Kevin Dugan noted in the April edition of Bloomberg's Structured Notes Brief that "Citigroup collected the highest average fees in the first quarter [of 2013] among the 10 biggest underwriters of U.S. structured notes." This got us wondering, is there any relationship between the credit quality of the underwriter and the fees the underwriter collects? If investors truly understood credit risk, issuers with higher credit risk would presumably have to structure products with lower fees to entice investors. All else equal, as credit risk increases, the fee should decrease.1

To explore this question, we obtained the rates on one-year credit default swap (CDS) contracts for nine of the ten underwriters -- data was unavailable for Royal Bank of Canada. The rate on a CDS contract reflects the perceived likelihood that an issuer will be unable to pay their obligations as they become due. Essentially the higher the CDS rate, the higher the probability of default.

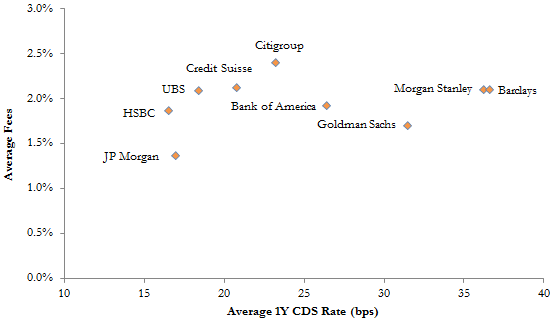

We averaged the daily observations of the CDS rates over the first quarter 2013 and plotted them against the results of Kevin's study on structured note fees (CDS rates are quoted in basis points with 100 basis points = 1%):

This analysis shows that higher fees don't necessarily mean the underwriter is of higher credit quality -- lower CDS rate. Morgan Stanley and Barclays had the highest perceived risk of default in the first quarter 2013, but still charged fees higher than the average for this group of nine. On the other hand, Citigroup charged the highest fees and was the median underwriter with respect to perceived risk of default.

Investors considering structured notes should remember that these products are often short term and carry high fees (both explicitly stated and implicit in their structuring). In addition, investors are exposed to the credit risk of the issuer. This is sometimes forgotten in the complex structure, but a structured note is still basically single-name corporate debt from a financial company.

In a perfectly liquid market, in which all investors understood and appreciated credit risk, we might expect that riskier issuers would have to compensate investors with lower fees or better terms on the notes. At least in regards to fees, that does not appear to be the case in the real world.

_______________________________________

1 This analysis assumes, for simplicity, that issuers would not change the features of the products (cap levels, etc.) to compensate investors for credit risk.