We have found so many red flags in GWG Holdings' public filings years before its bankruptcy filing in 2022 that no unconflicted broker would have recommended GWG's L Bonds and no fully informed investor would have bought them. Nonetheless, $1.3 billion face value of L Bonds remained outstanding at the time of the bankruptcy. These bonds were sold by third tier brokerage firms in pursuit of undisclosed commissions as high as 8%.

We will tell a more complete story about GWG in the coming months, but recent events related to GWG Holdings' primary potential asset in bankruptcy - Beneficient common stock - warrant a short post today.

You can download this post to print or email here.

GWG Bondholders' Near Worthless Beneficient Common Stock

GWG bondholders have $1.6 billion in claims in bankruptcy - the outstanding face amount of L bonds and accrued interest as of the bankruptcy filing in April 2022.

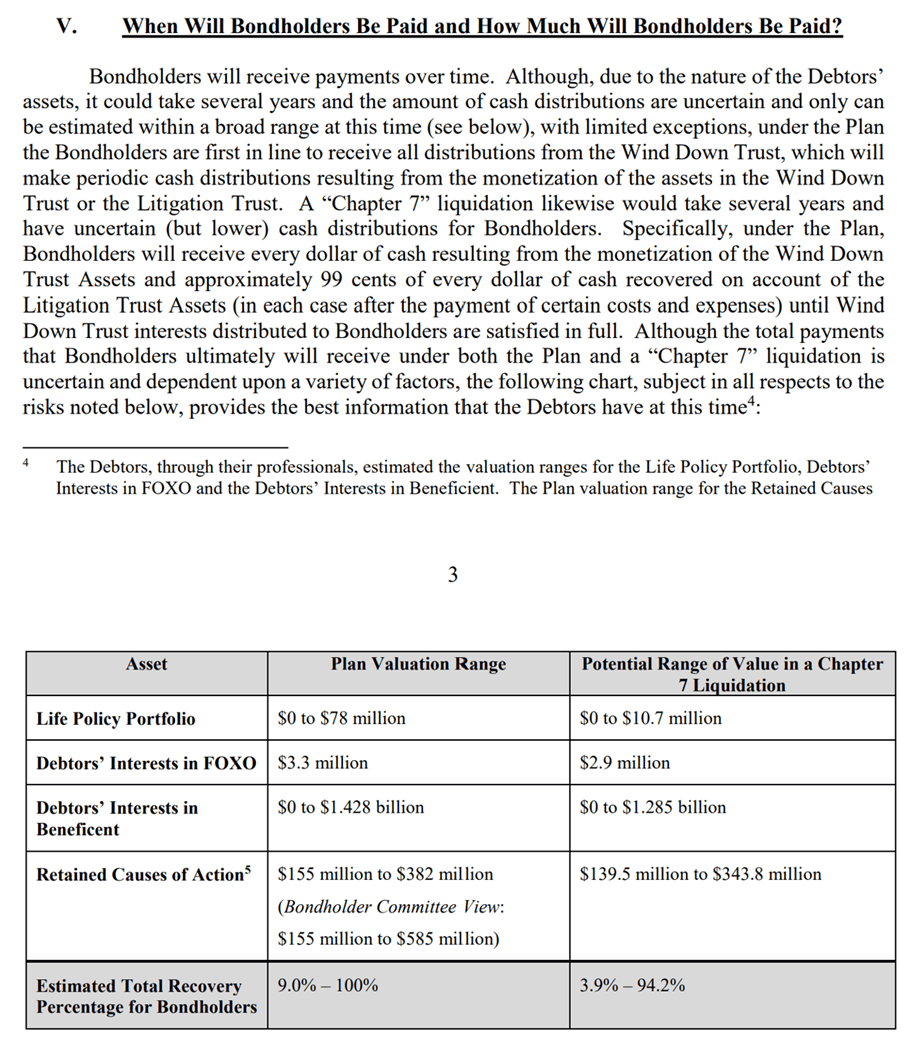

There are four possible sources of recovery.

GWG's legacy life insurance portfolio is collateral for secured lenders. As insurance policies are sold or serviced and pay out death benefits the secured lenders will be paid off. Excess value in the insurance contracts, if any, after the secured lenders are paid off will be paid into the bondholders' trust. The Plan estimates this residual interest in the insurance contracts to be between $0 and $78 million. Any amounts resulting from this residual interest likely to be received well off in the future.

GWG FOXO assets are estimated to be worth $3.3 million.

GWG bondholders have a stake in litigation which may be worth $155 million to $382 million.

Finally, GWG bondholders own at least 142.8 million shares of Beneficient stock (BENF). If BENF could be sold for $10 per share the bondholders' trust would receive $1.428 billion and the bondholders' recovery would be close to 100% after considering results from other sources of recovery. On the other hand, if BENF is nearly worthless as seems likely to us, bondholders will likely recover less than 10% of their claims.

