We have been researching Reg D offerings. You can read our previous posts "Reg D Offerings Summary Statistics" here, "$8 Trillion of Broker-Sold Reg D Offerings" here and "HJ Sims Reg D Offerings: Heads Sims Wins, Tails their Investors Lose" here. You can download and print or email this post by clicking here.

I. Introduction

Regulation D issuers are not required to provide disclosures that are mandatory in registered offerings. Not only are Reg D issuers exempt from making the offering prospectus public, they are not required to file financial statements with the SEC or state regulators. This lack of transparency makes it extremely difficult for practitioners and researchers to gauge the financial soundness of Reg D issuers and monitor the performance of Reg D offerings.

In this note, we develop a proxy measure for the financial performance of Reg D offerings. Issuers are required to file registration documents with the Secretary of State (SOS) in the state where they are incorporated. Although these filings only include elementary information about the issuer, they inform the general public of the current business status of the issuer - An issuer with an "active" status has the legal right to transact business in the state while "inactive" issuers have lost that right. By linking the SEC's Reg D database with state SOS's business filing data, we estimate the number of Reg D issuers that have lost the right to transact business in their states of incorporation as a result of either a voluntary dissolution or a forfeiture of business registration for failing to comply with state law. This provides a lower bound on the issuers that have gone out of business.[4]

All 50 U.S. states make the filing status of business entities publicly available, either via a free search tool or upon request with a payment. 46 "open-records" states provide a free search or bulk data download service. The states of Arkansas, Delaware, New Jersey and Oklahoma charge a nontrivial fee for each entity search, precluding us from obtaining their data. By querying the exact names of the Reg D issuers in the 46 states' SOS business search systems, we identify 64,168 Reg D issuers which constitute 25.3% of all issuers that sold a Reg D offering between 2009 and 2022 and 90.3% of the Reg D issuers incorporated in the 46 states.[5]

The various registration statuses assigned to companies by states can be divided into four categories. (a) An active company is current with all the required filings and tax payments and its business registration is active. Such a company is in good standing and entitled to all the rights and protections under the state corporate law. (b) A voluntarily dissolved company has voluntarily closed its business by filing a certificate of dissolution or termination with the SOS. This means the company has chosen to wind up its business and terminate its existence based on a majority vote of shareholders as required by law.[6] (c) A merged or converted company ceases to exists by merging into another entity or moving its home state to a different state (also called "conversion" or "redomestication"). (d) A delinquent company is not in good standing for failure to comply with state regulations, including missing an annual report, failing to pay registration fee or taxes, failing to maintain a registered agent, and engaging in some other type of illegal activity.[7] A company in this category typically forfeits the right to transact business in the state and cannot sue or defend itself in a state court, and the directors or controlled persons of the company may become personally liable for a debt of the company.[8] We refer to issuers who are voluntarily dissolved, merged or converted and delinquent as inactive because they are not entitled to the full range of corporate privileges granted to companies with an active registration status.

Among the 64,168 issuers found in open-records states' SOS data, 32.3% have an inactive status, 14% were delinquent and 14.6% were voluntarily dissolved as of September 30, 2022. We also use the SOS data to calculate the probabilities of Reg D issuers becoming inactive and delinquent within any given year, and find that a Reg D issuer has a probability of 30.1% to be inactive and a probability of 13.5% to be delinquent within 5 years after selling the first Reg D offering. In contrast, the academic literature has established that the failure rate of SEC-registered companies is much lower than these rates.[9] Assuming the rate of a company being inactive or delinquent approximates the true failure rate of a company[10], our results indicate that Reg D issuers are at a much higher risk of failing than SEC-registered companies.

The remainder of this note is organized as follows. Section II discusses the state SOS databases' coverage of Reg D issuers. Section III presents summary statistics on inactive Reg D issuers in aggregate and broken out by issuer attributes. Section IV reports the probabilities of Reg D issuers becoming inactive and delinquent for each year of issuer age in aggregate and along several issuer attributes. The rates of inactive status and delinquent status are estimated separately for all Reg D issuers and issuers of broker-sold Reg D offerings. Section V concludes.

