Earlier this week we posted about the $122 billion in autocallable structured products sold in the past 4 years, mostly issued by UBS, Goldman Sachs, JP Morgan, Citigroup and Morgan Stanley. You can read that post here.

We illustrated features of autocallables with reference to the five notes linked to the stock price of Lucid issued by Credit Suisse and Citigroup in a post available here and pointed out a particularly poorly timed issuance by Citigroup linked to Silicon Valley Bank stock in a post available here.

In this post, we explain how some issuers overstate a key disclosure required by the Securities and Exchange Commission to be prominently displayed in the 424b filing for every structured product. Some issuers (Goldman Sachs and Morgan Stanley for examples) appear to adhere to the word and spirit of the SEC's guidance by using yields on their straight debt to estimate the Day-1 value of structured notes. Other issuers (Citigroup, Toronto Dominion and HSBC for examples) use internal funding rates but disclose qualitatively at least that if they had used secondary market yields their estimated Day-1 values would be lower.

On the other hand, UBS, Credit Suisse and Bank of Montreal appear to flout SEC guidance and instead provide meaningless Day - 1 values based on arbitrarily low discount rates and without any discussion of the impact of using these lower discount rates on the estimated values they place on 424bs.

UBS, Credit Suisse and Bank of Montreal issued $43.1 billion of autocallable structured notes, and billions more in other types of structured notes with inadequate disclosures. Moreover, investors in Credit Suisse's autocallables which physically settle have lost at least $100 million.

Introduction

Since 2013, the SEC has required issuers to include an estimated value of structured products in the pricing supplement describing the terms of the security being offered. At the time, the SEC provided guidance to issuers in a February 21, 2013 letter from the Division of Corporation Finance. See for example, the Corp Fin letter sent to UBS available here.

The SEC's intent to provide investors with the "market value" as well as the "purchase price" of the notes seems clear and is certainly laudable. Unfortunately, some issuers have taken extraordinary liberties in their calculations of Day-1 value such that, at best, the values reported in the 424bs should be viewed as an upper bound on the true value of the note.

The option components have to be valued by reference to observable option prices (and implied volatilities and correlations). The bond component on the other hand can be valued using yields on the issuers' straight debt which would including compensation for credit and liquidity risk. Using these "credit spreads" would result in a true FMV to the extent the structured notes are as liquid as the issuer's debt trading in secondary markets.

The SEC also allows the issuers to value the bond component using its internal funding rate. Some issuers appear to interpret "internal funding rate" to mean whatever the issuer wants to pay on the notes being issued, not at the rate the issuer allocates capital internally or the rate at which it values the outstanding notes as a liability in its accounting.

To get a rough idea of the range of discretion: Suppose Citigroup has 2-year bonds trading a yield to maturity of 5%. This 5% includes Citigroup' yield spread and would be a sensible discount rate to apply to the structured note to estimate a FMV ignoring the difference in liquidity between Citigroup's traded debt and the nontraded structured note. Suppose, given a note's parameters and the 5% discount rate derived from the yield on Citigroup's traded 2-year bonds, the estimated value of the newly issued note is $930.

If instead, Citigroup instead discounts at 4% because that is the 2-year Treasury yield (also Citigroup's yield less its yield spread) the estimated value will be about 2% higher or $948.

Some issuers seem to discount the structured notes future payments at whatever rate the issuer wants to pay to investors on the notes given it may have other costs which it is not supposed to include in the note's valuation. Continuing with our example, suppose the issuer structures the note to pay investors only 2.5% so that the issuer can incur additional selling commissions, hedging costs and legal fees entailed in issuing the structured product and still pay less all-in that if the issuer had issued straight debt. Now, a very aggressive interpretation of the SEC's 2013 guidance would allow the issuer to value the notes using a 2.5% discount rate and our example note would be valued at $976.

All of which is to say, the Day-1 values posted on 424bs sometimes look like our $930, $948 or $976 examples and so are an upper bound on the FMV. In our example, the FMV is $930.