Table 1. Bondholder Potential Recoveries Mostly From BENF

Source: Summary of Treatment of Bondholders under the Debtors' Second Amended Joint Chapter 11 Plan, filed April 24, 2023 and available here, at page 3-4.

GWG's Form 3 filed with the SEC on June 7, 2023 available here, reports the bondholders' trust owns 125,710,725 shares of BENF common stock and a $205.2 million Preferred C-1 Unit account. The preferred units will be converted into common stock based on the lower of (i) the volume-weighted average trading price of BENF for the 20 trading days following June 7, 2023 and (ii) $10.20.

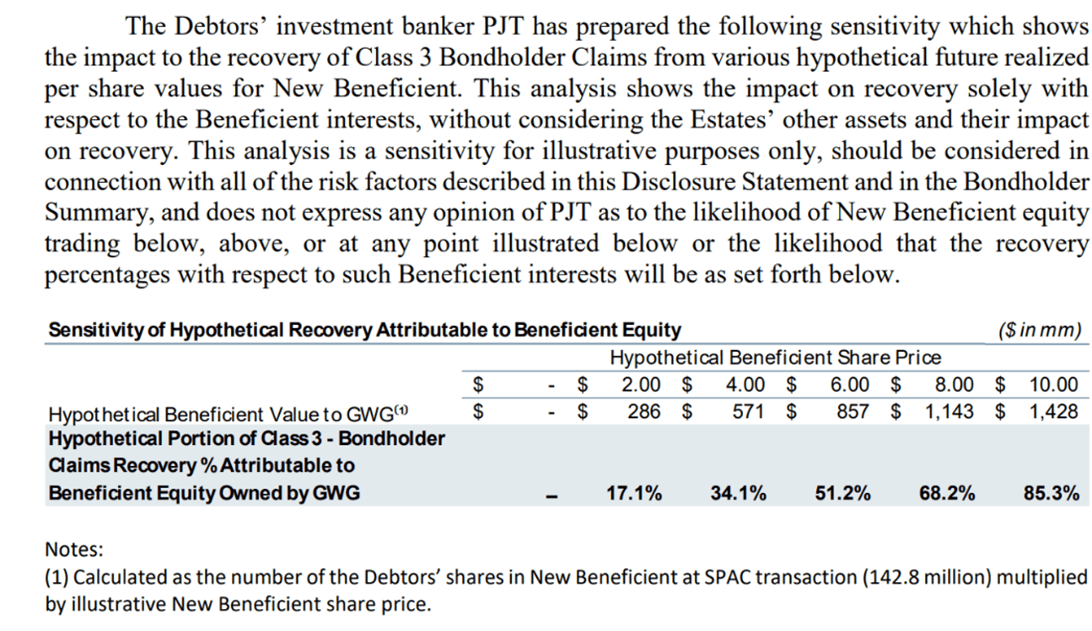

The sensitivity to L bondholder recoveries is further detailed in the Disclosure Statement. Assuming the bondholders own 142.8 million shares of BENF, the trust will receive $1.428 billion if the stock can be sold for $10 but only $286 million if the stock can be sold for only $2.

Table 2. Bondholder Recoveries are Highly Sensitive to Value of BENF

Source: Disclosure Statement for the Debtors' Further Modified Second Amended Joint Chapter 11 Pla, Submitted by the Debtors, the Bondholder Committee, and L Bond Management, LLC as Co-Proponents, filed April 24, 2023 and available here, at page 10.

As we show next, the price at which the preferred stock converts is likely to be less than $7 so the trust will end up owning more than 155 million shares of BENF.

