Okay, we've talked a bit about what structured CDs are and why we think they are interesting. But what does a structured CD offering document actually look like? Unfortunately, it isn't possible to find such documents from Bloomberg or the SEC website since structured CDs are not registered securities. However, you can often find offering documents using Google. For example, as a relatively simple equity-linked CD, we're going to take a look at the "Global Opportunity Certificate of Deposit with Minimum Return" which was issued by HSBC in May 2012 with the CUSIP40431GS75 .

This product is linked to not one but several securities, referred to as the underlying 'basket,' which includes in equal parts the Dow Jones Industrial Average, the Dow Jones EURO STOXX 50 Index, and the TWSE (Taiwan Stock Exchange) Index. Basket products are common among both structured CDs and structured products, and are one way issuers can add complexity/diversification to the product. The final payout at maturity is subject to a minimum return of 0.75% corresponding to an annual percentage yield of 0.10% for the seven year product.

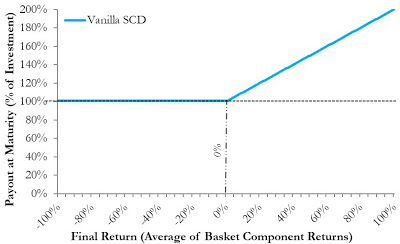

The payoff for this type of product is shown below, and is very similar to structured products known as principal-protected notes:

This payout diagram also resembles that of a long call option, except with the return of original principal paid. Therefore, this product can be modeled as the combination of:

A zero-coupon bond with a single payment at maturity of the initial investment amount plus 0.75%, and

A call option on the underlying basket with a strike price that is in-the-money by 0.75%.

The bond component's value will be less than the payout at maturity due to the time value of money. However, unlike structured products, this component is FDIC insured such that it is not subject to the credit risk of the issuer (we'll discuss the implications of FDIC insurance in tomorrow's post).

The call option for this simple product is somewhat complex -- referred to as an "average price option" or "Asian option". The payoff of this particular structured CD depends on the quarterly average portfolio level during the term of the CD. If the average portfolio level (determined by the 28 quarterly observation dates) is higher than the initial index level, the CDs may return more than the minimum 0.75%. The FDIC views the interest payment uncalculable prior to maturity and as a result the payment would not be covered should the bank go under.

The call option will have a positive value that is dependent on several factors including the volatility of the underlying indexes. The question is: is the value of the call option greater than the value of the bond discount?

One important variable in determining that value is the very long term of this product (seven years). The long term erodes the value of the components dramatically. Also, the fact that you cannot buy and sell these products in the open market suggests that their true value may be even less, a phenomenon referred to as an illiquidity discount.

These factors would be difficult for most retail investors to appreciate, let alone precisely value. Banks, however, have sophisticated models that can value these components quickly and easily. It should be clear that structured CDs are nowhere near as simple and assured an investment as traditional CDs, just as structured products are nowhere near as simple and assured as corporate debt.