Last week, Blackstone Real Estate Income Trust ("BREIT") announced that it was not going to honor redemption requests from investors in excess of 2% per month and 5% per quarter. In response, Blackstone's stock price fell 7% the first day and another 7% over the following week.

In this note, we explain how BREIT smoothed and inflated its reported returns for years, leading to extraordinary accolades, a prominent role in important regulatory debates and large investor inflows.[1] A run on the bank has started. Blackstone will be flooded with redemption requests it cannot honor without revealing BREIT's true NAV. Blackstone's prior conduct leaves it with two very bad options. It can honor redemption requests and see its NAV cut in half or it can severely limit redemptions for the foreseeable future until it can slowly adjust its reported NAV down to its true NAV.

Why Blackstone Real Estate Income Trust Matters

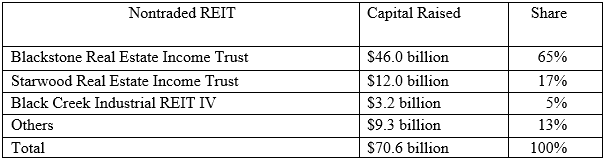

BREIT is a Monthly NAV non-traded REIT. It has accounted for almost all the capital raised by non-traded REITs in recent years as old-fashioned "lifecycle" non-traded REITs have been largely exposed for the high-cost, low-return, illiquid investments.

Table 1: Capital Raised by Nontraded REITs 2019-2022

Blackstone has been able to raise so much money from investors because it has reported high and steady returns relative to traded REITs while providing limited but sufficient redemption opportunities to appear nearly as liquid as traded REITs. BREIT reserves the right to halt redemptions altogether at any time in its sole discretion but has met redemption requests subject to a 2% of NAV per month, 5% of NAV per quarter limit. BREIT's redemption limits do not provide real liquidity. Compare the 2% monthly cap to the monthly trading in a traded REIT like Simon Property Group which has median monthly trading of 10% and mean trading of 15% of market capitalization. It is the illusion but absence of trading that makes BREIT NAV returns look good. Blackstone is telling investors that its reported returns are extraordinary but only allows no more than 2% of investors in any month to realize these returns.

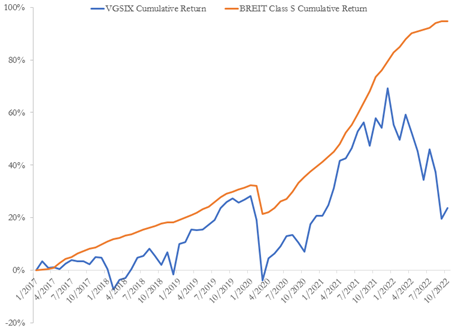

We made a presentation to a training program four weeks ago in which we discussed BREIT's relatively good performance compared to traded REITs. We pointed out that BREIT's NAV was certainly artificially smoothed and looked significantly inflated. BREIT holds $118 billion of mostly residential and industrial commercial real estate. These sectors' traded REITs have lost nearly 30% in 2022 while BREIT claims a 9% year to date return. As we explain below, this enormous gap between BREIT's claimed cumulative returns and traded-REITs' mark-to-market returns resulted from BREIT assuming its properties would be worth a lot more in the future than is implied by transaction prices. See Figure 1.

Figure 1: BREIT's Claimed Returns Far Exceed Its Peers, Especially in 2022.

Not Really Appraisals; BREIT Simply Assumes its Returns Will be Really Good!

BREIT's claimed returns are not based on property transaction prices or even based on property appraisals - Blackstone simply assumes the extraordinary returns BREIT reported.

According to its most recent 424B3, BREIT values $118 billion of real estate by assuming high single digit growth in net operating income, assuming exit cap rate of 5.4% and 5.5% and assuming discount rates of 6.9% and 6.8% for rental housing and industrial properties which account for the vast majority of its holdings.[2]

Every monthly 424B3 up to and including the one BREIT filed a month ago includes exactly this paragraph and table.[3]

These assumptions are determined by the Adviser, and reviewed by our independent valuation advisor. A change in these assumptions would impact the calculation of the value of our property investments. For example, assuming all other factors remain unchanged, the changes listed below would result in the following effects on our investment values:

BREIT's filing dated November 14, 2022 includes the following modified paragraph and table. We highlight a critical sentence Blackstone adds to the most recent 424B3 for the first time as stuff starts hitting the fan.