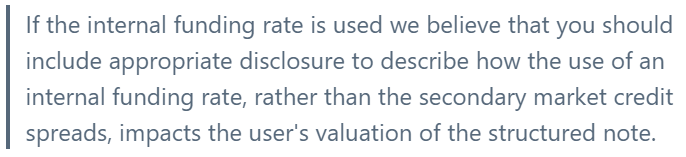

Moreover, the SEC told issuers to inform investors of the impact of using something other than the yield on the issuers' traded debt or other similar debt. As we demonstrate below, when issuers use internal funding rates rather than discount rates which include credit spreads, they use nonsensical language which fails to address the SEC's disclosure requirements.

The issuers offering a Day-1 value based on any discount rate substantially less than the yield on their traded debt, could and should report the value using discount rates which include their credit spreads so investors can see the impact of using the lower internal funding rates.

Goldman Sachs $60,000,000 Autocallable Nasdaq-100 Index(R)-Linked Notes due 2026

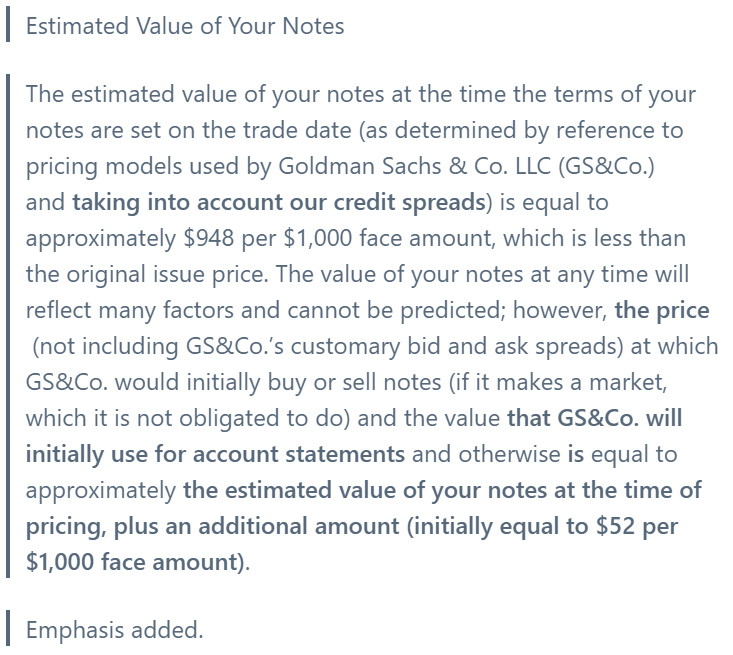

Goldman Sachs appears to meet the spirit of the SEC's disclosure rule in all the 424bs we recently reviewed. For example, its September 29, 2022 424b reads in part:[1]

Thus, Goldman Sachs is using the yield on its debt to value the notes at $948. It also discloses that the first few months it will add enough to the value of the notes when reporting a value of the notes on account statements so that investors won't notice a loss due to the difference between the $1,000 purchase cost and the $948 fair market value.

