SLCG Research: Structured Product Based Variable Annuities

Sep 2013

In 2010, AXA Equitable began issuing a new kind of variable annuity that, in addition to traditional mutual fund-like subaccounts, also included an option for a structured product-like crediting formula linked to an underlying index such as the S&P 500. Our firm had done a lot of work on both structured products and variable annuities, so in late 2011 we started analyzing the structured product embedded in AXA's product, eventually writing a short research paper on the subject which we released in early 2012. In this paper, we warned about the complexity of this type of annuity, and showed how its value to investors was critically dependent on the cap level and expectations about future volatility -- features that most retirement investors might not fully appreciate.

Since then, the idea of a structured product based variable annuity (spVA) has apparently taken hold. Not only has the originalAXA Structured Capital Strategies sold over $2.2 billion since it was issued, but MetLife has introduced their Shield Level Selector product, which has many of the same features as the AXA Structured Capital Strategies Variable Annuity including the embedded structured product option. Moreover, Allianz has recently filed a prospectus for their Index Advantage annuity which also embeds structured product-like crediting options. With all these changes in the marketplace, we decided to completely revise our previous paper on spVAs, and we are happy to announce that it is now available on SSRN and the SLCG website .

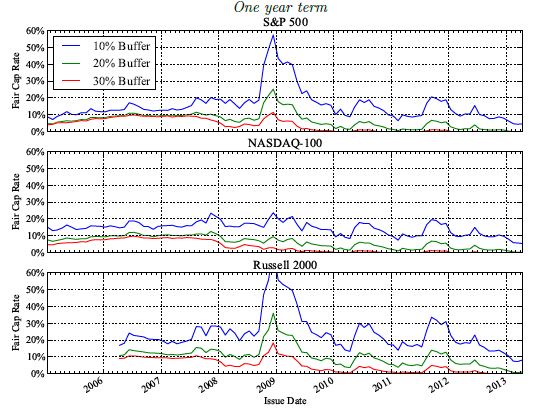

In it, we review each of the three currently available spVAs, highlighting their key similarities and differences. One of the most important features of spVAs is the embedded cap on index-linked returns. The cap is chosen by the issuer, and as we had shown previously, has a huge effect on the value of the annuity. In our paper, we solve for the cap level that would compensate investors for their exposure to the underlying index. We calculate the fair cap levels for three underlying indexes (S&P 500, NASDAQ 100, and Russell 2000) at various buffer levels and terms, all the way back to 2005. We also provide extensive backtesting of spVA crediting formulas.

spVA Fair Cap Levels Over Time

One of our key findings is that the fair cap level is very dependent on current market conditions, especially the implied volatility of the underlying index. This fair cap level is often surprisingly high, and in some market conditions, there in fact exists nocap level that could fairly compensate investors for certain spVA crediting formulas.

Investors considering an spVA should understand that their choice of buffer level, term, and underlying index make a big difference in how their account accumulates over time. We argue that spVAs are markedly different investments than traditional variable annuities, and their additional complexity makes comparing their features very difficult. We hope that our paper offers some insight into how to make those choices, or whether to purchase an spVA at all.