II. Reg D Issuers Identified in State SOS Databases

Table 1 summarizes state SOS databases' coverage of Reg D issuers. Among 253,888 issuers that sold an Reg D offering between 2009 and 2022, 151,042 (59.5%) are incorporated in Delaware and 71,041 (28%) are incorporated in the 46 open-records U.S. states. 64,168 Reg D issuers can be matched to a business entity in the open-records states' SOS databases using an exact name search, which account for 25.3% of all Reg D issuers and 90.3% of the issuers incorporated in the open-records states. This indicates that the business status summary statistics based on the SOS data presented in this blog post are representative of the Reg D issuers from the open-records states.

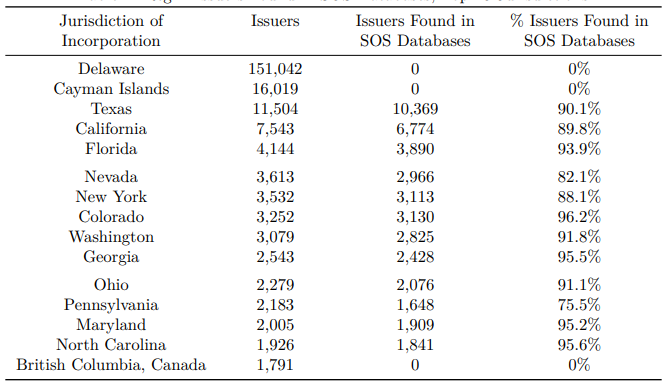

Table 1: Reg D Issuers Found in SOS Databases

Table 2 reports state SOS databases' coverage of Reg D issuers for each of the top 15 jurisdictions ranked by the number of issuers incorporated. Delaware is by far the most frequent state of incorporation for Reg D issuers, followed by Cayman Islands. Among the top 12 U.S. states for which SOS data is available, we are able to identify from the state SOS databases 76% of the Pennsylvania issuers, 82% of the Nevada issuers and more than 88% of the issuers incorporated in each of the other 10 states.

Table 2: Reg D Issuers Found in SOS Databases, Top 15 Jurisdictions

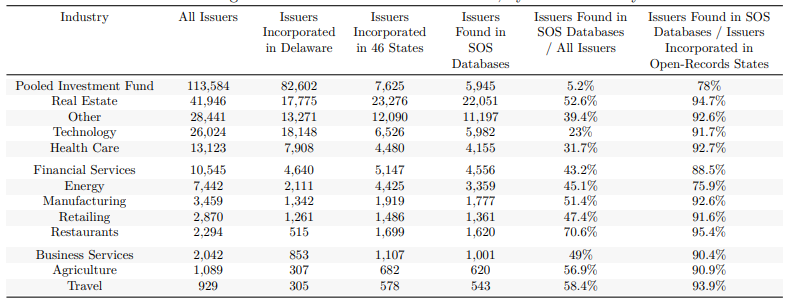

Table 3 shows that the state SOS databases' coverage of Reg D issuers varies across issuer industries. While only 5.2% of Pooled Investment Fund issuers can be identified from SOS data (because the majority of these issuers are incorporated in Delaware), we obtain SOS business status information for 52.6% of the Real Estate issuers, 45.1% of Energy issuers and 43.2% of the Financial Services issuers.

Table 3: Reg D Issuers Found in SOS Databases, by Issuer Industry

III. Inactive Reg D Issuers and Reg D Offerings Sold by Inactive Issuers

Table 4 reports summary statistics on Reg D issuers with an inactive status in the SOS databases downloaded between late September and early October of 2022. 20,755 (32.3%) of the issuers found in state SOS data had an inactive status as of September 30, 2022. 9,341 (14.6%) were voluntarily dissolved, 2,422 (3.8%) were merged or converted, and 8,992 (14%) were delinquent. Similarly, 27,676 (32.4%) of the Reg D offerings sold by issuers identified in the SOS data were sold by inactive issuers. Voluntarily dissolved, merged or converted and delinquent issuers account for 11,215 (13.1%), 4,621 (5.4%), and 11,841 (13.8%) of the Reg D offerings sold by identified issuers, respectively.

