Investors may think, when investing in Futures-Based Commodities exchange traded funds (ETFs), that they are gaining exposure to the underlying commodity. In this blog post, we discuss the ability of these ETFs to track the spot price of the underlying commodity.

In a previous blog post, we introduced the basics of Exchange Traded Funds (ETFs). In this post, we are going to discuss a specific kind of ETF: Commodities Futures Based ETFs.

There are a large number of Exchange Traded Funds (ETFs) on the market today that purport to offer investors exposure to a commodity, whether it is gold (e.g. GLD), crude oil (e.g. USO) or crops (e.g. DBA). There are many reasons an investor might want exposure to the price changes of a commodity. Equity investors can decrease the volatility of their portfolio by allocating a portion of their investments to commodities without decreasing expected returns. This is due to the negative correlation between equity returns and the returns of commodities futures contracts. Another reason is that the price of commodities is positively correlated with inflation. So an investor concerned about the buying power of their money might invest in commodities as a hedge against the inflationary deterioration of their money. ETFs make gaining exposure to commodities easier for retail investors when compared to conventional methods.

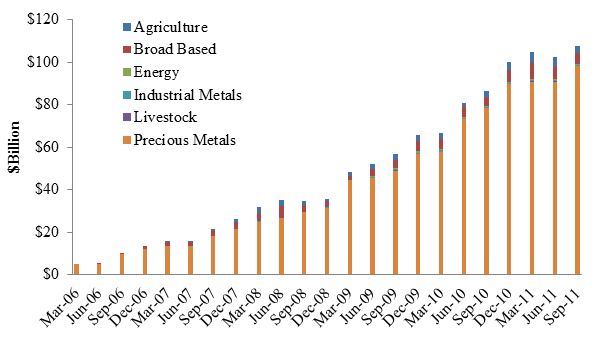

The first commodity ETF in the U.S. was State Street's SPDR Gold Trust ETF (GLD) issued on November 12, 2004. In the figure below, we show the total amount of funds invested in commodities ETFs from March of 2006 to September 2011.

Asset Value of Commodities ETFs

Commodities ETFs obtain exposure to those markets not through purchasing the physical assets (since the storage of most commodities is impractical) but through futures contracts, which involve complex "rolling" strategies. An investor that wants exposure to commodities in his or her portfolio will likely buy futures contracts, either directly or indirectly. Since all futures contracts have expiration dates, an investor will have to replace an expiring contract that he or she owns with a new contract that expires later, a process known as "rolling-over". Essentially if the contract you're replacing is sold for less than the contract you're buying, you are losing some of the return associated with change in the spot price of the underlying commodity.

As a result of these rolling strategies, these ETFs show substantial deviations from the returns investors might expect or intend when they purchase them. Retail investors might assume that those ETFs track the spot price of a commodity itself, such that when the price of oil (or silver, or wheat) rises or falls, the ETF's value will rise or fall a proportional amount. This potential for misunderstanding could lead to substantial losses, especially since most of these ETFs grossly underperform the spot prices of their underlying assets.

For more details about commodities ETFs and an analysis of the mechanism that leads to the departure from naive expectations for returns, see the following paper.