The report categorizes HFT firms as 'aggressive', 'mixed' or 'passive' depending upon the proportion of their trades that are immediately filled. Firms are categorized as aggressive if trades are liquidity taking more than 40% of the time and passive if trades are liquidity taking less than 20% of the time. The firms that fall in the middle are deemed mixed.

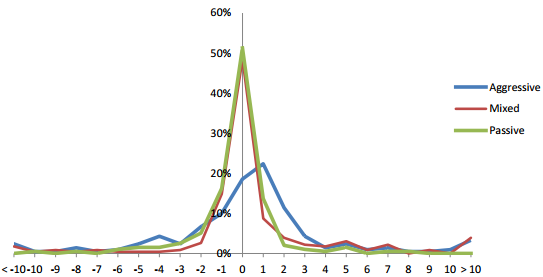

According to Table 8 in the report, high frequency traders realized an average daily short-term profit of $1.9 million in one particular market (S&P 500 E-mini futures contracts) in August 2010. On the other hand, retail investors realized an average daily short-termlossof about $123,000. The report finds that profits were concentrated in aggressive HFTs which "reveals deviations from market efficiency at very short intervals." The following figure depicts the profit per contract realized by each type of HFT trading strategy during the period analyzed.

Given that HFT firms are highly profitable, the question becomes whether they benefit markets as a whole. One of the primary ways HFT firms justify their activities is by arguing that they provide liquidity to markets. This study found that about 60% of HFT firms are net liquidity providers, but that the 'aggressive' HFT firms were liquidity takers on average. The authors note that "aggressive HFTs could be predatory and extract rents from slower or less informed traders, or they may provide value by correcting transient price deviations and thus leading to lower volatility and better price discovery."

They also note that "an arms race for ever-increasing speed and technological sophistication raises questions about whether the speed of information incorporation into the market at the millisecond time horizon has social value." It appears from their (admittedly limited) sample that not all HFT firms are the same, and that those identified as 'aggressive' may have less benefit than others.

These findings could provide guidance to regulators about how to most effectively regulate HFT firms to prevent abusive rent-taking while still encouraging productive liquidity. While its scope is limited, this study makes an important contribution to our understanding of these relatively secretive and unstudied firms who may have a disproportionate impact on financial markets.