Apple's Declining Stock Price and Structured Products

Jan 2013

Jason Zweig at the Wall Street Journal has an excellent piece on a part of the Apple story that hasn't gotten much press: many equity-linked structured products are linked to the common stock of Apple.

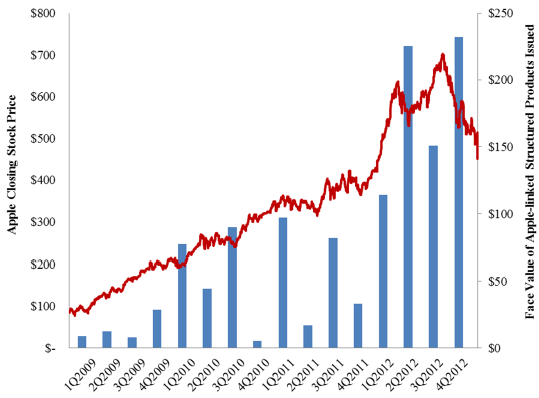

SLCG has recently completed an analysis of the market value of outstanding structured products linked to Apple common stock (AAPL). In the following figure, we plot the total quarterly issuance of AAPL-linked structured products in our database since the first quarter of 2009.

As Apple's common stock continued to increase in price, the total issuance of AAPL-linked structured products increased. The price of AAPL has been on a steady decline since late September 2012 -- when the stock briefly traded above $700 -- with the stock currently trading in the mid $400's. Following Tuesday's conference call in which Apple provided details surrounding their operations for the quarter ending December 29, 2012 (SEC Form 8-K), the price of AAPL common stock fell more than 12% -- a loss of more than $50 billion in market capitalization.

We have conducted an analysis of approximately 450 equity-linked structured products linked to AAPL in 2012 to determine what effect this decline had on the market value of these derivative products. In particular, we have studied three types of structured products: reverse convertibles (example), single observation reverse convertibles (example) and autocallable reverse convertibles (example).

Each of these products can be thought of as a bond issued by the investment bank paying fixed coupons in combination with a short put option. In the case of a reverse convertible, this put option is actually a down-and-in barrier option. In the case of an autocallable reverse convertible, the underlying bond is callable. From our report:

Reverse convertibles tend to pay higher coupon rates than traditional notes because, in addition to the issuer's credit risk, the notes expose investors to the risk of a decline in the price of the reference security.

For the 294 products that are outstanding as of January 24, 2013, we determined the fair value on Tuesday (before Apple's earnings announcement) and on Wednesday (after Apple's earnings announcement). We found that the value of these notes, which were on average already worth substantially less than their face value, declined another 12% -- amounting to mark-to-market losses approaching $50 million based upon SLCG's fair value estimates.

For more detailed information concerning these losses, please see our working paper on this issue. SLCG has compiled a database of over 14,000 structured product research reports including full valuation and analysis of each product.