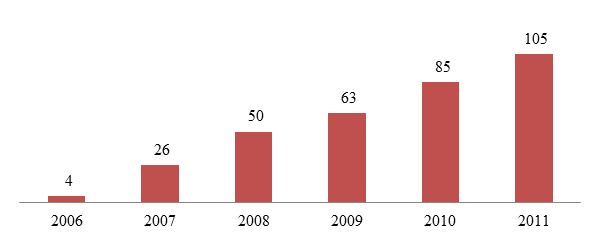

The first leveraged ETF was released by ProFunds in June 2006 and the number of funds has grown dramatically over the past half-decade.

Number of (US Domiciled) Leveraged ETFs from 2006 to 2011

SOURCE: Bloomberg L.P.

An important piece of information investors in leveraged ETFs need to be aware of is the effect of rebalancing. Rebalancing can best be explained by example. Let's say an investor uses $200 to buy some asset ($100 her own money and $100 borrowed) so that she is 2x leveraged. If the asset increases in price by 10%, the investor now has $120 after she returns the borrowed funds (assuming her friend doesn't charge interest). In order for our investor to have 2x exposure to the asset for the following day, she must rebalance her account so that the total amount invested is twice her investment (she must borrow $20 more dollars). After she borrows $20 more from her friend, she now has $240 invested in the asset and $120 net equity (regaining her 2x exposure).

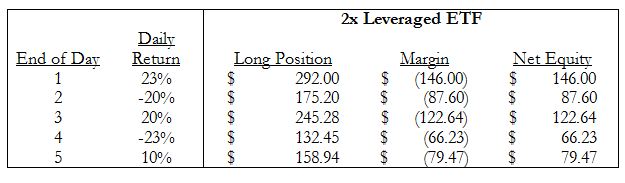

Leveraged ETFs must rebalance on a daily basis since at any time an investor could buy the fund and at that point the ETF needs to be of the appropriate leverage. The effects of rebalancing on buy-and-hold investors compound over time and lead to substantial deviations from expectations. We present the following table as an example of the compounding effect of rebalancing.

Hypothetical Scenario Illustrating the Effect of Rebalancing

Notice that the underlying asset has not appreciably changed in price ($0.01 five day return); however, the net equity value in the 2x Leveraged ETF experienced a 20% decrease. The take-away message from this is that buy-and-hold investors should not invest in leveraged ETFs unless they understand the risks associated with daily rebalancing.

Proshares discusses the rebalancing issue in some detail here and here. For further reading on this topic, we suggest taking a look at our paper on the effect of rebalancing on investors in ETFs.