Financial innovation is typically associated with banks, but lately we've seen a number of new financial products developed and sold by insurance companies. Some of the most interesting products are known as insurance-linked securities, or ILS.

In the broadest sense, ILS transfer risk from insurance companies to investors. The largest segment of the ILS market is in catastrophe bonds (or 'cat bonds' for short), whose interest and principal payments depend on a specifically defined natural disaster or other major insurable event not happening. Insurance companies issue ILS in order to sell risk to investors when traditional reinsurance companies are unwilling or unable to accept that risk at acceptable prices.

According to Swiss Re, ILS came about in response to Hurricane Andrew in 1992. The extreme damage caused by that storm left insurance companies, and the reinsurance companies that back them, with extensive losses and reduced reserves for further catastrophic events. The 2005 hurricane season, which included hurricane Katrina among others, also encouraged insurance companies to divest their risk exposure to capital markets. Effectively, the risks of insuring against disasters became so large that insurance companies began selling that risk to institutional investors, such as hedge funds, other insurers, and pension funds.

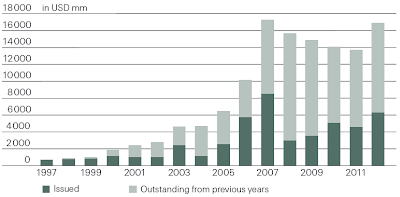

The market for ILS has grown significantly over time, according toa recent report from Swiss Re, and new issuance is approaching the pre-crisis high.

Source: Swiss ReInsurance-Linked Securities Market Update, January 2013

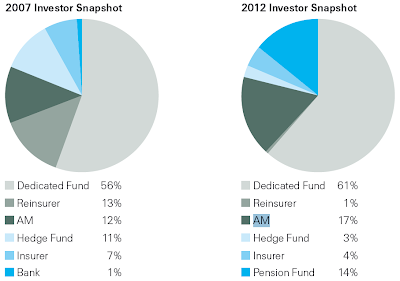

Interestingly, pension funds have purchased a larger share of the ILS market over the last few years.

Source: Swiss ReInsurance-Linked Securities Market Update, January 2013

However, there may be an adverse selection problem when insurance companies sell risk to outside investors. If insurance and reinsurance companies are the best firms for understanding and predicting losses, then they will only sell risk exposure when the market underprices it -- i.e., when the insurance company expects to profit from the sale. Pension funds, perhaps under pressure to deliver better than market rates of return, might underestimate these risks and thereby expose their investors to catastrophe-related insurance losses.

How large those losses might be can be difficult to determine even months or a year after an event (see the discussion of Hurricane Sandy in the Swiss Re report). ILS use complex criteria to determine whether a disaster or other event qualifies for coverage, and each ILS covers only specific types of events and particular geographic areas in which the disaster must occur. How transparent those criteria are can vary from one ILS to another ILS and are not standardized across the industry. Some ILS may also expose investors to a broader range of insurance-related losses, including operational risks of particular insurance companies.

ILS are a relatively new financial product and will likely evolve over time. But in current form, institutional investors may be exposed to the risk of a major catastrophe -- even if that catastrophe happens in a different state or country.