You can download a PDF of this article to print or email here

Introduction

We recently posted research into stock issuances solely underwritten by Aegis Capital. We concluded that investors, including many Aegis' retail customers, suffered $3.0 billion to $5 billion in losses in

recent years as a result of Aegis' conduct. You can view that post here.

We also concluded that in at least three instances either Aegis marked the close or looked the other way while others marked the close to facilitate an underwriting. We described one of these examples,

Meten. In this note, we describe facts leading us to conclude that someone marked the close in SeaChange International. We also illustrate how an issuer and underwriter might game the dilution disclosure

when the issuer is burning through resources at a rapid pace, as was true of virtually all the Aegis underwritten issuers we reviewed.

SeaChange International

SeaChange issued 10,323,484 shares at $1.85 for total gross proceeds of $19,098,445 on March 30, 2021. You can see the 424(b)(5)

here.

Aegis received $1,241,399 plus reimbursed expenses. As of February 28, 2024, the value of these shares has dropped 95.5%.

The first page of the 424(b)(5) reads in part:

SeaChange's closing stock price declined 72.3% from $3.72 on March 31, 2020 to $1.03 on March 26, 2021, before spiking to close at $2.08 on March 29, 2021 and then continuing

its decline to $0.08 on a split-adjusted basis on February 28, 2024.[1] See Figure 1.

The fleeting spike in SeaChange's closing price to $2.08 the day before the offering occurred with no material news but on extraordinary volume.[2] Trading in SeaChange on March 29, 2021 drove the price up throughout the day to close at $2.08. The issuer and the underwriter benefited from this activity as it allowed the issue size to be larger. If SeaChange had closed above $2.40, the issue size would not have been limited at all but the effort to push the closing price higher appears to have run out of juice.

Figure 1 SeaChange Daily Closing Stock Price, March 31, 2020 to March 18, 2024

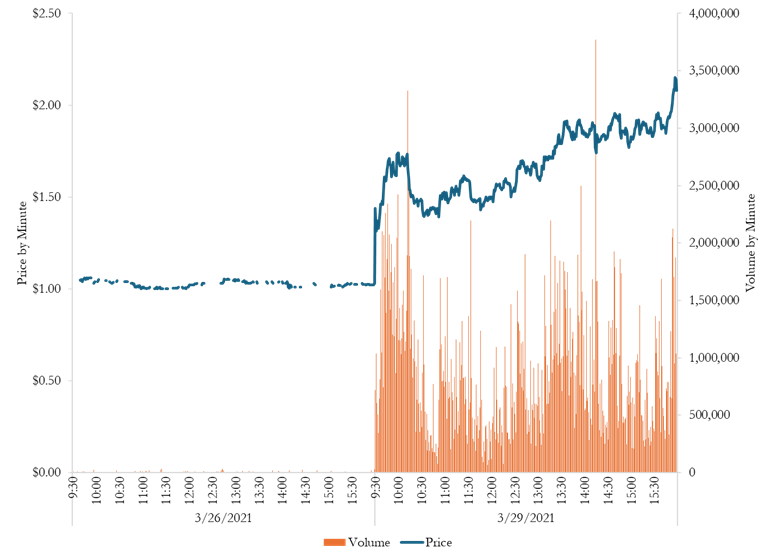

The trading volume on March 29, 2021 was 440 times the trading volume on March 26, 2021 and 12 times the float. In fact, the average trading volume per minute on March 29, 2021 was roughly equal to the trading volume for the entire day on March 26, 2021. See Figure 2.

Figure 2 SeaChange Intraday Price and Volume, March 26, 2021 and March 29, 2021

Dilution Games

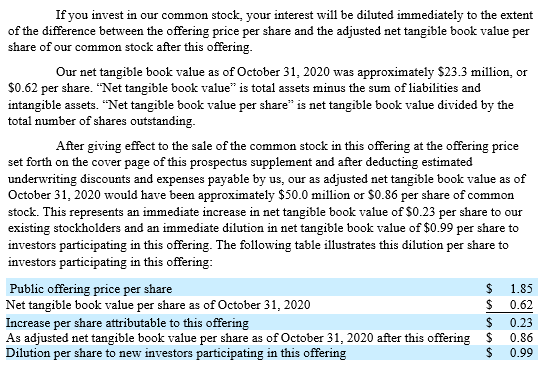

As with the other Aegis Capital underwritings we reviewed, investors who were paying $1.85 per share were being substantially diluted. SeaChange used its reported net tangible book value per share as of October 30, 2020 in the March 30, 2021 424(b), which read in part:

