Jan 2013

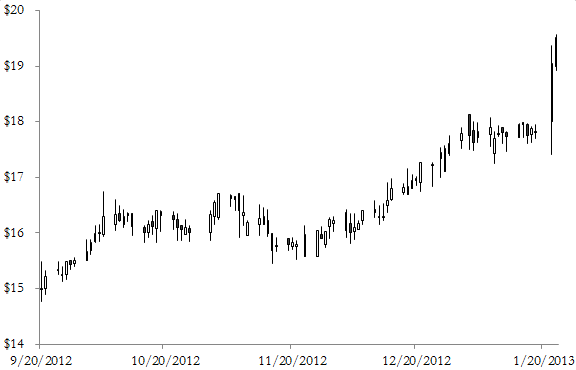

Based on Spirit Realty's closing price of $17.82 per share on January 18, 2013, the exchange ratio implies a value of $9.36 per CCPT II share and reflects a positive cumulative total return including dividends of 20-42% for shareholders of CCPT II, depending on the shareholder holding period. When compared to the volume weighted average price of Spirit's share price from the date of its inclusion in the Russell 2000 Index through the closing price on January 18, 2013, which was $17.66, the exchange ratio implies a value of $9.27 per CCPT II share. Based on the volume weighted average price of Spirit Realty over the last 20 trading days of $17.47 per share, the exchange ratio implies a value of $9.17 per CCPT II share. Following the close, CCPT II shareholders are expected to own approximately 56% and Spirit Realty shareholders approximately 44% of the common shares of the combined REIT.