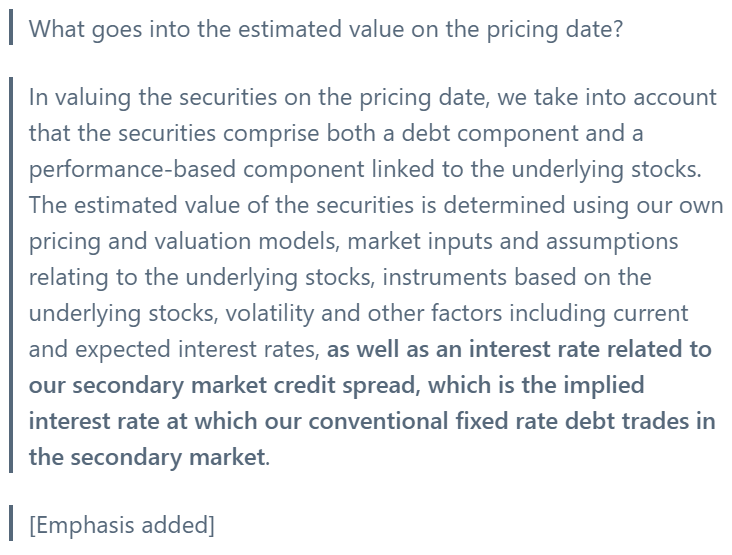

Morgan Stanley's Contingent Income Auto-Callable Securities due August 15, 2024

Like Goldman Sachs, Morgan Stanley uses a discount rate which incorporates its credit spread when valuing these notes at $933. The 424b for this note at page 3 reads:[2]

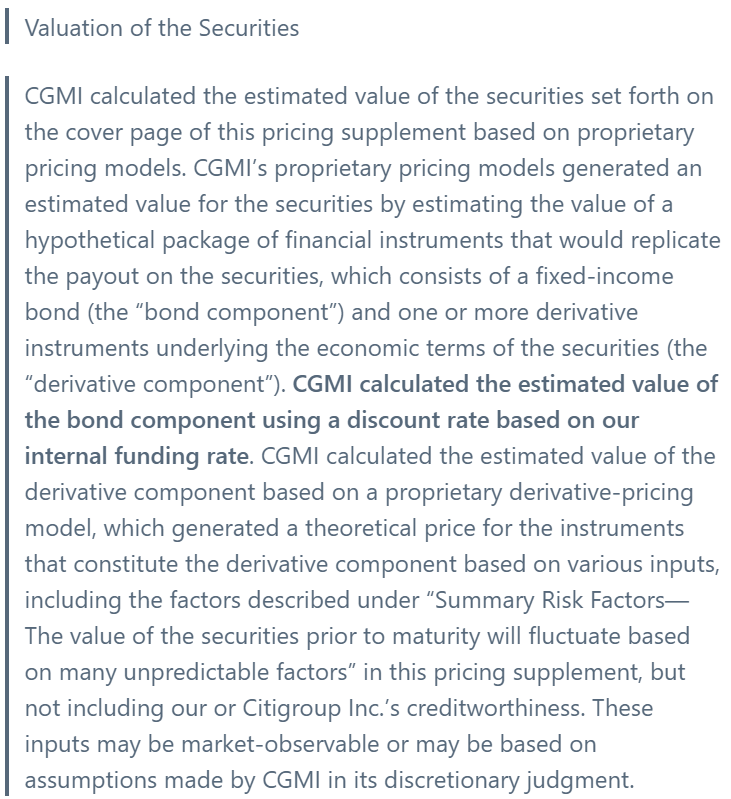

Citigroup's Autocallable Barrier Securities Linked to the S&P 500(R) Index Due July 1, 2027

