The total asset value in Exchange-traded funds (ETFs) has increased dramatically in recent years. At the same time, ETFs have become more commonly associated with exotic features. One such ETF (a synthetic ETF), also known as a swap-based ETF, tracks the return of a selected index (e.g. the S&P 500 stock index) using a total return swap. The use of derivatives such as total return swaps distinguishes a synthetic ETF from the physical ETFs on the market. A complete list of synthetic ETFs offered on the Hong Kong stock exchange is available online.

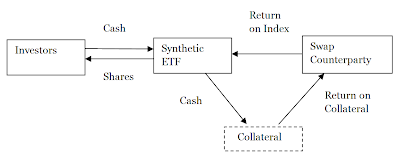

A physical ETF tracks an index in the most obvious way: owning the securities which constitute the index in the same portion as the index itself. The approach guarantees that the fund's return will track that of the selected index if the transaction costs and a few other inefficiencies are ignored. However, this strategy will not work in all cases. For example, imagine an ETF that is seeks to track the Russell 3000. Owning all of the stocks underlying Russell 3000 index could be prohibitively expensive due to the trading cost and market illiquidity for many small cap stocks. This is where synthetic ETFs come into the picture. If all the fund needs is to buy the return with a total return swap, few indexes are off limits. We present the following graphical representation of the synthetic ETF:

In the chart, a total return swap is a contract between the synthetic ETF and a counterparty. The counterparty pays the ETF the precise return of the selected index in exchange for the interest payment on the collateral portfolio. In an unfunded swap, as depicted above, investors' cash is used by the ETF provider to buy the basket of collateral. On the other hand, in a funded swap, investors' cash is paid to the swap counterparty and the collateral is pledged to the ETF's account held with a custodian. This means that the ETF does not legally own the collateral and when the counterparty defaults, the collateral might not be released to the ETF provider.

This brings us to the biggest potential downside of synthetic ETFs over physical ETFs: the heightened counterparty risk. When the swap counterparty defaults, the best investors could hope for is getting their share value back from the sale of the collateral. But this is unlikely for at least two reasons. First, the counterparty default usually happens in tumultuous market conditions. As a result, even decent quality assets may suffer a substantial haircut due to lack of liquidity. Second, the type and the quality of the collateral involved in a synthetic EFT are often opaque. For example, there is no requirement that collateral must be of the same type as the underlying index the ETF tracks. In other words, a synthetic ETF tracking the S&P 500 may well hold European sovereign bonds in its basket of collateral. This lack of transparency renders synthetic ETFs especially dangerous for retail investors.