Mar 2018

... Paying a premium purchase price over the Indicative Value of the ETNs could lead to significant losses in the event the investor sells such ETNs at a time when such premium is no longer present in the market place or such ETNs are accelerated (including at our option, which we have the discretion to do at any time), in which case investors will receive a cash payment in an amount equal to the Closing Indicative Value on the Accelerated Valuation Date (each as defined herein). Investors should consult their financial advisors before purchasing or selling the ETNs, especially for ETNs trading at a premium over their indicative value. ...[January 29, 2018 Pricing Supplement, p.2]

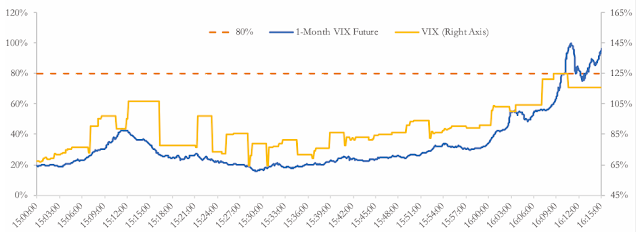

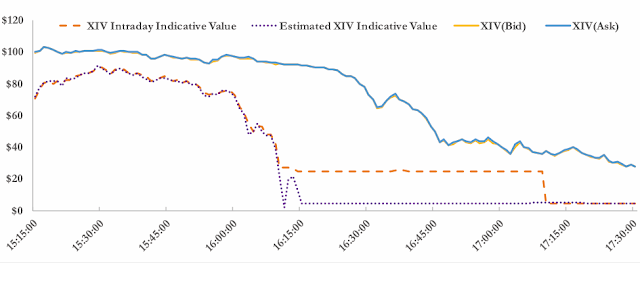

... If the price of the underlying futures contracts increases by more than 80% in a day, it is extremely likely that the Inverse ETNs will depreciate to an Intraday Indicative Value or Closing Indicative Value equal to or less than 20% of the prior day's Closing Indicative Value and will be subject to acceleration if we choose to exercise our right to effect an Event Acceleration of the ETNs. ...[January 29, 2018 Pricing Supplement, PS-28; emphasis added]This excerpt from the Pricing Supplement demonstrates that Credit Suisse knew, independent of any calculation by Standard and Poor's, that an 80% or slightly greater increase in the price of the February and March VIX futures contracts would cause the Indicative Value to breach the threshold which would give Credit Suisse the option to redeem all XIV shares.3