DILUTION

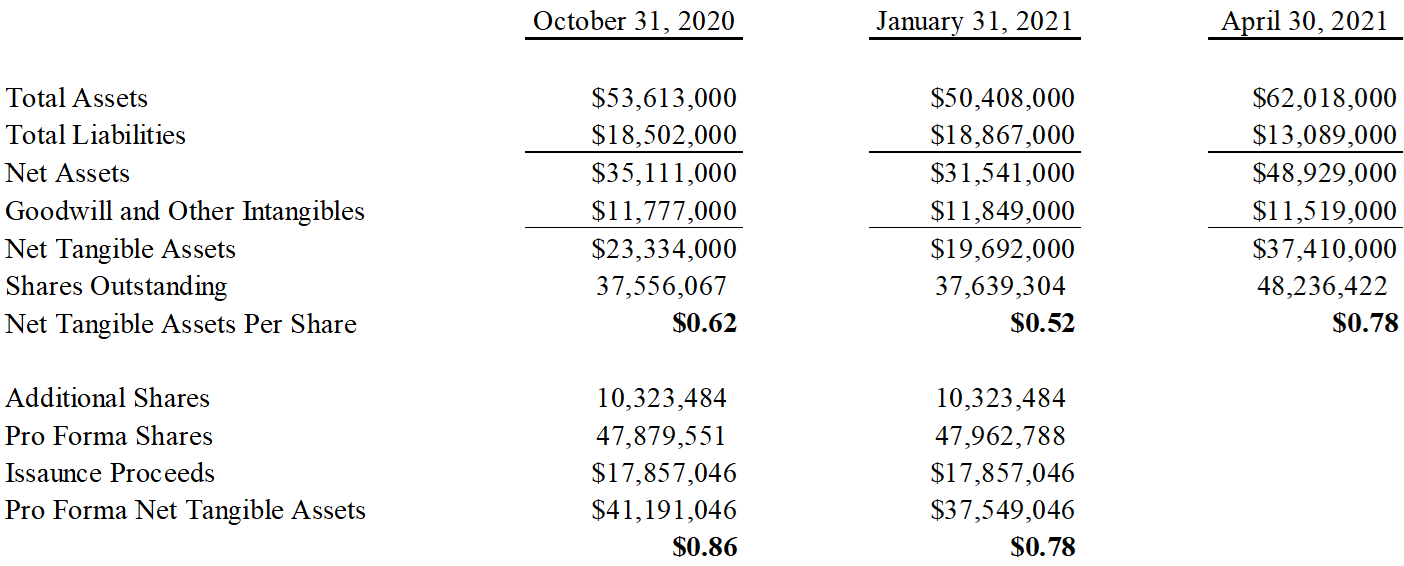

I recreate the dilution calculation using information from SeaChange's October 31, 2020 10-Q in Table 1.[3] Tangible Net Assets Per Share would increase from $0.62 to $0.86 as a result of the March 30, 2020 issuance occurring on October 30, 2020. By this calculation, investors paying Aegis $1.85 were suffering immediate dilution of $0.99. This calculation is troublingly misleading because the issuance did not occur on October 30, 2020 and more current information reflecting further deterioration at SeaChange and therefore greater dilution of new investors.

Table 1 Recalculation of Investor Dilution in the March 30, 2021 SeaChange /Aegis Issuance

SeaChange's 10-K for the period ended January 31, 2021was not filed by March 30, 2021.[4] If January 31, 2021 had marked a fiscal quarter-end rather than year-end, this information would have been published by March 15, 2021. The high-level information on total assets, total liabilities, goodwill and intangible assets and shares outstanding as of January 31, 2021 should have been knowable to SeaChange and Aegis Capital on March 30, 2021.

I recalculate the dilution suffered by Aegis's clients in this offering using balance sheet information for January 31, 2021 - two months, not five months before the offering. Net Tangible Assets Per Share had declined from $0.62 on October 31, 2021 to $0.52 on January 31, 2021. Therefore, Tangible Net Assets Per Share would increase from $0.52 to $0.78 as a result of the March 30, 2020 issuance occurring on January 31, 2021. By this much-closer-in-time calculation, investors paying Aegis $1.85 for these shares were suffering immediate dilution of $1.07, not $0.99. As a check, I calculate the Net Tangible Assets Per Share on April 30, 2021 - one month after the issuance was in fact $0.78 and so the dilution was $1.07.

Conclusion

Whoever marked the close in SeaChange on March 29, 2021, SeaChange and Aegis benefited as the stock price jumped more than 100% in a day on 440 times the previous day's trading volume and no material news.

The reported dilution we find in many offerings substantially understate the actual dilution investors suffer in these issuances because the issuer and underwriter use stale financial information on a business that is burning through resources.