These assumptions are determined by the Adviser, and reviewed by our independent valuation advisor. In addition, the valuations for our two largest sectors (rental housing and industrial) assume high single digit net operating income growth in the near term given our below market rents and short duration leases. A change in these assumptions or factors would impact the calculation of the value of our property investments. For example, assuming all other factors remain unchanged, the changes listed below would result in the following effects on our investment values: [emphasis added]

Blackstone's belated disclosure highlights the significance of its assumptions in generating purported returns and partially reveals for the first time its sleight of hand.

BREIT uses a discounted cash flow ("DCF") model to calculate a present value for its residential properties. The basics of its DCF model are as follows. BREIT assumes net operating income will grow rapidly over a forecast period. It also assumes that the properties will be sold at a multiple of the assumed future net operating income equal to 1.00 divided by the assumed exit cap rate. For example, if BREIT assumes an exit cap rate of 5.0% it is assuming the property could be sold at 20 (1.00 ÷ 0.05) times the assumed dramatically higher future net operating income. Finally, BREIT discounts the future annual net operating income and terminal value based on the distant future net operating income and the assumed cap rate back to the present at an assumed discount rate.

Because Blackstone does this exercise every month with very slight changes in assumptions about discount rates and cap rates BREIT's NAV is smoothed. Also, since Blackstone has built in very substantial assumed future capital appreciation into its model, the NAV just keeps climbing with each passing month even if property values are falling.

What could go wrong?

BREIT's 424B3s illustrate the sensitivity of its valuations to the assumed exit cap rate and assumed cap in the tables excerpted above. Roughly speaking, if the exit cap rate Blackstone assumes is too low by 0.25% it inflates the investment values by over 3%. If the discount rate is too low by 0.25% it inflates the investment values by 2%. If both the assumed exit cap rate and discount rates are too low by 0.50% it inflates the investment values by 10%. Since BREIT is levered almost 2 to 1, those modest differences in assumptions would inflate BREIT's NAV by 20%.

BREIT didn't disclose it was assuming high net operating income growth from existing properties until just a few weeks ago. This assumption is critical because high assumed growth generated larger future annual distributions and, critically, higher terminal values at the end of the forecast periods. BREIT's properties are mature, income generating properties. Their long run valuations have to imply net operating income growth rates that are lower than the discounts rates used in the DCF. In fact, the exit cap rates assumed by BREIT are the amount by which the discount rate exceeds the long run rate of growth of net operating income growth. Despite acknowledging the discount rate will be 5% higher than the growth rate, BREIT is assuming growth rates greater than the discount rate over its projected future periods.

BREIT's assumed discount rates and assumed but non-disclosed high net operating income growth rates have symmetric impacts on valuations. Using BREIT's sensitivities to discounts rates we know that if BREIT's assumed growth rate is too high by 0.25% it inflates the investment values by 2%. There is good reason to believe BREIT's assumed but non-disclosed growth rate is a full 2% too high. Correcting BREIT's assumption of substantially above market growth rates, lowers its property values 15% and its NAV by 30%.

BREIT's outperformance is simply assumed.

BREIT has not delivered a 9% year to date return as it recently said. BREIT simply assumed its performance and assumed it was much better than any of its peers.

Conclusion

Until last week, there had not been sufficient redemptions to test BREITs purported valuations and returns. If BREIT's model-based NAV approximates the value of its underlying properties, BREIT could meet all redemption requests without the outperformance it has reported for years evaporating. If BREIT's NAV materially exceeds the true value of its properties, Blackstone will have to strictly enforce the redemption limits to protect the NAVs and prior claimed returns or meet redemptions requests and see its returns drop back in line with the long run return to traded REITs.

Blackstone can ride this out limiting redemptions to 2% per month but over time the gap between the BREIT cumulative value and the traded REIT benchmark will disappear. Blackstone had not been tested but now it is being tested and the truth is being revealed. Smart money is trying to get out of BREIT when the NAV is significantly overstated. Over the next year or two BREIT will fall 35% relative to the traded REIT index.

[1] The North American Securities Administrators' Association' attempts to put a 10% cap on direct participation programs, including non-traded REITs has been opposed by the industry, largely pointing to the growth and high, steady returns of BREIT. Problematically, counterfactually assuming Blackstone had found the secret sauce to large scale commercial real estate investing, if the concentration limit fails because of BREIT's capital raising prowess, reported outperformance and effective lobbying efforts, retail accounts will be loaded up with oil & gas DPPs and newly launched non-traded REITs not just BREIT.