Table 4: Inactive Issuers as of September 30, 2022 and Reg D Offerings Sold by Inactive Issuers

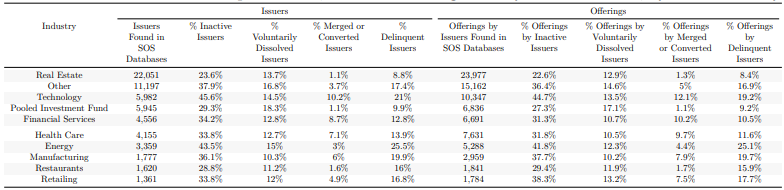

Table 5 breaks down the inactive issuers summary statistics by issuer industry for the 10 industries with the most issuers found in SOS data. The Technology industry has the highest percentage of inactive issuers (45.6%) and offerings sold by inactive issuers (44.7%), followed by the Energy industry where 43.5% of the issuers are inactive and 41.8% of the offerings were sold by inactive issuers. Issuers from the Energy industry are also the most likely to run afoul of state filing and tax requirements with 25.5% of Energy issuers listed as being delinquent, which sold 25.1% of Reg D offerings in the Energy industry. 18.3% of Pooled Investment Fund issuers have voluntarily dissolved their business, a percentage higher than any other industry. Issuers from the Technology industry have a higher probability to consolidate into another entity or change jurisdiction, with 10.2% of Technology issuers reported as being merged or converted.

Table 5: Inactive Issuers as of September 30, 2022 and Offerings Sold by Inactive Issuers, by Industry

Table 6 presents summary statistics on inactive issuers by issuer type for the 3 most common issuer types. 37.9% of the issuers formed as corporations have become inactive by September 30, 2022, a percentage higher than the other 2 issuer types. Corporation issuers also have the highest rate of delinquent status, with 17.4% of Corporation issuers having a delinquent status. 12.4% of the issuers formed as limited liability companies are delinquent, and these delinquent LLCs account for 11.9% of Reg D offerings sold by LLC issuers. Limited partnership issuers have the highest rate of voluntary dissolution (about one fifth).

Table 6: Inactive Issuers as of September 30, 2022 and Offerings Sold by Inactive Issuers, by Issuer Type

Table 7 presents summary statistics on inactive issuers by disclosed issuer size. While most issuers chose not to disclose either revenue or aggregate net asset values (NAV), we sort those that made the disclosure into five categories by revenue and NAV. The smallest issuers (those with a revenue of no more than $1 million or NAV of no more than $5 million) have the highest rate of inactive status (43.7%) and the highest rate of delinquent status (21%). The mid-sized issuers (revenue between $5 million and $25 million or NAV between $25 million and $50 million) are about half as likely to be delinquent as the smallest issuers (11.4%), and the rate of delinquent status of the largest issuers (revenue over $100 million or NAV over $100 million) is only a third of that of the smallest issuers (7%). The issuers that chose not to disclose any information about their size have similar rates of inactive status and delinquent status to mid-sized issuers, indicating that the average size of issuers disclosing no size information may be close to that of a mid-sized issuer.

Table 7: Inactive Issuers as of September 30, 2022 and Reg D Offerings Sold by Inactive Issuers, by Issuer Size