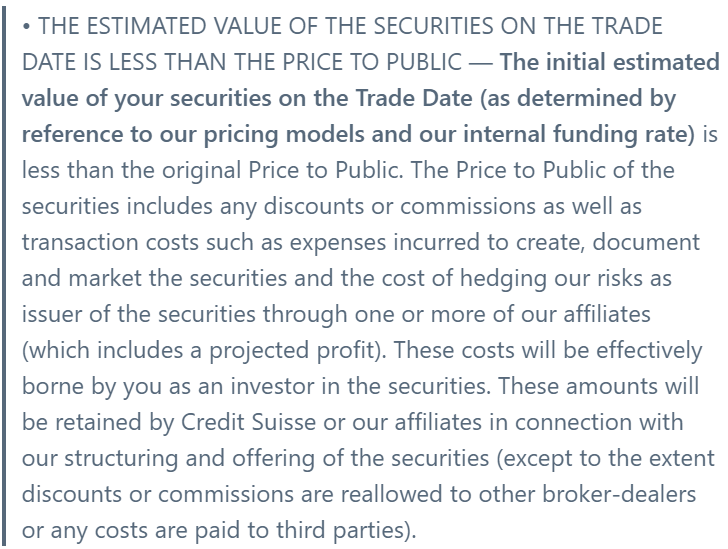

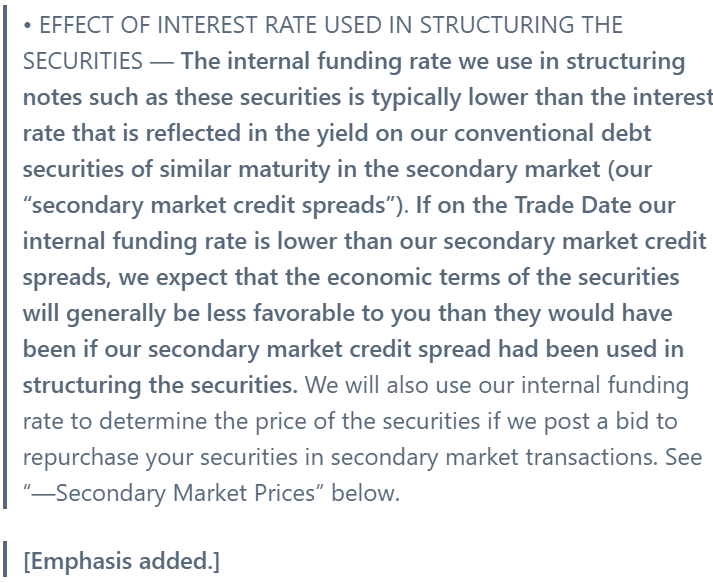

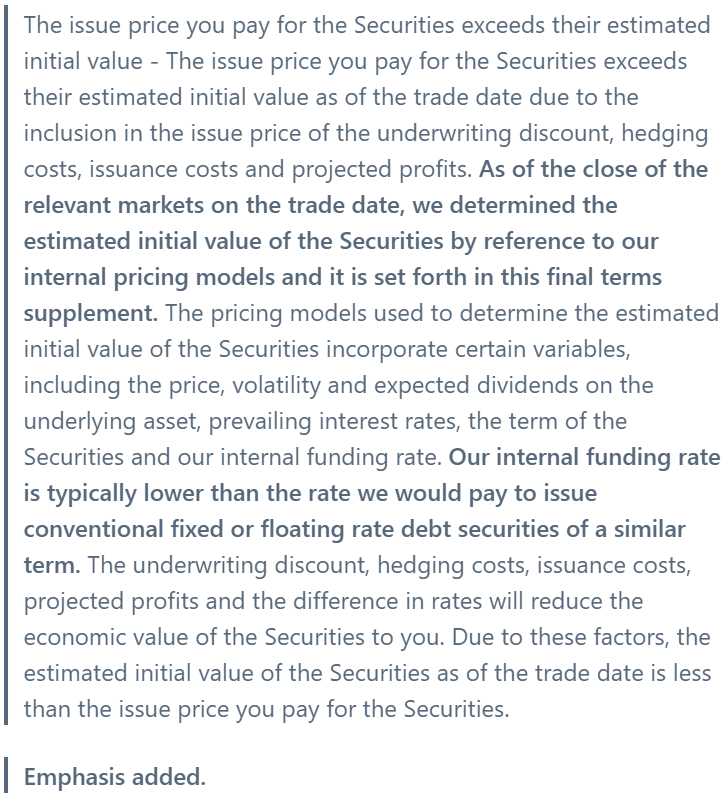

While Goldman Sachs and Morgan Stanley meet the spirit of the SEC's guidance, Citigroup does not. It uses an internal funding rate rather than the yield on its traded debt when valuing this note at $964.20. This is implausibly high since the net proceeds to Citigroup is only $970. Citigroup's 424b reads at PS-9.[3]

