Feb 2018

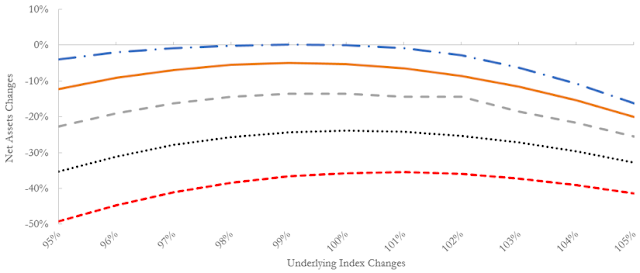

"The Fund seeks to achieve its investment objectives by capturing gains on options sold on S&P futures contracts that can be purchased ("closed") at a later date for a lower price than the price realized when originally sold.... In the aggregate, the Fund is typically "net short" in the portfolio of contracts that it holds, which means that the Fund holds more uncovered option contracts than covered."