IV. Inactive and Delinquent Rates of Reg D Issuers

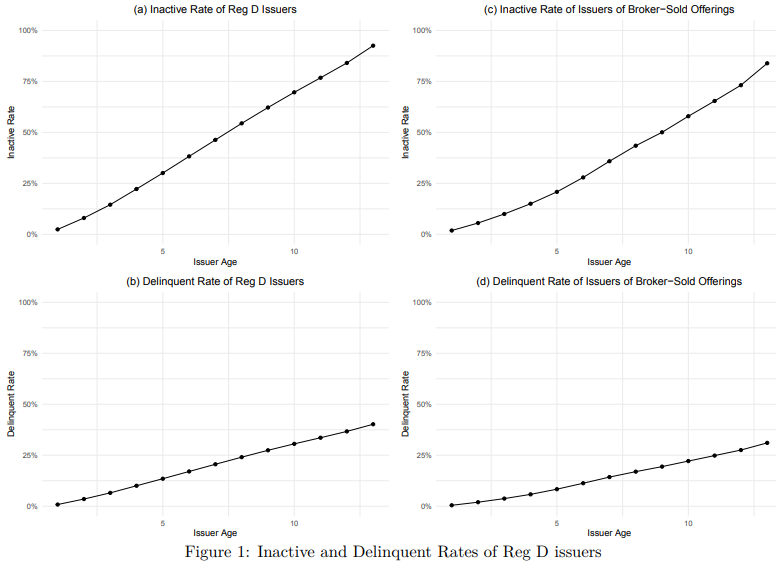

This section reports findings of a survival analysis of all Reg D issuers and the issuers that sold Reg D offerings via a broker-dealer. Figure 1(a) illustrates the probability of a Reg D issuer becoming inactive (i.e., voluntarily dissolved, merge or converted, or delinquent) within n years of the issuer's first Reg D offering for n=1,2,...,13.[11] Figure 1(b) presents the probability of a Reg D issuer becoming delinquent within n years of the issuer's first Reg D offering. The probability of a Reg D issuer becoming inactive within 5 years of the first offering is 30.1%, whereas 13.5% of Reg D issuers become delinquent within 5 years of the first offering. Within 10 years of the first offering, 69.7% of Reg D issuers become inactive and 30.6% of Reg D issuers become delinquent. Reg D issuers stay active for an average of 7 years.

Figures 1(c) and (d) illustrate the probabilities that an issuer of a broker-sold Reg D offering becomes inactive and delinquent, respectively, within n years of the issuer's first Reg D offering for n=1,2,...,13. Issuers that sold Reg D offerings via broker-dealers tend to remain active for longer than those selling Reg D securities without a broker-dealer - 20.8% of the issuers of broker-sold offerings become inactive within 5 years of the first offering and 57.9% become inactive with 10 years of the first offering. Issuers of broker-sold Reg D offerings are also less likely to become delinquent, with 8.3% of the issuers of broker-sold offerings becoming delinquent by the 5th year and 22.1% becoming delinquent within 10 years of the initial sale. Issuer of broker-sold Reg D offerings stay active for 8.1 years on average.