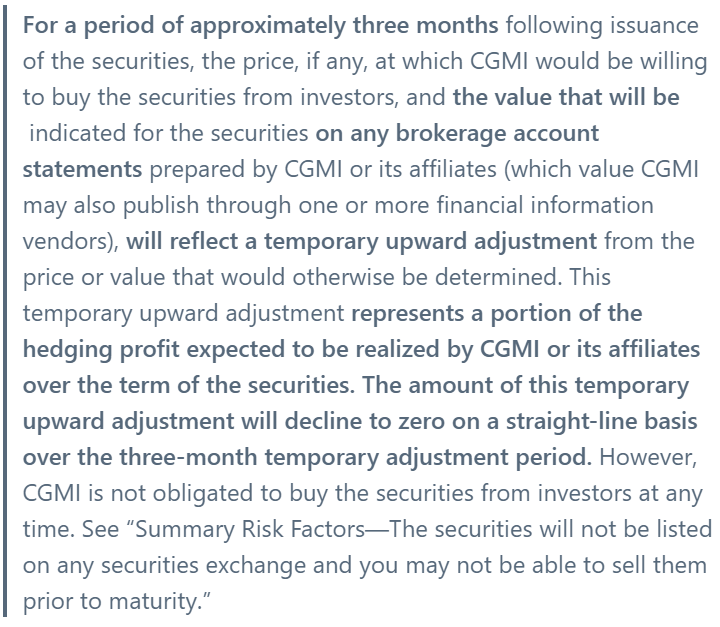

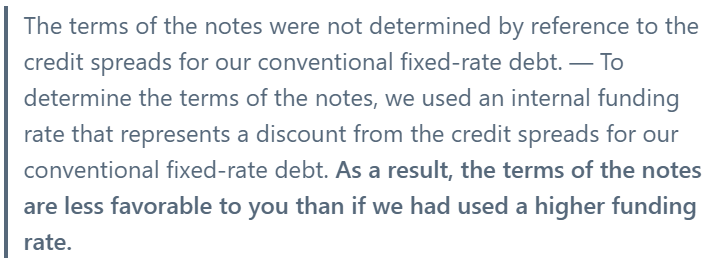

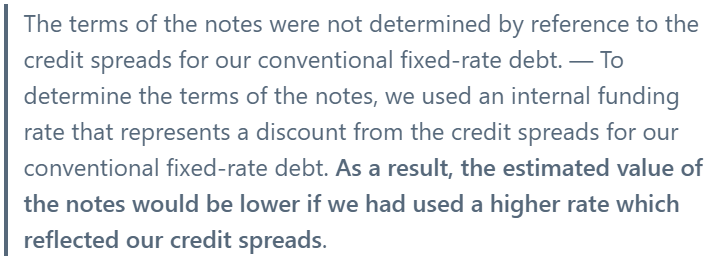

The same 424b at page PS-6 at least offers a qualitatively correct statement about the impact of using an internal funding rate which is lower than market yields to value the structured note.

The SEC instructed issuers to make substantially this Citigroup disclosure in the event the issuer uses an internal funding rate which does not incorporate credit spreads. Page 2 of the SEC's 2013 instructions to issuers including the following instruction.

