In this blog post, we will discuss a particular kind of over-the-counter (OTC) derivative instrument called interest rate swaps. This post is meant as a broad stroke and an introduction to interest rate swaps. In the future, we plan to have additional posts about specialized interest rate swaps, case studies of particular interest rate swaps and on the pricing of interest rate swaps.

Interest rate swaps are customizable bilateral (involving two parties) agreements wherein one party exchanges a series of cash flows based upon one (possibly floating) interest rate for another (possibly floating) interest rate. The party that takes the opposite position in the agreement is referred to as the "counterparty". The interest payments each party is to receive are based upon the same principal amount - called the "notional". At each payment/settlement date, the interest payments are netted and only the party that has agreed to pay the higher interest payment makes a payment.

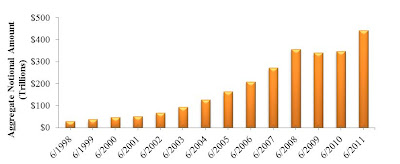

Interest rate swaps have become increasingly popular over the past several years. The aggregate notional amount of interest rate swaps within developed countries has grown from less than $50 trillion in June 1998 to more than $500 trillion in June 2011. The following figure was produced using data compiled by the Bank for International Settlements.

Total Notional Amount of interest rate swaps within G10 countries and Switzerland between June 1998 to June 2011.

Interest rate swaps can be used for a number of purposes. Institutions use swaps to ensure that income payments better match the required payments for their liabilities. Swaps can also be used as a hedge against rising interest rates. For example, if a municipality has floating rate debt and is concerned about the possibility of rising interest rates then an interest rate swap could transform this liability into a fixed-rate obligation. In addition, an interest rate swap can be used to change an entity's sensitivity to interest rate changes - called duration. The floating rate leg of the interest rate swap has shorter duration and therefore the value of the agreement to the floating-rate receiver is more sensitive to interest rate changes.

Interest rate swaps are usually structured so that neither side has an advantage at the beginning of the agreement - ignoring fees attached to the agreement by the financial intermediary structuring the agreement. This process involves projecting future cash flows for each party and then making sure the present value of the two party's cash flows are equal. As interest rates change over time, the agreement becomes an asset for one party and a liability to their counterparty.

There are significant risks associated with using these derivative products. For example, although swapping a floating rate for a fixed rate can change a floating-rate obligation to a (synthetic) fixed-rate obligation, the continued success of the agreement depends upon the counterparty's ability to hold up their end of the bargain. There is also the possibility that one party could terminate the agreement when the contract has a negative fair value for the counterparty. In this situation, it is possible that a large payment would be required to compensate the terminating party for the value of the agreement.

Interest rate swaps are powerful financial instruments that can be used for good or evil. It is important to consider fully the risks associated with the investment decision since these choices will have a profound fiscal impact for years to come.