Inverse exchange traded funds (ETFs) are, by most measures, just as popular and liquid as their leveraged counterparts. In this post we discuss the rebalancing and tracking behavior of these ETFs.

This is the second part of our two part series. Last time we discussed leveraged Exchange Traded Funds (ETFs). In this post, we are going to discuss a related kind of ETF: Inverse ETFs.

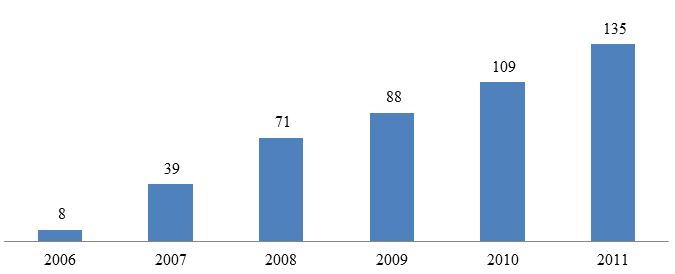

An Inverse ETF offers investors a daily return that is opposite of the daily return of the index or asset tracked by the ETF. For example, an inverse ETF that tracks the S&P 500 index (SPX) would return the inverse of the daily return of the SPX. So if SPX exhibited a return (loss) of 10%, then an investor in the fund would see a loss (return) of 10%. Since their introduction in 2006, the number of inverse ETFs has grown quickly over the past five years.

Number of (US Domiciled) Inverse ETFs from 2006 to 2011

Just as with leveraged ETFs, investors interested in inverse ETFs need to be aware of is the effect of rebalancing. Following the previous post in the series, we will explain rebalancing by example. Let's say an investor has $100 cash and shorts $100 of some asset (giving her $200 cash and a -$100 position in the asset). If the asset increases in price by 10%, the investor now has $90 net equity. In order for our investor keep her inverse exposure to the asset for the following day; she must rebalance her account so that the total amount invested is equal to the short position in the asset. To keep her inverse exposure, she must take $20 of her cash to buy a share of the underlying asset. The resulting position is $90 net equity with a -$90 position in the asset.

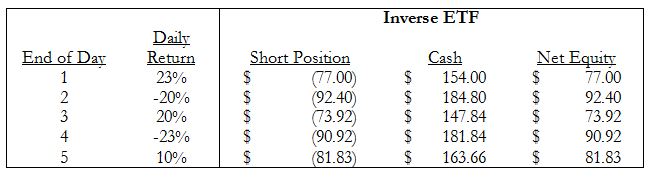

Inverse ETFs must rebalance on a daily basis since at any time an investor could buy the fund and at that point the ETF needs to be of the appropriate leverage. The effects of rebalancing on buy-and-hold investors compound over time and lead to substantial deviations from expectations. We present the following table as an example of the compounding effect of rebalancing.

Hypothetical Scenario to Illustrate Effect of Rebalancing

Notice that the underlying asset has (basically) not changed at all in price; however, the net equity value in the inverse ETF experienced a 18% decrease. The take-away message from this is that buy-and-hold investors should not invest in inverse ETFs unless they understand the risks associated with daily rebalancing.

Although we have only discussed in detail -1x (Inverse) ETFs here, there are also many inverse leveraged ETFs on the market that offer investors multiples of the inverse daily returns of an underlying index or asset.

Proshares discusses the rebalancing issue in some detail here and here. For further reading on this topic, we suggest taking a look at our paper on the effect of rebalancing on investors in ETFs.