Dodging Hedge Fund Requirements: The Case of Mariner Access

Jun 2013

Nowadays, there are several ways that retail investors can purchase risky investments which would typically be considered unsuitable. For example, many exchange-traded funds (ETFs) use derivatives to offer investors access to risky asset classes (such as CDOs) or complex options positions (such as covered calls). Since ETFs can be bought and sold like any other listed stock, essentially any investor can now take covered call positions regardless of her understanding of options. There is even talk of allowing hedge fund investments in mutual funds(such investments are typically restricted to wealthy and sophisticated investors).

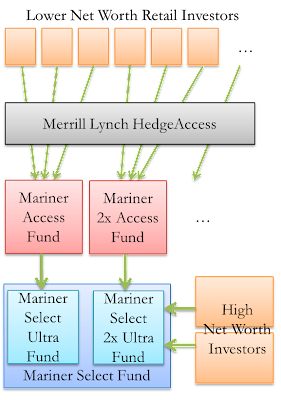

But trying to sell restricted hedge fund units to retail investors is nothing new. Take for example the Mariner Access Fund and the Mariner 2X Access Fund offered through the Merrill Lynch HedgeAccess program. The HedgeAccess program was designed by Merrill Lynch for the purpose of facilitating access to hedge third-party funds at reduced minimum investment requirements.

The Mariner Access Fund and the Mariner 2x Access Fund were feeder funds for third-party hedge funds Mariner Select Ultra Fund and Mariner Select Ultra 2x Fund, respectively. Each of these third-party funds invests through a master fund called these Mariner Select Fund. Mariner Investment Group, Inc. served as the investment manager for the master fund.

The Mariner Access Fund and the Mariner 2X Access Fund effectively bypass minimum investment requirements of the Mariner Select Ultra Funds to allow investors with a lower net worth to access these funds. According to their SEC filings, a minimum of $100,000 was required for investing in both the Mariner Access Fund and the Mariner 2X Access Fund while the Mariner Select Ultra Fund and the Mariner Select Ultra 2x Fund each required minimum investments of $5,000,000.* The combined interests sold by the access funds are approximately $408 million according to their latest SEC filings (available here and here).

The Mariner Investment Group funds, as is typical of hedge funds, have virtually no limits to their investment strategies. The funds may allocate their cash balances to investments as speculative as distressed securities--that is, the debt or equity of companies whose business is impaired by high debt or illiquidity and that may require debt restructuring.

Hedge funds often claim that their returns diversify stock and bond portfolios, but this claim is dubious. Hedge fund managers have significant leeway over how they report returns, which are frequently reported on a lag (are either "stale" or "managed").This can lead to Sharpe ratios that are overreported by as much as 65%.** This reporting bias also results in a decreased correlation with traditional asset classes and a decreased volatility of reported returns,*** which will overstate diversification benefits and underestimate risks. Unsophisticated investors would likely not appreciate these esoteric facts and could be duped into hedge fund investments by the misuse of simplistic risk measures.

So even if Merrill Lynch's claims that the HedgeAccess program would have benefits for investors such as "advantageous redemption and exchange privileges compared to investing in the Underlying Funds directly," this does not change the fact that investments in the underlying funds were incredibly risky and opaque. The reduced minimum purchase requirements leave open the question of whether or not such 'access' funds are suitable for the targeted investor. Indeed, it also questions whether ETFs and mutual funds should purchase such assets, given that their shares could be purchased by unsophisticated investors.

_______________________________________

*Direct investment in the master fund (Mariner Select Fund) required a minimum investment of $1,000,000. ** Lo, "Statistics of Sharpe Ratios" Financial Analyst Journal (July/August 2002). *** See, for example, Asness, Krail and Liew, "Do Hedge Funds Hedge?" Journal of Portfolio Management (Fall 2001) and Brooks and Kat, "The Statistical Properties of Hedge Fund Index Returns and Their Implications for Investors" The Journal of Alternative Investments (Fall 2002).