Most research on structured products focuses on what is known as initial date mispricing -- the difference between what a product costs and how much it is worth, as of the issue date. If you look at any of our structured product reports (let's take this reverse convertible, for example), you can see that the product was issued at a price of $1,000, but that the present value of its resulting cashflows only comes out to $960.40. The difference, $39.60 or 3.96%, represents an expected loss to the investor. We and others have documented issue-date mispricing on many types of structured products -- for example: reverse convertibles, dual directionals, absolute return barrier notes, etc.

But you might be wondering, how have structured products actually performed? Have structured product investors actually fared well, or poorly? These are pretty tricky questions. In order to answer it for any given time period, you would have to look at how the value of all outstanding structured products changed on each day. But since structured products don't have liquid secondary market prices, you would have to actually value each structured product on each day, and aggregate the returns to see how structured products as a whole have performed.

In our latest research paper, released today, we do exactly that. We use our sample of over 18,000 structured products and value every outstanding structured product in that sample every day, then weight each return by the face value of the note and combine those returns. The result is an index of ex post structured product returns, which we calculate over a period from 2007 to April 2013.

We also calculate subindexes for four popular structured product types: reverse convertibles, single-observation reverse convertibles, autocallables, and tracking securities. These indexes show the ex post returns to large numbers of products over time.

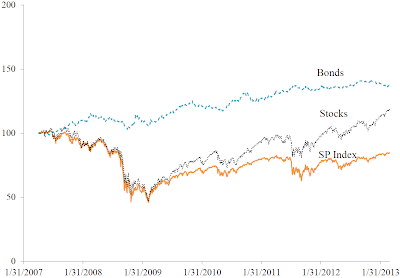

But to answer the question: structured product returns have been poor. Structured products as a whole have had lower returns than either bonds or stocks over this period, as have each of the four subtypes we have studied. In addition, structured product returns are highly correlated with the S&P 500, suggesting little diversification benefit.

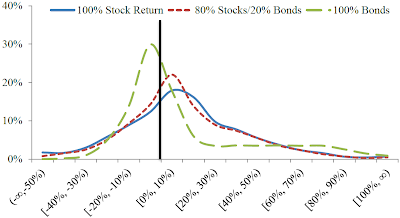

We have also studied the performance of individual structured products. We find that the majority of structured products underperformed stock and bond portfolios -- see Table 6 and Figure 8 (reproduced below). In the following figure, we plot how frequently stock and bond portfolios overperform structured products, measured by the difference between the returns on stock and bond portfolios and contemporaneous structured product returns. The black bar marks a 0% difference in returns.

The fact that the majority of the weight in each of the above distributions is found to the right of the black bar indicates that stock and bond portfolios generally overperform contemporaneous structured products. To our knowledge, this is the first large-scale study of ex post US structured product returns. We encourage you to check out the paper for details on our methodology and results, which we think have import implications for structured product investors.