GWG Bondholders are Unlikely to Realize Much From Their BENF Holdings

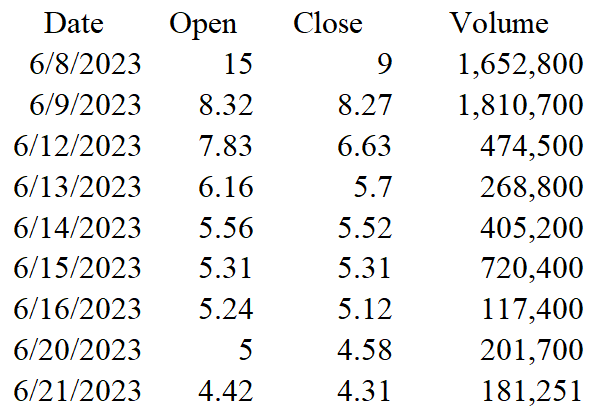

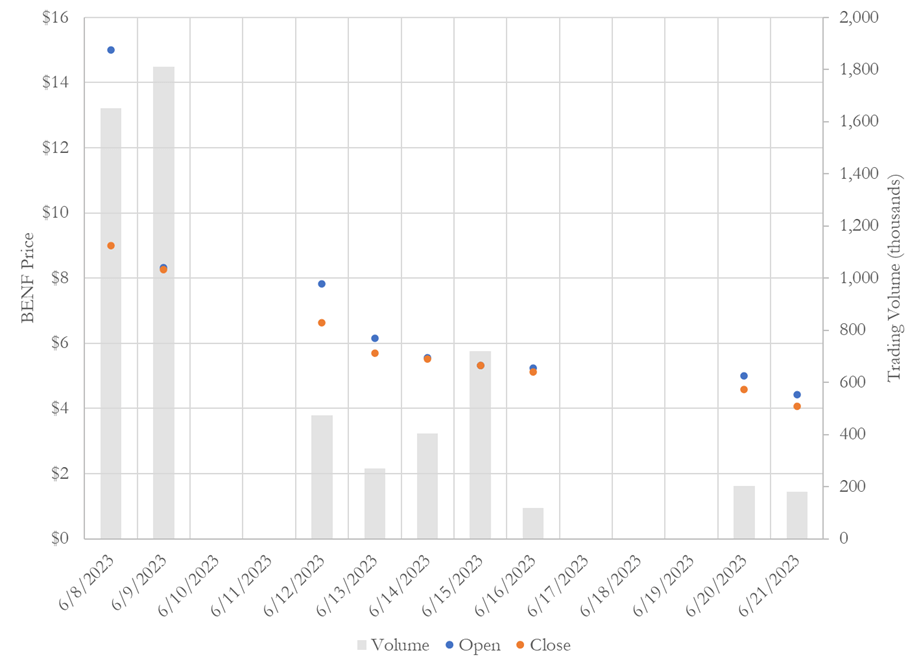

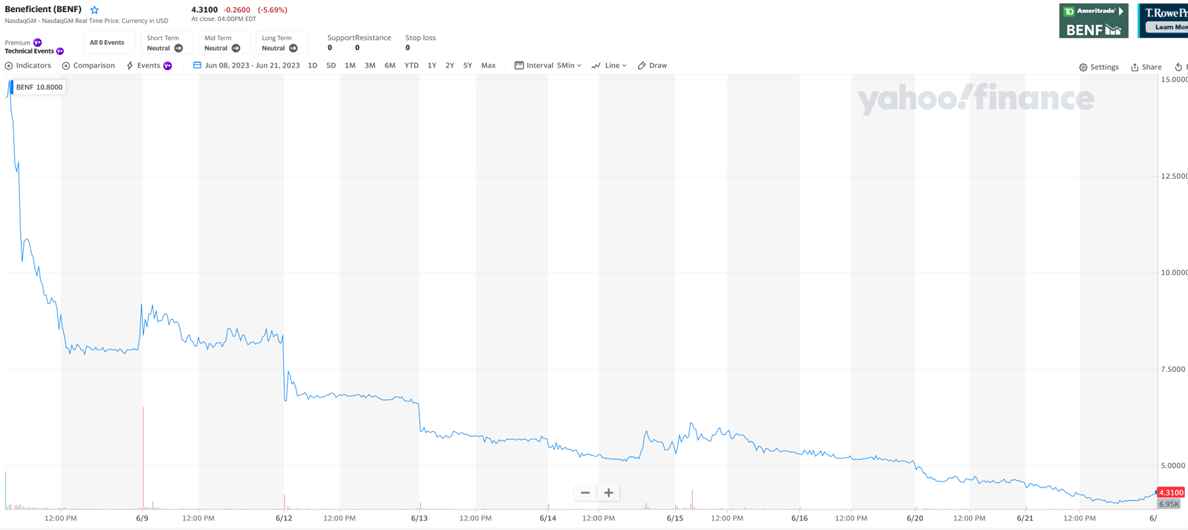

The bondholders' trust will own at least 142.8 million shares of BENF. Since opening at $15 on the first day new BENF traded, the stock has followed a uniquely wretched pattern for nine straight days; each day BENF drops from the open to the close and then opens the next day lower than it closed the previous day on very low trading volumes. See Table 3 and Figure 1.

Table 3. BENF Has Dropped Each Day on De Minimis Volume

Source: Yahoo Finance

As a result of market making activities, the actual number of shares transferred between investors is no more than half the reported trading volumes. Thus, on June 14, the 405,000 reported trading volume means that at most 202,500 shares were sold by investors to investors who purchased no more than 202,500 shares. Excluding the first two days of trading, the average daily reported trading volume has been 365,000 and so at most 182,500 shares have actually been sold by investors. At this rate, it would take 3.5 years to sell the bondholders' 155 million to 165 million shares of BENF.

