Continuing our blog posts and working papers on non-traded REITs, today we report on how investors fared in five non-traded REITs sponsored by affiliates of The Inland Real Estate Group of Companies.1 Inland raised over $18.1 billion from investors in these REITs. Inland's affiliated companies served as conflicted property managers, dealer managers, and business managers (see one of our early blog posts on the interrelated entities involved in Inland American Real Estate Trust).

Two of the five non-traded REITs, Retail Properties of America (RPAI) and Inland Real Estate Corporation (IRC), became listed REITs, Inland Retail Real Estate Trust merged with a publicly-listed REIT, Developers Diversified REIT (DDR), and Inland Diversified Real Estate Trust last week announced a merger with Kite Realty Group (KRG). Inland American Realty Trust has not listed or merged with a listed REIT but has provided an updated net asset value (NAV) per share.2

We gathered data on gross proceeds, distributions, and share redemptions from the REITs' SEC filings, starting from each REIT's registration date, up to the earliest of today or the day the REIT's shares first listed on an exchange.3 We calculate the market value of the common shares at the time each REIT's shares became publicly listed, a merger was announced, or the REIT last reported an NAV per share. We refer to this market value as the value of the REIT upon price discovery (see Table 1 below).

We apply the daily net investment in each of the non-traded REITs to the Vanguard REIT Index (VGSIX) - a liquid, diversified mutual fund of traded REITs. We compare the market value of the common shares of the non-traded REITs upon price discovery to the value of an equal size investment in the diversified traded REIT mutual fund to determine whether investors benefited from their involvement with Inland's non-traded REITs.

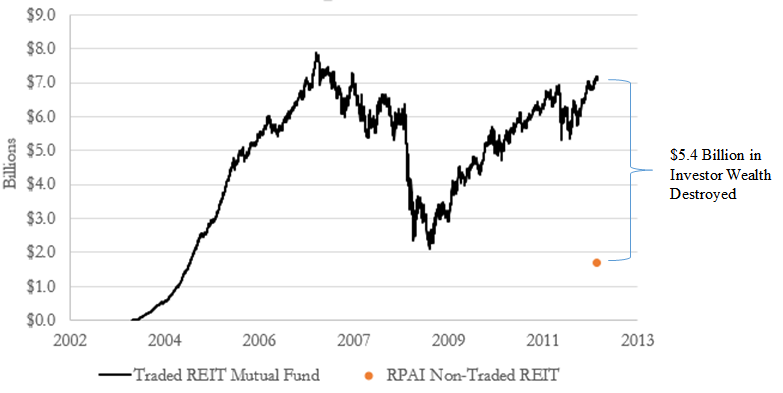

For example, the black line in Figure 1 plots the value of RPAI gross proceeds invested in the Vanguard traded REIT mutual fund. RPAI listed one-fourth of its common shares on the NYSE on April 5, 2012 and its remaining non-traded shares became listed over the following 18 months. RPAI's 194 million postreverse-split shares were worth $1.7 billion (denoted by the orange dot on the figure) on April 5, 2012. The same $4.9 billion invested in diversified, liquid traded REITs would have been worth $7.1 billion. RPAI thus managed to destroy $5.4 billion or 76% of real estate investors' wealth.

Figure 1. RPAI Investors Lost $5.4 billion or 76% Compared to Diversified Liquid REITs

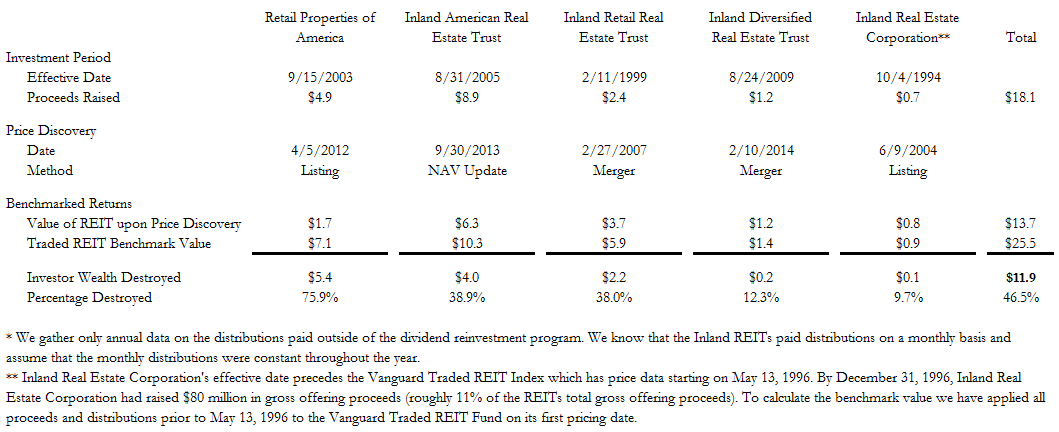

Table 1 summarizes our analysis for the five Inland non-traded REITs (click the image to enlarge). We find that investors' $18.1 billion combined net investment in Inland's five non-traded REITs was worth $13.7 billion on their price discovery date. Had stockholders invested the same $18.1 billion over the same time period in traded REITs, they're investments would have been worth $25.5 billion. Thus, Inland has destroyed $11.9 billion or 46.5% of real estate investors' wealth through its non-traded REITs.

Table 1. $12 Billion Aggregate Investor Wealth Destroyed by Inland's Non-Traded REITs* (Dollar amounts are in billions)

_______________________________________

1. There is a sixth Inland non-traded REIT called Inland Real Estate Income Trust that commenced its initial public offering in October 2012 and has not listed, merged with a listed REIT, or provided an updated net asset value per share. We exclude this REIT from our analysis because there is no information on its market price.

2. Inland American reported a $6.93 NAV per share as of September 30, 2013. While equal to the REIT's dividend reinvestment and share repurchase program price, the NAV is 14.5% higher than observed secondary market trade prices for Inland American's shares. In our calculations we use Inland American's September 30, 2013 NAV in calculating a likely upper bound for the market value of its common shares, likely underestimating investor losses.

3. We have gathered data from prospectus supplements (424B3) filings and annual reports (10-K) for all of the REITs. Additionally, we have gathered data from the quarterly reports (10-Q) from the date of the last annual report until the listing of the common shares, the announcement of merger, or most recent update to the NAV.