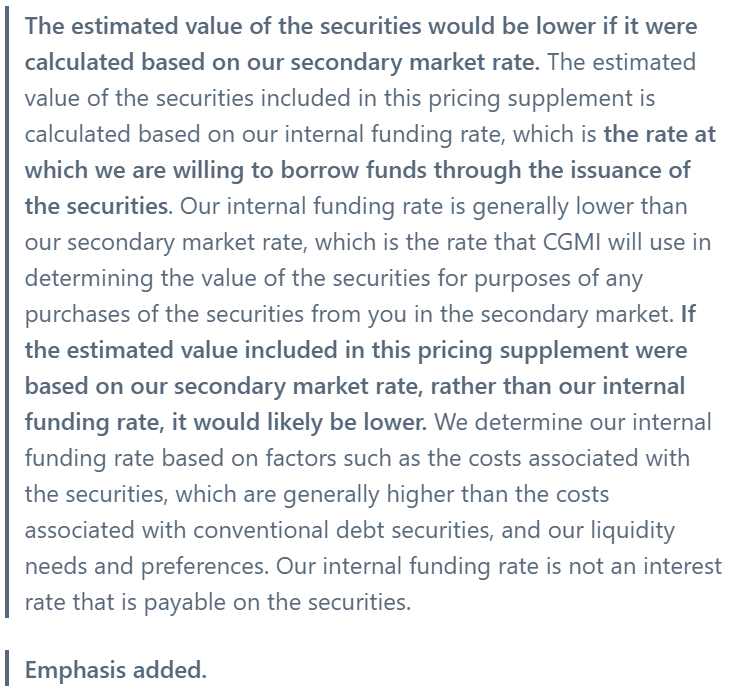

Credit Suisse's $1,142,000 Contingent Coupon Autocallable Yield Notes with Upper Threshold Feature due November 7, 2024 Linked to the Performance of Four Underlyings

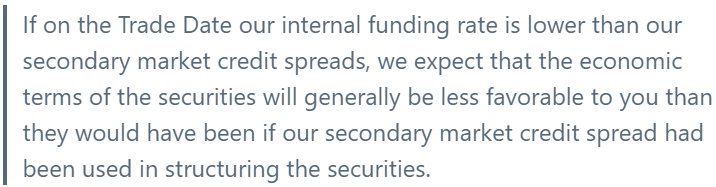

Like Citigroup, Credit Suisse discloses it uses its internal funding rate to value newly issued structured products. Credit Suisse's 424b for this autocallable, it valued at $959, includes at page 14:[4]

Remarkably, Citigroup's and Credit Suisse's statements could allow for the use of an arbitrarily low discount rate. The worse Citigroup and Credit Suisse structure the note from the investor's perspective, the lower the expected yield the note's structure implies. The lower the expected yield, the lower the discount rate the issuer feels justified in using and the higher their reported Day-1 value. That is, under Credit Suisse' apparent interpretation of the SEC's guidance it could report a $959 value whether the true FMV was $959, $929 or even $899 because the lower the true FMV, the lower the yield will pay investors over the life of the note.

At least Citigroup was clear that using a market yield which reflected its credit spreads would lower the estimated Day-1 value compared to the value reported on the first page of the 424b.

Credit Suisse's language isn't even close to what the SEC requires. The SEC told issuers to tell investors what the impact on the Day - 1 values would be of using market yields instead of internal funding rates. Instead of providing Citigroup's qualitatively correct disclosure, preferably quantified, Credit Suisse offered this meaningless word salad.

UBS AG $301,000.00 Securities Linked to the common stock of D.R. Horton, Inc. due on December 27, 2024[5]

UBS's standard language is similar to Credit Suisse's language and does not state that using its secondary market yields instead of its internal funding rates to value the notes would result in a lower Day-1 value.

Autocallable Barrier Notes with Contingent Coupons due March 28, 2024 Linked to the Least Performing of the shares of VanEck Vectors(R) Gold Miners ETF and the shares of VanEck Vectors(R) Junior Gold Miners ETF[6]

Bank of Montreal at page 8 of the 424b uses language similar to Credit Suisse's language.

Better disclosure would read something like:

Of course, issuers should value structured products using the yields on their straight debt. Using an internal funding rate, especially a rate that can be whatever the issue structures the note to pay investors, allows for extraordinary mischief.

Issuers can and do lower the discount rate to whatever they want and call it an internal funding rate. By lowering the discount rate arbitrarily, issuers like UBS, Credit Suisse and Bank of Montreal can push Day-1 values arbitrarily close to the "proceeds to issuer" amount and thereby include in the Day-1 values costs and profits the SEC explicitly told them not to include in Day-1 values.

This mischief could be somewhat offset if UBS, Credit Suisse and Bank of Montreal told investors the Day-1 value is not a fair market value based on its secondary market yields as does Citigroup, Toronto Dominion and HSBC.