The Wall Street Journal has an article about the rollercoaster ride that TVIX, a volatility-related ETN, has been on recently. [UPDATE 3/31/12: there is now a second WSJ article] TVIX is a leveraged ETN issued by VelocityShares, which is Credit Suisse's ETF/ETN brand. Contrary to popular belief, TVIX and other volatility products do not track the CBOE S&P 500 Volatility Index (the VIX); instead, TVIX tracks a daily rolling portfolio of first and second month VIX futures with an average maturity of one month, leveraged to 200%. Therefore, it is susceptible to both the contango effect which erodes VXX's value as well as the compounding effects which trouble leveraged ETFs.

The interesting thing about TVIX is that there's really only one reason to hold it: speculation on market sentiment. The reason most volatility derivatives were created was as a hedge for equities, since the VIX (and to a lesser extent VIX futures) are negatively correlated to the S&P, especially on particularly bad days--hence they're sometimes called 'catastrophe insurance'. TVIX, however, is highly volatile itself and exposed to both contango and leverage effects, so holding it beyond a single day could lead to significant deviation from expected performance. Bill Luby, one of the most respected voices on volatility derivatives, calls it "day trading rocket fuel." And so it is.

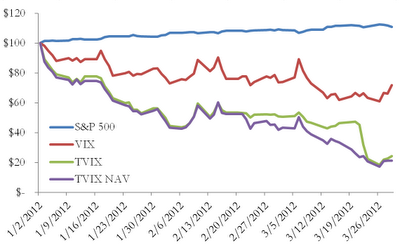

Even more interesting is that a little over a month ago TVIX exploded in popularity. For most of its life TVIX was well behind VXX in terms of assets and volume, but for reasons that aren't at all clear yet, TVIX all of a sudden took off and become more widely traded than VXX and started approaching it in terms of assets. Credit Suisse, for similarly unknown reasons, decided to stop creation of new shares on Feb 21, saying that the explosion in interest violated "internal limits on the size of the ETNs". After that, TVIX started trading at a huge premium to net asset value--even beyond 80%--as continued demand was not met by new share issuances. On March 22, they announced they would issue new shares again "on a limited basis", at which point the premium disappeared and the share price dropped about 50% in 48 hours, back to NAV.

Recent Performance of TVIX

TVIX investors have obviously been in for a wild ride. The WSJ article highlights one investor, who purchased TVIX as "a way to hedge if the market took a big drop and offset my losses in other securities." While many volatility derivatives claim to be effective for this type of hedging strategy (at least for very short periods of time), of all the available volatility products, TVIX is unlikely to be useful for this purpose. Indeed, TVIX is one of the most complex and unpredictable exchange-traded products a retail investor could buy.