Aug 2023

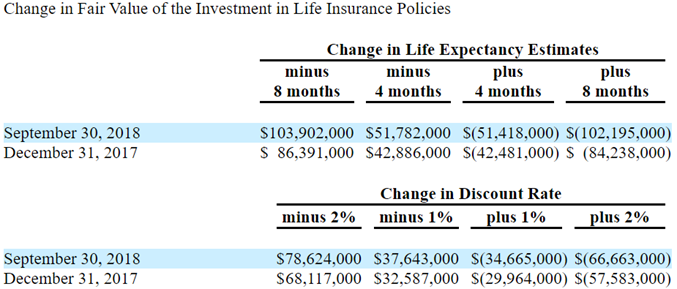

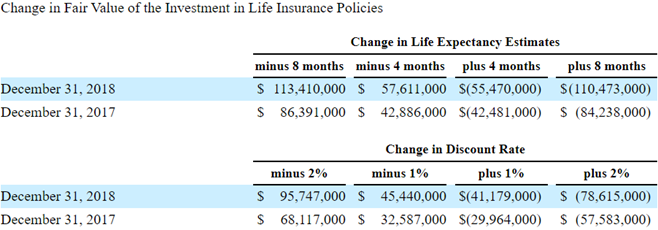

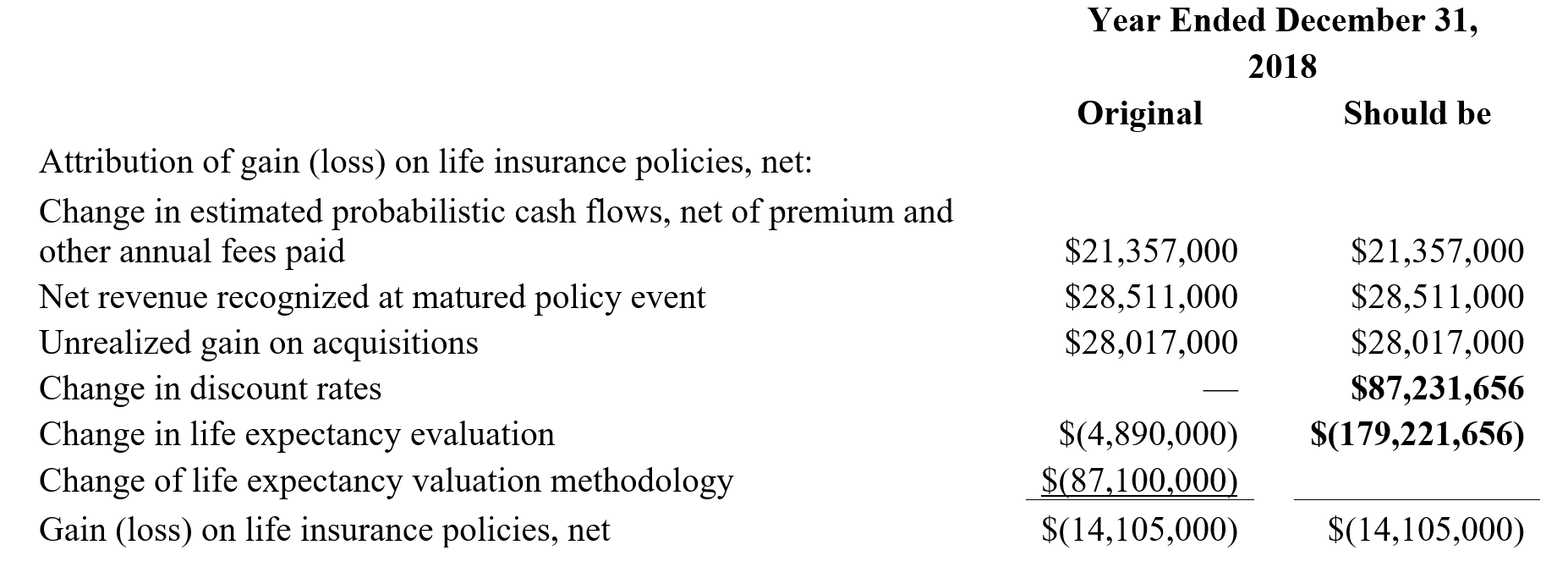

The implementation of the Longest Life Expectancy methodology required us to take a non-cash charge (net of the impact of a change in discount rate) to revenue of $87.1 million, reflecting a decrease in the fair value of its portfolio of life insurance policies at December 31, 2018. This non-cash charge represents approximately 10% of fair market value of the portfolio prior to adjustment.

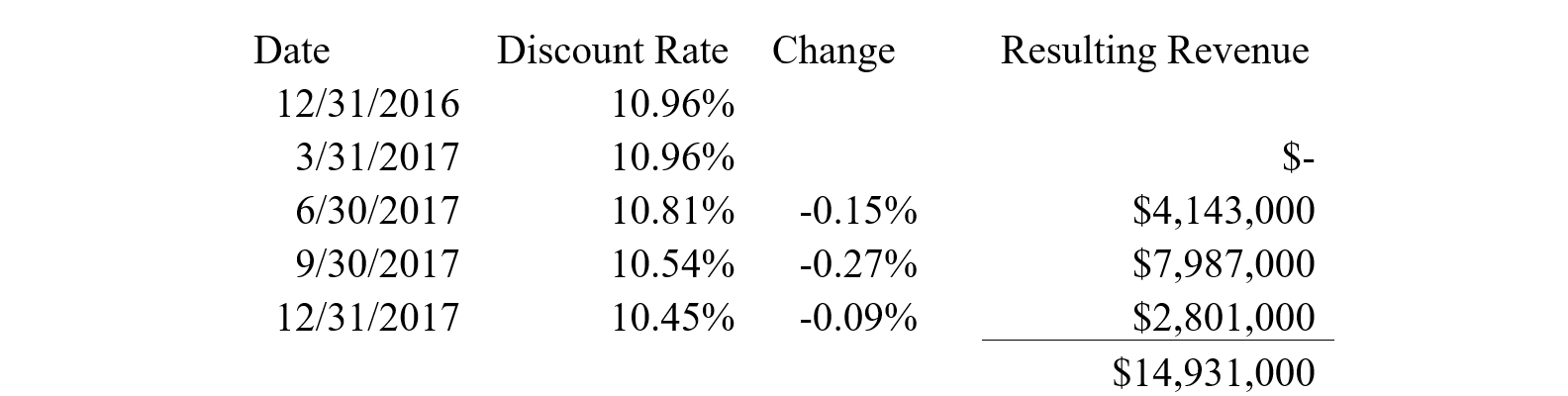

The discount rate we apply incorporates current information about discount rate applied by other reporting companies owning portfolios of life insurance policies, the discount rates observed in the life insurance secondary market, market interest rates, the credit exposure to the insurance companies that issued the life insurance policies and management's estimate of the risk premium a purchaser would require to receive the future cash flows derived from our portfolio as a whole.[5]