Figure 1: Inactive and Delinquent Rates of Reg D Issuers

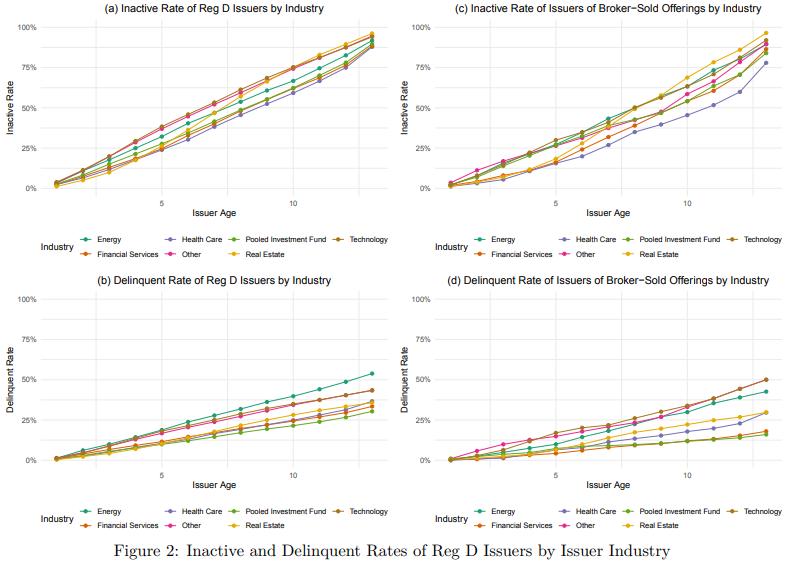

Figures 2(a)-(d) illustrate survival probabilities of Reg D issuers by issuer industry for the 7 industries with more than 3,000 issuers found in SOS databases. Figure 2(a) shows that the Technology and Other industries have the highest rates of inactive status in every year up to the 10th year after the first offering. It is also noteworthy that the rate of inactive status for issuers from the Real Estate industry increases more quickly than any other industry from Year 3 to Year 10 and becomes the highest of all industries in Year 11. According to Figure 2(b), the Energy industry has the highest rate of delinquent status for each year of issuer age while the Pooled Investment Fund industry has the lowest rate of delinquent status for most issuer age years. No industry has a clearly higher rate of inactive status than others when it comes to issuers of broker-sold offerings although the Health Care industry has the lowest rate of inactive status (Figure 2(c)). A comparison of Figure 2(d) with Figure 2(b) shows that the delinquent rate of issuers of broker-sold offerings is lower than the delinquent rate of all Reg D issuers in each year of issuer age for most industries except Technology and Other, each of which has a higher rate of delinquent status for issuers of broker-sold offerings from Year 11 to 13.

Figure 2: Inactive and Delinquent Rates of Reg D Issuers by Issuer Industry

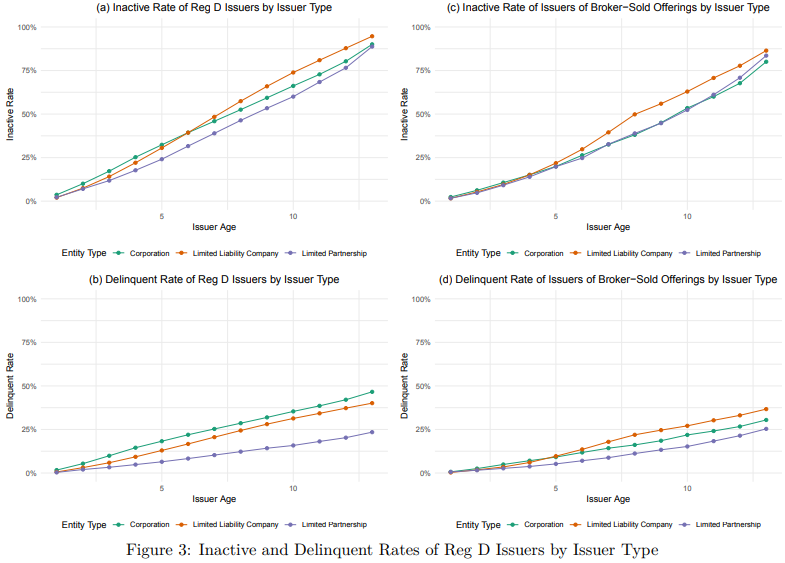

Figures 3(a)-(d) illustrate survival probabilities of Reg D issuers by issuer entity type for the 3 most common issuer types. Corporation issuers have the highest rate of inactive status until Year 5 and LLC issuers are the most likely to become inactive in each year of issuer age starting from Year 7. Corporation and limited partnership issuers have the highest and lowest rate of delinquent status in each year of issuer age, respectively. As for broker-sold offerings, LLC issuers have the highest rates of inactive status and delinquent status in each year of issuer age starting from Year 5, while corporation issuers of broker-sold offerings are the most likely to become delinquent before Year 5.