Figure 1. BENF Has Dropped Each Day on De Minimis Volume

The drop in BENF's opening and closing prices illustrated in Figure 1 is not masking large but transitory positive intraday swings. BENF is working its way down throughout the trading day each day since it began trading. See Figure 2.

Figure 2. Intraday BENF Illustrates a Relentless Dive to $0 in First 9 Days

How Much is BENF likely Worth? $0

We will more fully break down BENF's fundamentals in a future note, but for current purposes we offer a few observations.

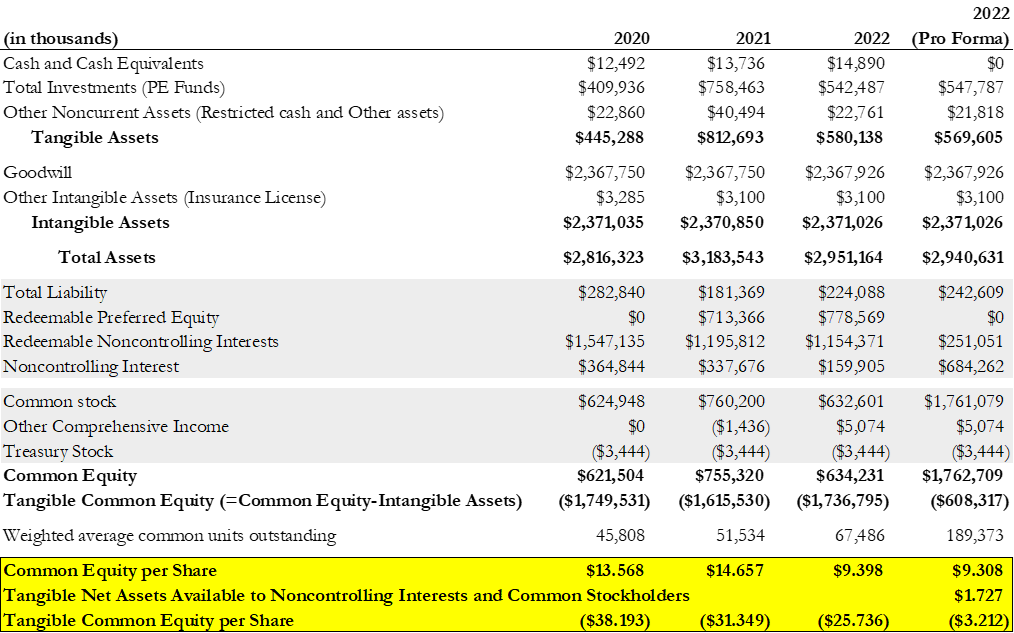

Beneficient values its portfolio of private equity investments at $547.8 million and has $21.8 million in restricted cash as of December 31, 2022. It has $242.6 million in liabilities, so it has tangible net assets of $327 million.

There are $684 million in noncontrolling interests and $251 million in redeemable noncontrolling interests on BENF's balance sheet.

The tangible net assets available to noncontrolling interests and common stockholders is $1.727 per share of common stock although some or all of the tangible net assets would be payable to the noncontrolling interests. If the noncontrolling interests are senior to common stockholders, the tangible net assets available to common stockholders is -$3.212 per share.

Table 4. BENF Tangible Common Equity Per Share is -$3.212

BENF reports 80% of its total assets are goodwill. The only way BENF can be worth some positive value after things settle down is if BENF's $2.37 billion accounting goodwill reflects a substantial market valuation of BENF's intellectual property. Given BENF's historical financial performance and recent trading we believe its goodwill is illusory and its stock nearly worthless.

How Quickly Might BENF Collapse? A few weeks.

The bankruptcy court held a hearing this afternoon to approve an uncontested motion for an order allowing the debtors to sell BENF stock. The proposed order is available here. I listened into the hearing this afternoon and the Court has approved the proposed order. The bondholders' trust holds 125.7 million shares which are eligible to be sold immediately. In a few weeks, after 20 trading days, the bondholders' trust will receive another 30 million to 40 million BENF shares.

Based on our research to date, we believe BENF will continue to drop on low trading volumes and any attempt by the bondholders' trust to sell millions of BENF shares will drive the price close to $0. Ultimately bondholders will receive negligible amounts — perhaps $1 per share — for their BENF common stock. Even this amount can not be achieved in open market transactions when the market is not absorbing total sales of 100,000 to 200,000 shares per day. Only through a bulk sale of a large controlling interest can the bondholders' trust hope to realize even $150 million

Returning to Table 1, recovery of $150 million through block stock sales pays bondholders 9 cents on the dollar. Additional recoveries through litigation might generate another 9 or 10 cents many years in the future.