In the past few months, we have constructed a database of thousands of structured certificates of deposit (CDs). We have analyzed and evaluated hundreds of these CDs and have compiled these results into a recently completed study . Our results indicate that structured CDs are usually issued at significant discounts to face-value (comparable to structured products), offer little if any market exposure and are often less valuable than contemporaneously issued fixed rate CDs.

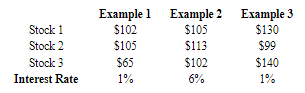

We've recently come across a structured CD that has some interesting features and we thought we'd take this opportunity to talk about them in some detail. This particular structured CD pays interest annually at a minimum rate of 1% per annum for five years. It adds additional contingent interest based on the prices of three common stocks, known as the 'basket'.

The price of each stock in the basket is observed annually. For a given observation date, if all of the stock prices are at least as high as their respective initial prices when the CD was offered, then the CD pays an additional 5%. This type of position is known generally as a binary dispersion option, specifically a 'worst-of' binary option (we have covered the basics of binary options in a previous post). The following table walks through some examples of this calculation, assuming each stock's initial value is $100.

At maturity, the issuing bank will return principal and the final interest payment. The FDIC views each of the interest payments as "incalculable" prior to their crediting and as a result investors are exposed to the credit risk of the issuing bank before these coupons are paid.

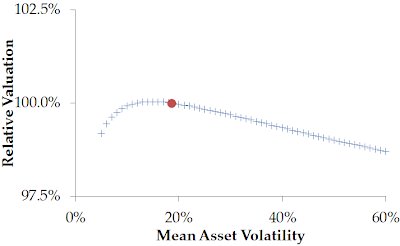

This particular CD's value depends on the characteristics of the underlying common stock prices. For example, if the stock prices are not volatile enough, then when the price of one stock dips below its initial price, the likelihood of increasing back above the initial level is relatively low. Similarly, if the stock prices are too volatile, there is an increased likelihood that any one of the stocks will decrease in price below its initial price. We have valued the product for different levels of average volatility and have produced the following figure.2

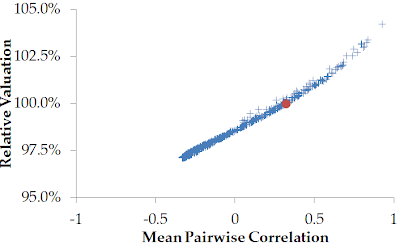

The value of the structured CD also depends on the correlation of the underlying assets.1 If the underlying assets are generally negatively correlated, then if one of the assets increases above its initial price, one of the other two assets will likely decrease in price. As a result, we generally expect the product to be more valuable as the average pairwise correlation increases. We have valued the product for various levels of average pairwise correlation and have produced the following figure.

In addition to the dependence on volatility and correlation, the structured CD's value also depends on the skewness of the underlying return distributions. If any of the underlying stocks have a return distribution that is very negatively skewed (higher probability of negative returns than positive returns), the deposit will decrease in value relative to the case where each of the stocks has a normal return distribution.

We have determined that there is about a 30% chance that an investor would receive any additional payments from the market exposure throughout the term of the deposit (ignoring skewness). We find that the structured CDs with this market exposure are at best comparable in value to contemporaneously issued fixed-rate CDs.

It's unlikely that investors will appreciate the complicated dependence this particular structured CD has on the characteristics of the underlying assets. It will be interesting to see if other products with similar structure continue to be issued.

_______________________________________

1 The returns of two assets are said to be positively correlated if the two assets generally increase and decrease in price at the same time. On the other hand, the returns of two assets are said to be negatively correlated if when one asset increases/decreases in price, the other asset decreases/increases in price. 2By relative valuation we mean the value of the CD with the altered parameter(s) divided by the value of the CD with observed market parameters. As a result, the relative valuation for a CD with no alteration of parameters is 1 (100%).