Figure 3: Inactive and Delinquent Rates of Reg D Issuers by Issuer Type

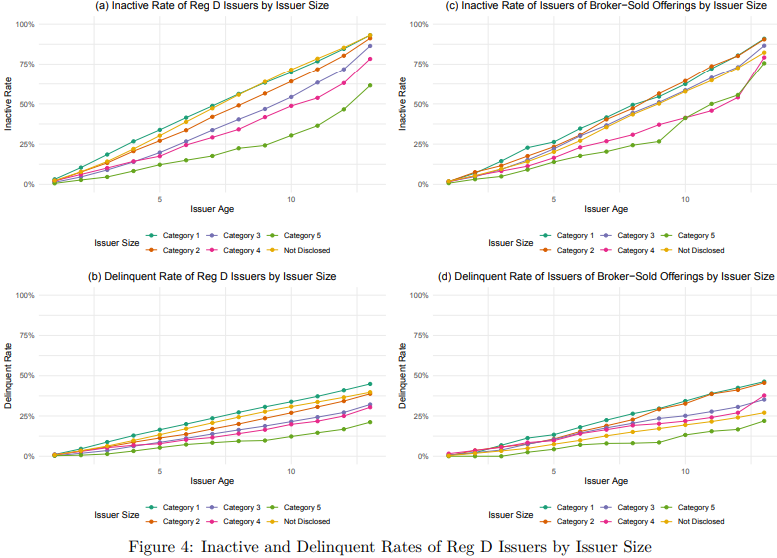

Figures 4(a)-(d) illustrate survival probabilities of Reg D issuers by disclosed issuer size.[12] The smallest issuers (Category 1) and issuers that do not disclose size have the highest rates of inactive status and delinquent status in each year of issuer age, followed by the second smallest issuers (Category 2). The largest issuers (Category 5) are more likely to remain active and compliant than issuers from any other size category in each year of issuer age. When it comes to broker-sold offerings, the issuers from the bottom two categories have higher rates of inactive status and delinquent status in most issuer age years, while issuers of broker-sold offerings that do not disclose size appear to remain active and compliant for somewhat longer than mid-sized issuers (the yellow line lies below the blue line in Figures 4(c) and 4(d)).

Figure 4: Inactive and Delinquent Rates of Reg D Issuers by Issuer Size

V. Conclusion

Whether a company maintains an active business license with its state of incorporation is public information available from the state SOS's office. By searching issuer names in state SOS data, we identify the business status of over 90% of the Reg D issuers incorporated in 46 open-records U.S. states. Among issuers that sold Reg D offerings between 2009 and 2022, 32.3% had an inactive status and 14% were delinquent as of September 30, 2022. A Reg D issuer has a probability of 30.1% of becoming inactive and a probability of 13.5% of becoming delinquent within 5 years of its first Reg D offering. These rates are much higher than the well documented failure rate of registered companies, indicating the greater risk and unpredictability associated with Reg D issuers' business models.

[1] Craig McCann can be reached at craigmccann@slcg.com.

[2] Chuan Qin can be reached at chuanqin@slcg.com.

[3] Mike Yan can be reached at mikeyan@slcg.com.

[4] Some companies keep filing registration reports and remain active even after they file for bankruptcy to wind up their business operations in an orderly manner.

[5] The state SOS data was downloaded between mid-September and early October of 2022.

[6] Winding up a company requires paying off business debts and distributing any remaining assets to the members, and before doing so the company is required to cure all the filing and tax deficiencies with the state.

[7] The large majority (40) of the states adopt the practice of actively assigning a "delinquent" or "forfeited" status to noncompliant companies. The remaining 6 states either label very few noncompliant companies as delinquent (Connecticut, New York, Ohio and South Carolina) or do not publish a delinquent designation at all (Alabama and Pennsylvania), either because they do not require an annual report filing or appear to be reluctant in publicly labeling a noncompliant business entity delinquent.

[8] While some delinquent companies restore to good standing by filing missed reports or paying overdue fees, most remain delinquent until they are administratively dissolved or terminated by the state. Most states allow a grace period from a few months to a few years for noncompliant companies to reinstate their status before permanently revoking their registrations. For example, Georgia starts the proceeding to dissolve a company administratively if it fails to pay its annual registration fee within 60 days after it's due, and Nevada revokes a business entity's charter after it's in default for a year.

[9] See, for example, Anagnostopoulou, Seraina C. & Gounopoulos, Dimitrios & Malikov, Kamran & Pham, Hang, 2021. "Earnings management by classification shifting and IPO survival," Journal of Corporate Finance, Elsevier, vol. 66(C). It can be seen from Table 1 of this paper that only 16 (or 4.0%) of the 402 IPOs issued in 2004-2013 failed in the first 5 years.

[10] As discussed above, the number of inactive companies may be a lower bound for the number of companies with financial difficulties because inactive companies have lost the right to do business in their states of incorporation and some bankrupt companies may remain active while going through legal proceedings.

[11] The maximum number of years for which we can calculate the survival rates is 13 because the Reg D offering data has a time range from 2009 to 2021.

[12] Categories 1-5 represent the issuer size category displayed from row 2 through 6 in the first column of Table , i.e., Category 1 includes the smallest issuers and Category 5 includes the largest issuers.